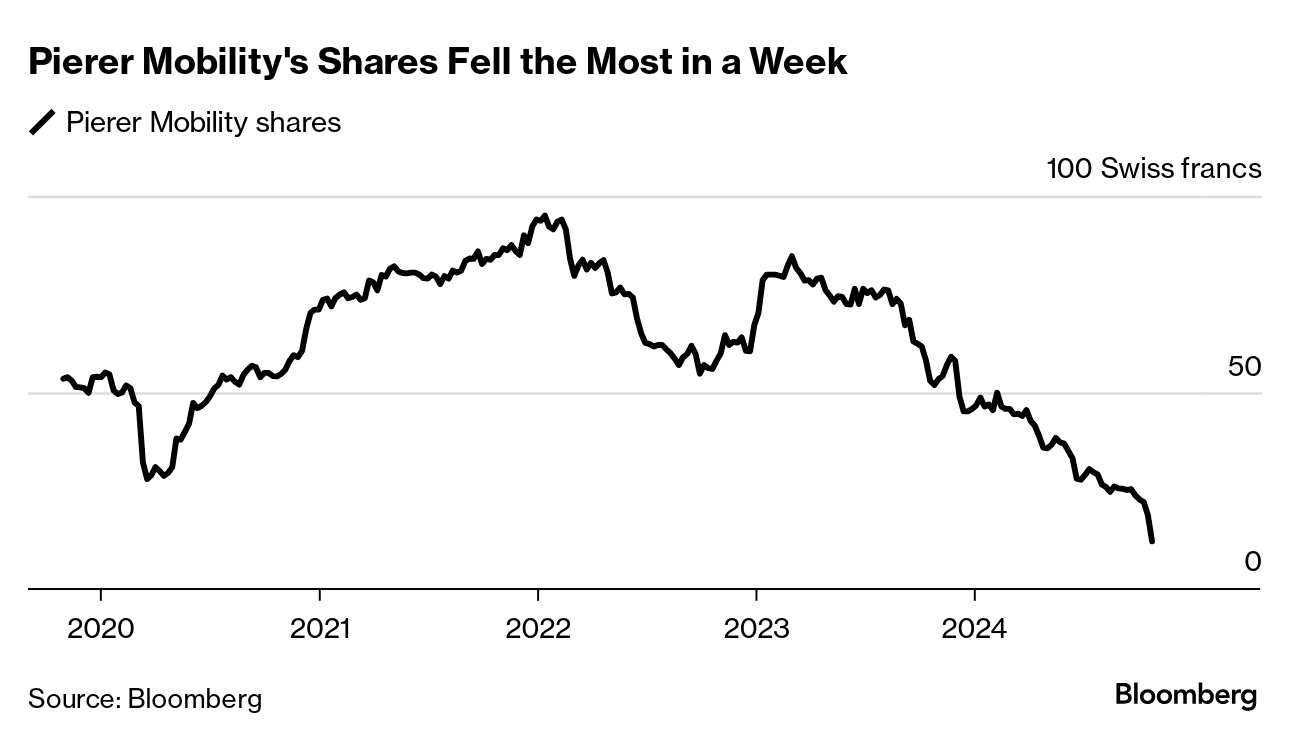

| In the world of motorbike racing, KTM is a well-respected brand, with a racer in the top rankings of MotoGP, the two-wheeled equivalent of Formula 1. In the real world, the Austrian company is struggling to keep up. Shares in KTM’s parent company, Swiss-listed Pierer Mobility — which owns a variety of motorcycle brands such as Husqvarna, MV Agusta and e-bikes — recorded the biggest weekly slump on record in the five days to Oct. 25 after its full-year earnings guidance was scrapped. Pierer Mobility’s story is an all-too-familiar one among companies that experienced an unexpected surge in sales during Covid-19 lockdowns. Needing to keep up with demand, the firm increased inventory, leaving it in a difficult position when sales suddenly slumped as the world returned to normal. The earnings debacle followed unexpectedly high impairment in Pierer Mobility’s e-bike segment, which has been undergoing restructuring, as well as a slowdown in demand for motorcycles, particularly in the US. The company has also been seeking to support its dealer base during the period of weaker sales by allowing dealers to pay for stock later, driving up working capital needs. Pierer Mobility’s debt had already started to show signs that investors weren’t comfortable even before last week. Market participants say investors have been trying to sell KTM’s promissory notes, also known as Schuldschein, at levels close to par. Such instruments are more illiquid than bonds or syndicated loans, which typically makes sales quite slow. Under the terms of the Schuldschein, KTM is required to increase interest payments if it fails to meet certain credit metrics, which will be tested when it reports annual results. In the event of a miss, the interest rate will be increased by 50 basis points, management said during the first-half earnings call. The notes don’t have covenants that would allow lenders to call for early repayment.  A Husqvarna AB 701. Photographer: Michaela Handrek-Rehle/Bloomberg Austrian businessman Stefan Pierer bought KTM’s motorcycle business out of insolvency in 1992, and listed Pierer Mobility in 2016 after building out new models and acquiring more brands. Around 75% of Pierer Mobility’s shares are held by a joint venture between Pierer and India-based automotive manufacturer Bajaj Auto. Pierer is known for his turnaround bets, most recently through the recapitalization of distressed Austrian firetruck maker Rosenbauer International alongside Red Bull heir Mark Mateschitz. He became the sole shareholder of embattled German auto supplier Leoni last year following a debt restructuring, and now plans to sell a 50.1% stake in the business to China’s Luxshare.

Pierer’s bets on Rosenbauer suggest he isn’t short on cash and he has already stepped in to provide some more support for his broader network of businesses. As recently as four months ago, he injected around €255 million via a profit participation right into Pierer Industrie AG, which indirectly owns a stake in Pierer Mobility, according to first-half results. |