| Welcome to the Mideast Money newsletter, I’m Adveith Nair. Join us each week as my team and I chronicle the intersection of money and power in a region that's become one of the most influential in global finance. You can sign up here. In the week’s special edition, we look at Saudi Arabia’s flagship event that’s drawing in heavyweights from the worlds of business, finance and technology — deals worth more than $28 billion are expected to be announced over the coming days. We’ll also cast an eye on Riyadh’s Vision 2030 economic transformation plan. The most influential names from the world of finance and business are flying to Riyadh for the eighth iteration of the kingdom’s Future Investment Initiative. Dubbed ‘Davos in the Desert,’ the event’s pre-summits started Monday. Over the course of the next few days, we’ll hear from the likes of David Solomon, Jane Fraser, Marc Rowan and Larry Fink. They’re heading to the kingdom amid a profound shift in their relationships with Saudi Arabia’s nearly $1 trillion wealth fund. The Public Investment Fund — like other regional sovereign investors — is increasingly flexing its financial muscle and wants foreign firms to do business on its terms. In previous years, the titans of finance would flock to the FII to raise money and invest it around the world. Now, they’re faced with a kingdom that’s more domestically-focused than ever. (My colleagues have previously written about that local pivot, and how it’s boosting the profile of a low-key executive at the PIF.) Also Read: Goldman Joins Rivals in Setting Up New Mideast-Focused Fund Broadly, there will be a focus on the US election and implications of a change in leadership in the world’s largest economy. Lower interest rates and their impact on markets and deal-flow, as well as questions around conflict in the region and oil prices, will be other key themes. On the finance side of things, Solomon’s remarks will be scrutinized for updates on Goldman Sachs’ plans in the kingdom, after the bank became the first Wall Street lender to obtain a so-called regional headquarters license. That came days before Bloomberg News reported the government is doubling down on efforts to get international firms to boost their local presence — or risk losing business. BlackRock is among firms that have been ramping up efforts locally. The firm secured a $5 billion commitment to invest in the Middle East and plans to build an investments team based in the kingdom. The world’s biggest fund manager is also now helping develop a market for mortgage-backed securities as the kingdom looks to improve the affordability of its housing stock.

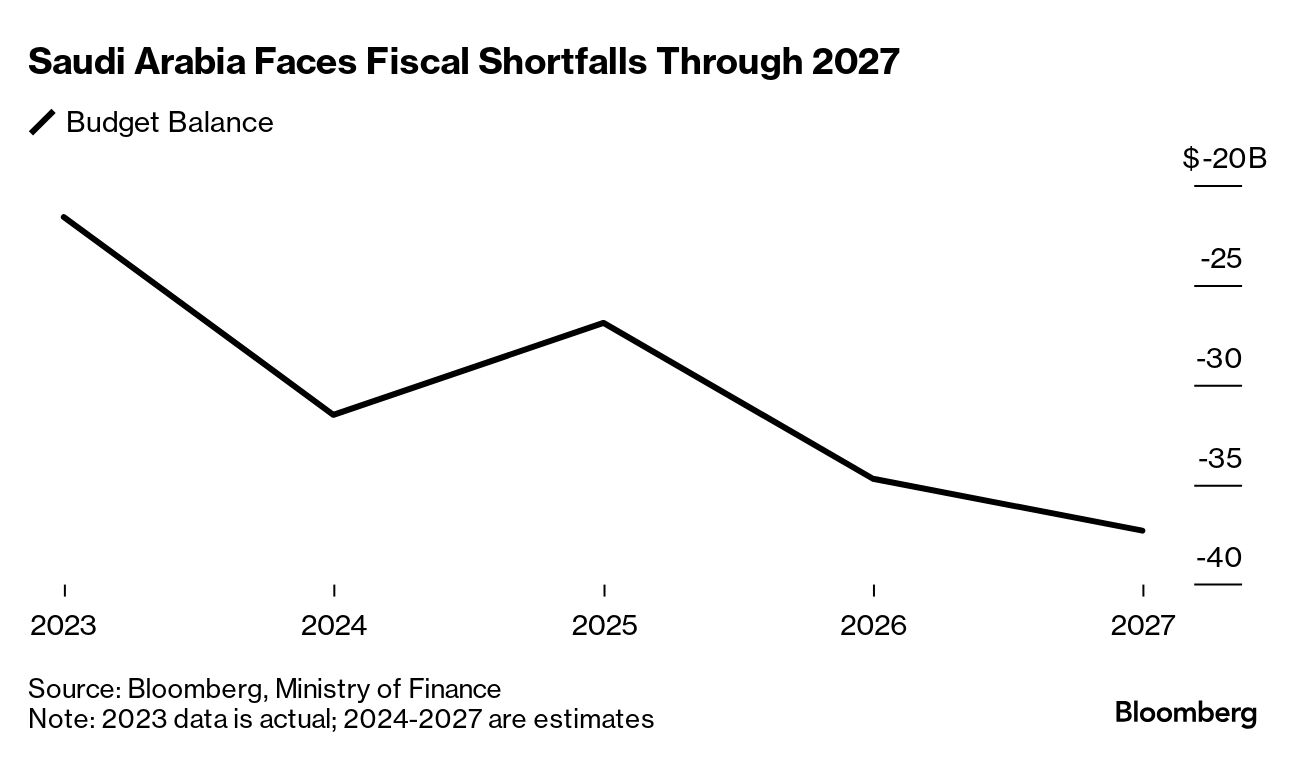

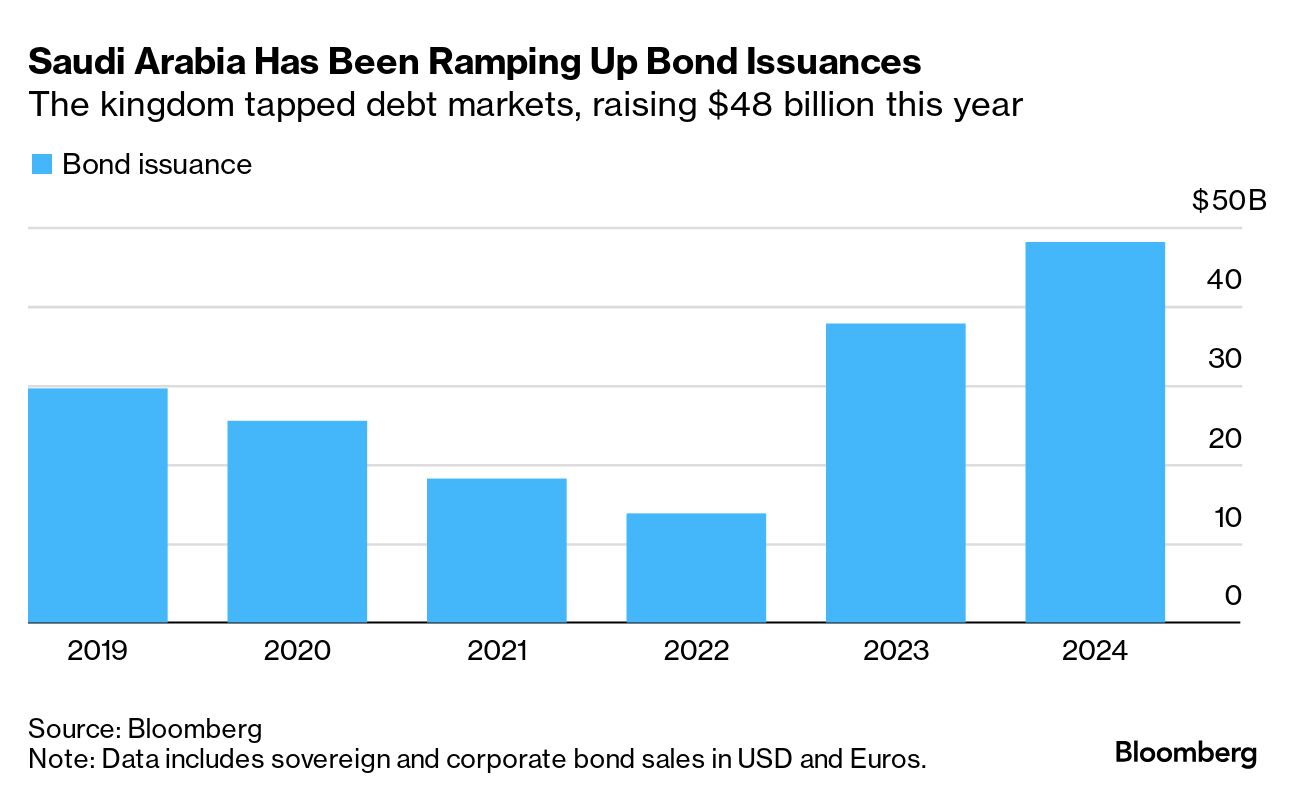

Also Read: General Atlantic Opens Saudi Office to Scout Mideast Deals Here, firms face a delicate balancing act. Neighboring Abu Dhabi — home to $1.5 trillion in sovereign wealth — is also staking a claim to be the region’s preeminent financial hub, while Dubai has for years been the center for business. Both cities in the UAE have drawn the world’s biggest firms for reasons including the lifestyle on offer. The choreography of FII 2024 will be similar to previous years. The main event will kick off with a keynote address from Yasir Al Rumayyan, and like last year, his remarks will come against the backdrop of conflict in the region. In 2023, the PIF governor spoke about the importance of artificial intelligence and the months since have offered some insight into the kingdom’s plans.  PIF Governor Yasir Al-Rumayyan. Photographer: Marco Bello/Bloomberg Also Read: Saudi Arabia, UAE Bet on Chips to Power Post-Oil Future The PIF is in early talks to partner with venture capital giant Andreessen Horowitz on an AI fund, which may grow to as large as $40 billion. It’s already backing an investment firm with $100 billion in capital that will plow money into industries including semiconductors and tech. (Neighboring Abu Dhabi is setting up its own technology investment firm, targeting deals in AI and semiconductors. That one aims to top $100 billion in assets under management in a few years.) And as the kingdom lays out its plans in that space, investors will scrutinize plans for how it intends to pay for them — and the various giga-projects. Falling oil prices and sputtering foreign direct investment have forced Saudi Arabia to scale back its medium-term ambitions for the desert development of Neom, and officials are likely to cut billions of dollars in spending on some of the biggest development projects, Bloomberg News has reported. Also Read: Middle East Trillions Force New Concessions From Wall Street  Project renderings in the window of the Neom pop-up store, showing the Sindalah Island development, right, and The Line, in Davos, Switzerland. Photographer: Stefan Wermuth/Bloomberg Amidst those setbacks, the kingdom welcomed an exclusive group to Sindalah Island, the first project to open its doors at Neom. Timing that with FII makes sense, said Karen Young, a senior research scholar at Columbia University’s Center on Global Energy Policy. “If investors see some major infrastructure in place for power, water, transport, that would do a lot to instill confidence about government commitment to major installations in Neom,” she said. It’s not just Neom. Saudi Arabia is preparing to begin construction on its next giga-project: a cube-shaped skyscraper big enough to fit 20 Empire State Buildings. The building, which will become the largest built structure in the world when it’s finished, will be the centerpiece of New Murabba, a community the country hopes will be a new destination within the capital city of Riyadh.  Artist illustration of the Mukaab building, center, and New Murabba. Source: New Murabba Development Co. The ambitious project is part of a series of developments that are key to Crown Prince Mohammed bin Salman’s Vision 2030 agenda, which is set to to turn Saudi into the world’s biggest construction market. Related Coverage: But the crown prince is increasingly having to come to terms with the limits of even Saudi Arabia’s vast financial resources to pay for his ambitions. The government has slashed its economic growth forecasts and projected deeper budget deficits than previously estimated — as its revenue from oil exports slumped to the lowest in over three years. The kingdom needs crude at $96 a barrel to reach equilibrium in its finances, according to the International Monetary Fund. Bloomberg Economics puts the so-called breakeven at $112, once domestic spending by the Saudi sovereign wealth fund is taken into account. Brent crude has been trading in the $68 to $86 range all of this year. As the oil-rich kingdom faces growing financial pressures, the government and its entities have issued around $50 billion in bonds this year, according to data compiled by Bloomberg. Related Coverage: The Saudi wealth fund is planning to ramp up annual spending to as much as $70 billion from 2025 — and a larger share is expected to be channeled to local projects. Still, the PIF maintains that the absolute amount allocated for international investments will increase over time. It’s also directing more of its firepower at China, in line with the kingdom’s deepening ties with Beijing. In just the last couple of months, the PIF has signed agreements worth as much as $50 billion with six Chinese financial institutions and unveiled plans for a so-called special economic zone inside the country to boost trade with China. The PIF has also benefited from a rally in global stocks, which helped push annualized returns since 2017 to 8.7%, up from 8% a year earlier. And as evidenced by recent deals to buy stakes in London’s Heathrow Airport and UK department-store chain Selfridges, the PIF is still investing globally.  A Lucid Air electric vehicle. Photographer: Samuel Corum/Bloomberg It’s also pumping more cash into some of its investments in the startup space to ensure the returns they want. Case in point: The PIF has now infused around $8.5 billion into struggling electric vehicle maker Lucid. Related Coverage: Saudi Arabia is plowing billions into tourism, sports and entertainment that are key pillars of the Vision 2030 plan. The kingdom wants to welcome 150 million tourists by 2030 and for the sector to account for 10% of its gross domestic product by then. To reach its ambitious targets, officials plan to pour $800 billion into the sector over the next decade. Luxury resorts on the Red Sea, |