Get ready. We’re about to endure three days of earnings reports from five of the six biggest companies in tech—not including Nvidia, which doesn’t report earnings until Nov. 20. What makes these updates more interesting than usual is that investors appear to have wildly varying views of these companies right now, at least judging by their recent stock performances.͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Oct 28, 2024

The Briefing

By Martin Peers

Supported by

Thanks for reading The Briefing, our nightly column where we break down the day’s news. If you like what you see, I encourage you to subscribe to our reporting here.

Greetings!

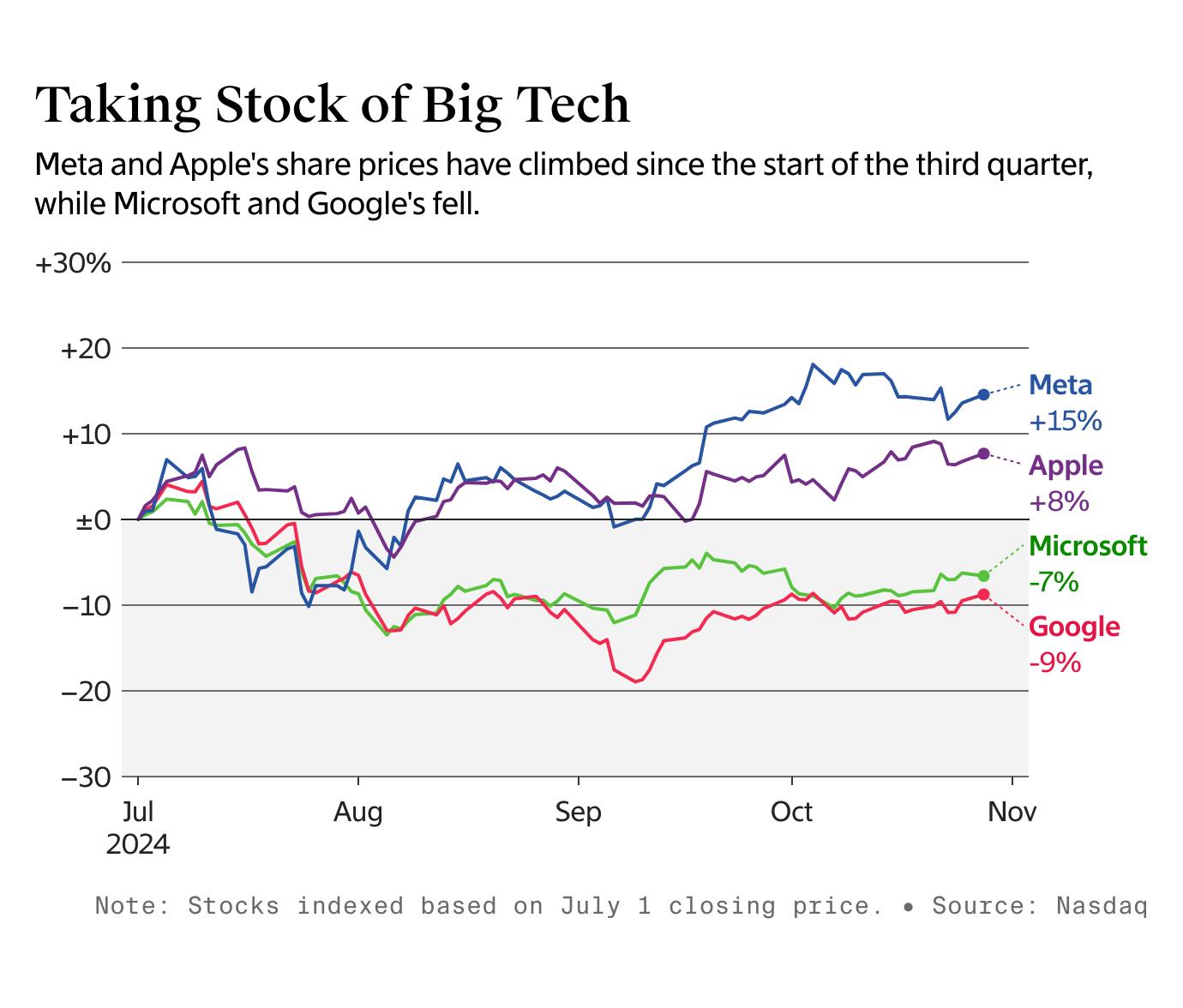

Get ready. We’re about to endure three days of earnings reports from five of the six biggest companies in tech—not including Nvidia, which doesn’t report earnings until Nov. 20. What makes these updates more interesting than usual is that investors appear to have wildly varying views of these companies right now, at least judging by their recent stock performances.

Shares of Microsoft and Alphabet both peaked in early July and since then both have fallen, by 8.6% and 12% respectively. The opposite is true for Apple and Meta Platforms. In fact, Apple today closed about 1% below its year-high set a few days ago, while Meta is trading 3% below its 2024-high set early this month. (See the accompany chart.) And there’s no one-size-fits-all explanation.

Meta is most likely benefiting from its relatively solid growth—analysts expect it to report 17% higher third-quarter revenues on Wednesday, according to S&P Global Market Intelligence. While that’s a slowdown from the past two quarters, it’s several percentage points faster than what Meta’s nearest rival in digital advertising, Google, is expected to report. Indeed, investors appear to be so appreciative of Meta’s growth that they’re overlooking the fact that Meta is spending hugely on AI with no clear path to a return.

In the case of Apple, as we reported today in this analysis, its stock is trading at a premium despite the fact that analysts expect it to report just 5.5% higher revenues for the September quarter. Investors may like Apple partly because it’s not spending as much money on AI as others. They may be hopeful that the AI features Apple is starting to roll out—the first of which came out today—will jumpstart stagnant iPhone sales. But investors may simply have faith in Apple’s sheer dominance in smartphones and the surrounding ecosystem, unthreatened by any near term rivals.

Investor perceptions of Google and Microsoft are much more downbeat, concerning risks related in one way or another to AI. As Arete Research analyst Richard Kramer put it to me, investors are concerned about the sheer volume of capex that Microsoft has to spend to support its AI business and about the long-term risks facing Google’s search business.

But investors are far less worried about such risks facing Apple. “Who is Apple's natural predator?” Kramer says. As for Meta, he says “people look at the combination of sales growth and cost cuts and extrapolate further earnings leverage, despite equally exploding AI-led capex.”

That suggests what Google reports on Tuesday about its business—particularly if competition from AI chatbots is having any impact on search—will be closely watched. The same is true for what Microsoft says about how its cloud business is benefiting from its AI investments. What Meta CEO Mark Zuckerberg says about the company’s ad outlook could be important. On the other hand, investors seem to take a longer term viewpoint of Apple’s performance.

Bezos’ Calculus

The outcry over the Washington Post’s decision to not make a presidential endorsement, reportedly at the behest of owner Jeff Bezos, is having an impact on the newspaper’s business. About 200,000 digital subscribers had canceled their subscriptions as of midday Monday, NPR reported, about 8% of the news organization’s subscriber base.

That’s a big number—for the Post. But it’s a tiny amount of money for Bezos, who may be more worried about the potential damage that alienating former president Donald Trump could do to his main businesses.

Assuming each Post subscriber was paying for a premium subscription, which costs $170 annually after the first year, these cancellations would cost the Post $34 million. That’s just 2% of the revenue that Amazon brings in daily.

Bezos may be more worried about protecting Blue Origin, his rocket company, whose executives met with Trump last week. We don’t know how much revenue Blue Origin brings in. But given the importance of government contracts to space businesses like his, Bezos can’t be blamed for wanting to maintain cordial relations with Trump. (The Post published an opinion piece by Bezos tonight about the episode and its worth reading).

So yes, Bezos might lose a few bucks from angry Washington Post readers. But staying on Trump’s good side will save him much, much more money. Still, Bezos could have saved himself some grief by making his decision much earlier, rather than days before the election.

In Other News

• Microsoft on Monday accused Google of running “shadow campaigns” to turn monopoly regulators and the public against the enterprise and cloud incumbent and distract them from Google’s own antitrust woes.

• The RealReal named Rati Sahi Levesque, a longtime executive at the luxury resale site, as CEO, succeeding John Koryl, who has left the company after less than two years in the top role.

• Some 75% of OpenAI’s revenue comes from consumers paying for its AI-powered chatbot and other products, a company spokesperson said on Monday. That figure highlights the uphill battle OpenAI and its rivals face in getting businesses to pay for their AI software.

Recommended Newsletter

More than 100,000 readers rely on The Information's Creator Economy newsletter for coverage of the creator startups making waves, big tech companies' social media playbooks, and scoops on the sector's biggest hires. Start receiving the free newsletter here.

Join Anita Ramaswamy and a panel of experts from NYSE, Citi and J.P. Morgan to hear their forecasts for IPOs in the months ahead. Request an invite — space is limited.