| | In this edition, Meta finds a new revenue line. And private credit investors keep cashing out.͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Business |  |

| |

|

- Warsh’s way

- Blue Owl’s slow bleed

- Trump Account lock-in

- The bank of Nvidia

- Gulf SWFs surprise

|

|

Does the world have too much compute or not enough? Meta’s new cloud business — selling excess compute capacity to outside customers — is confusing on its face. For years, the big tech companies have insisted their problem is a shortage of compute, not a surplus. If they’ve now hoarded so much of it they can peddle the leftovers, that’s a bad look, at best. At worst, it suggests Meta can’t find anything better to do with the chips it’s been stockpiling and that its AI efforts may be struggling. Just eight months ago, Mark Zuckerberg struck a very different note: Meta would use any extra compute it had “to accelerate our core [advertising and apps] business — which continues to be able to profitably use much more compute than we’ve been able to throw at it,” he said in October. What’s changed? Investors are losing patience. Meta’s stock had dropped 14% this year as shareholders questioned what the company was getting for the $135 billion in projected capex. Alphabet and Amazon’s shares have risen — same AI spending increases, but paired with big jumps in cloud revenue. Squeezing a few extra dollars out of consumers by adding tiered subscriptions to Instagram and charging power users of its chatbot wasn’t going to be enough. Spinning up a new revenue line — one tied explicitly to the billions it’s spending on AI — seemed to do the trick; Meta’s shares rose 9% on Bloomberg’s report. There’s a difference between discovering you have a surplus and strategically stockpiling a resource with plans to resell it. Amazon built AWS to serve its own business long before it realized it could make a boatload of money selling the same service to other companies. Meta, a software and ad company, could just as easily be a customer of the hyperscalers rather than a competitor to them. But Zuckerberg likes being on the bleeding edge of tech. The market has made its preferences clear: the beatings will continue until cash flow improves. |

|

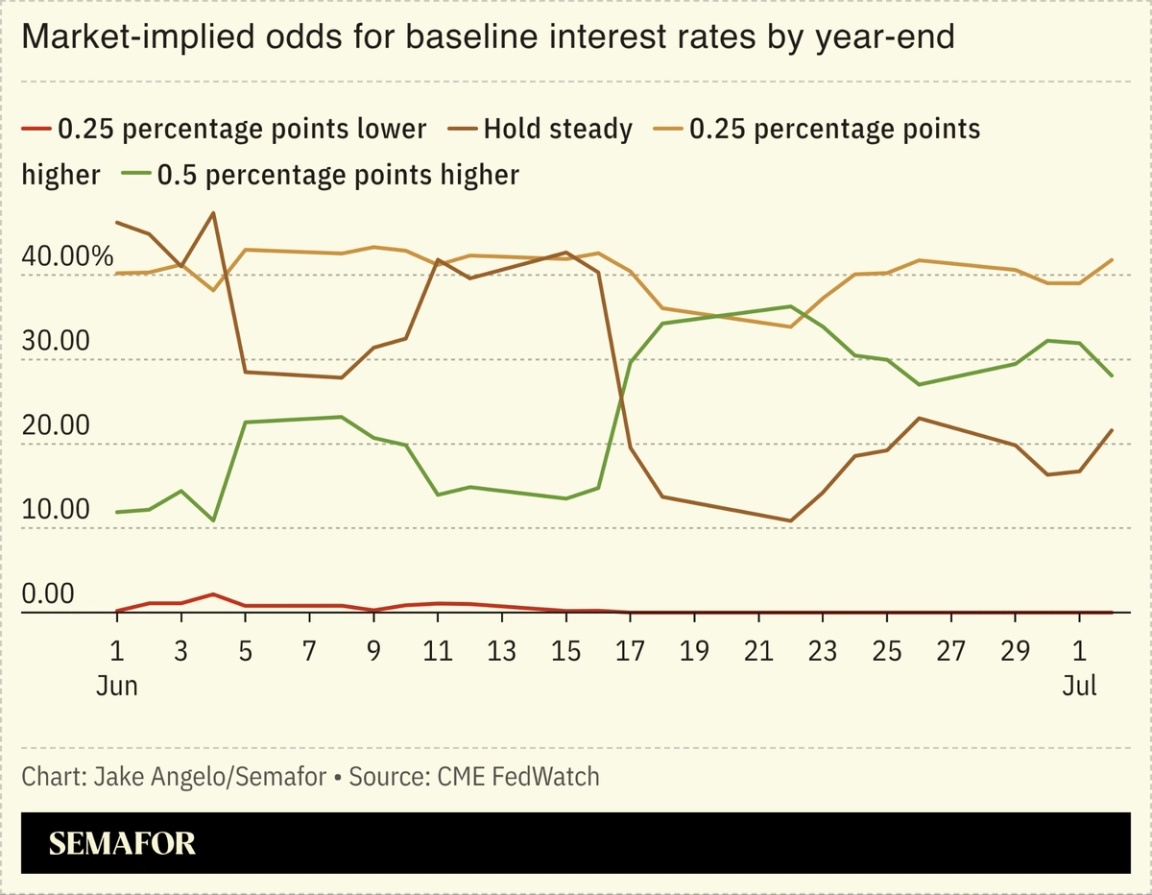

Jobs data changes Warsh’s game |

The US snapped its hiring hot streak in June, a weakening that will complicate the Federal Reserve’s path forward on interest rates. Employers added 57,000 jobs last month, about half of what economists had expected. That puts more pressure on new Fed Chair Kevin Warsh and his colleagues, a dissent-happy bunch over the past year, to consider whether a slowdown in jobs or an uptick in inflation is the bigger risk to the economy. Warsh in June hinted that he sees bringing inflation under the Fed’s 2% goal as the priority, saying “this committee will deliver price stability.” That would favor keeping interest rates high, or even raising them — the market is pricing in at least one rate hike by the end of the year — while protecting a weakening jobs market generally requires cutting borrowing costs to spur businesses to grow. AI complicates the Fed’s playbook even further. Business growth used to mean hiring more people; now it might just mean buying more tokens. And spreading that economic boom beyond a handful of AI companies is quickly becoming a national priority, as the White House weighs taking stakes in frontier labs and politicians float new ways to tax them. |

|

Blue Owl’s slow bleed continues |

Brendan McDermid/Reuters Brendan McDermid/ReutersInvestors asked to withdraw $4.7 billion across two big Blue Owl funds, slightly less than last quarter but still reflecting concerns about private credit, particularly loans to software companies imperiled by AI. Blue Owl has enough cash coming in from loan repayments to cover what is essentially a slow-moving run on its bank. Private credit funds let investors pull their money once a quarter, and redemptions at Blue Owl’s funds and others run by Apollo, KKR, and Blackstone have soared in recent months. The bigger question is: What happens next? The panickiest investors will eventually be fully redeemed — assuming there isn’t a wave of defaults in the underlying loans, which appear healthy so far — but it’s hard to see these retail-focused funds shrugging off the past year and returning as the powerful profit engines Wall Street embraced. Expect a pivot to data centers. |

|

Trump Accounts are missing key feature |

Jonathan Ernst/Reuters Jonathan Ernst/ReutersTrump Accounts will launch next week without a key feature that Wall Street wanted to see. Semafor’s Eleanor Mueller reports that the accounts — which are essentially 401(k)s for kids seeded by $1,000 in government cash — will not initially allow customers to move the funds from a handful of designated firms to their money manager of choice. The big win for financial firms was never getting the first-day dollars, which are tiny, but in being able to push users to move the accounts onto their platforms. They have seen Trump Accounts as a cheap way to acquire customers who might stick with them for decades. Experts estimate that more than half of the children eligible to receive $1,000 in seed money still have not enrolled. |

|

Nvidia finances more demand for its chips |

Kent Nishimura/File Photo/Reuters Kent Nishimura/File Photo/ReutersNvidia is playing banker to new players in the AI race. It told The Information that it’s cutting deals with neoclouds — smaller players spinning up GPU clusters to compete with Google, SpaceX, and other hyperscalers — to finance their purchases of its chips in exchange for a cut of their revenue. By extending its own balance sheet and AA credit rating to its scrappier customers, Nvidia is only deepening its role propping up huge parts of the AI boom. But it’s a smart play for the chip giant to diversify away from hyperscalers — and a way to blunt criticism that the AI world is becoming anti-competitive. Whether AI is ultimately pro-competitive (by making it easier and cheaper for anyone to start a business) or anti-competitive (by concentrating so much of the economy in the hands of a few companies with the capital to build it and clout to set the terms) is an open question. Nvidia sits at the heart of it, and as Trump put it, uncomfortably beyond the reach of traditional antitrust enforcement: “I figured we could go in, and we could sort of break them up a little bit, get them a little competition, and I found out it’s not easy in that business,” he mused last summer. — Rohan Goswami |

|

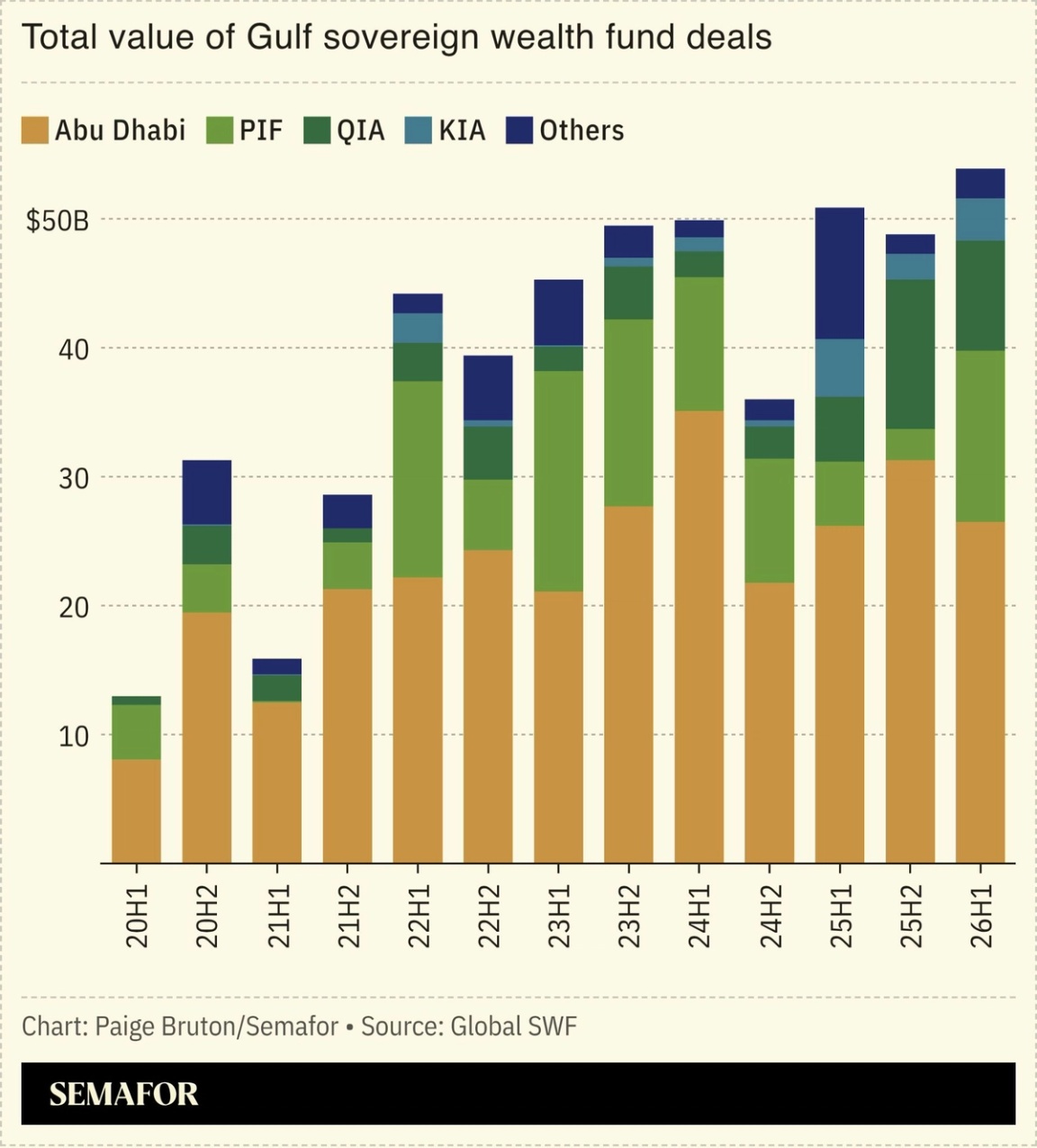

War doesn’t dim Gulf’s appetite |

Gulf sovereign wealth funds are on track for one of their busiest years on record, despite the economic disruptions caused by the Iran war. In the first half of 2026, Gulf funds invested a record $54 billion into 108 deals, according to data compiled by Global SWF. Almost half of that went into the US, including funding rounds for Anthropic and xAI (pre-SpaceX merger), showing that, even as the Iran conflict led to questions about the future of Gulf-US ties, America remains the main destination to recycle petrodollars. China was a distant second, receiving 17% of Gulf investments. Overall, half of the world’s largest deals so far this year involved Gulf sovereign capital. — Matthew Martin |

|

➚ BUY: Cravats. Chanel struck a deal for Charvet, a luxury shirtmaker, in an effort to establish a distinct menswear brand. Rohan is taking suggestions for new tie suppliers. ➘ SELL: Cravath. The BigLaw salary race began several weeks ago, when Milbank upped starting pay for associates to $235,000. So far, Cravath — which typically matches Milbank’s moves within days or weeks — hasn’t matched, nor have the other BigLaw firms. |

|

Companies & DealsWatchdogs- “Just not workable”: Emails between Pentagon officials and Anthropic CEO Dario Amodei show how their fight, patched up this week when the US government cleared its Fable model for release, got so fraught. Read them here.

- Help us help you: Microsoft said it would be investing $2.5 billion and 6,000 employees into a new group focused on helping businesses better understand how to implement and take advantage of AI, two days after Amazon made a similar announcement.

Markets- High on its own supply: South Korea’s exports posted the strongest growth since 1978, as sky-high demand for memory chips pushes up results.

- We’re so back: Saudi Arabia’s oil exports reached 90% of pre-war levels, driving oil prices back below pre-war prices of around $70 a barrel.

|

|

|