|

|

|

|

Good morning. All eyes are on Washington, where new U.S. Federal Reserve chair Kevin Warsh will deliver his first interest rate decision this afternoon. Everyone expects the Fed to hold, but this will be the first chance to see Warsh in action. In focus today we look at the balance he needs to strike between Donald Trump on one side and inflation on the other, along with a new study putting grocery prices under the microscope. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy: Oil prices plunged again after news that the U.S. and Iran had reached a yet-to-be-signed deal to end the war and reopen the Strait of Hormuz. |

|

|

|

|

|

|

|

|

|

|

Retail: Gildan Activewear’s shares tumbled 19 per cent on Tuesday after an American short seller alleged that the T-shirt maker was inflating its sales numbers, wiping about $3-billion from its market value. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

President Donald Trump speaks with Chairman of the Federal Reserve, Kevin Warsh after a swearing-in ceremony at the White House on May 22. Anna Moneymaker/Getty Images

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Welcome to the Warsh Era. I’m Mark Rendell, The Globe’s economics reporter. |

|

|

|

|

At 2 p.m. ET the U.S. Federal Reserve will publish its latest interest rate decision – almost certainly a hold. Thirty minutes later, Kevin Warsh – the suave 56-year-old banker whom President Trump dubbed his “central casting” pick – will take the podium for the first time to explain the decision to the world. |

|

|

|

|

|

|

|

|

That’s when things will get interesting. |

|

|

|

|

Warsh, who served on the Fed’s board of governors from 2006 to 2011, was long regarded as an inflation hawk. Over the past year, however, he recast himself as an advocate for cheaper borrowing as he looked to curry favour with President Trump. |

|

|

|

|

The call for lower interest rates was a respectable position in January, when Warsh was tapped to replace Jerome Powell as the head of the world’s most important financial institution. Five months later, not so much. |

|

|

|

|

|

|

|

|

|

|

The global oil price shock from the war in the Middle East and a string of strong economic data have scattered the inflation doves. Headline inflation in the U.S. came in at scorching 4.2 per cent in May (although the numbers were less hot under the hood

). Several members of the Federal Open Market Committee – which sets interest rates – have already said they want to drop the language suggesting the Fed has an easing bias, and markets have swung from pricing in rate cuts later this year to pricing in a possible hike in December. |

|

|

|

|

That puts Warsh in a tricky spot for his debut.

He can’t ignore the turn in the data and among his colleagues. After all, the chair is only one of 12 votes on the FOMC and needs to present his colleagues’ views alongside his own. But an overly hawkish performance could rile Trump, who tends to make life miserable for central bankers who don’t want to cut interest rates. (Just ask Powell, who has decided to remain on the FOMC for his sins.) |

|

|

|

|

“Don’t look at me, don’t look at anybody, just do your own thing and do a great job,” Trump told Warsh last month at his swearing-in ceremony. How long will this graciousness last? Watch for the Truth Social post. |

|

|

|

|

Ultimately, Warsh needs to build trust with his new colleagues more than appease the President if he wants to push through his vision of “regime change” at the Fed. He was lauded on Wall Street as a safe choice to lead the central bank. But he has big ideas about changing it. |

|

|

|

|

|

|

|

|

|

|

Warsh thinks central bankers have become too chatty. So look for fewer, or shorter, press conferences and fewer speeches by other Fed governors. |

|

|

|

|

And he doesn’t like forward guidance – the Fed’s practice of trying to influence market interest rates by signalling what it intends to do in the future. There’s speculation that the FOMC could scrap its famous “dot plot,” where committee members write down their predictions for future interest rates. |

|

|

|

|

“I don’t think we’ll go back to the 1970s, when it’s a smoke-and-mirrors Fed, where there’s no communication. Probably just less communication than we’ve been used to,” Thomas Ryan, senior North America economist at Capital Economics, told me last week. |

|

|

|

|

Then there’s the Fed’s balance sheet. Warsh has been a longstanding critic of quantitative easing: the practice of buying bonds to try to hold down interest rates. Several rounds of QE since the 2008/09 financial crisis have caused the Fed’s balance sheet to balloon. Warsh has said he wants to slim it back down, although it’s not clear how much buy-in he’ll get from other FOMC members. |

|

|

|

|

Regime change takes time. But if you want to see where things are heading, Warsh’s presser this afternoon is the can’t-miss TV event for finance nerds. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

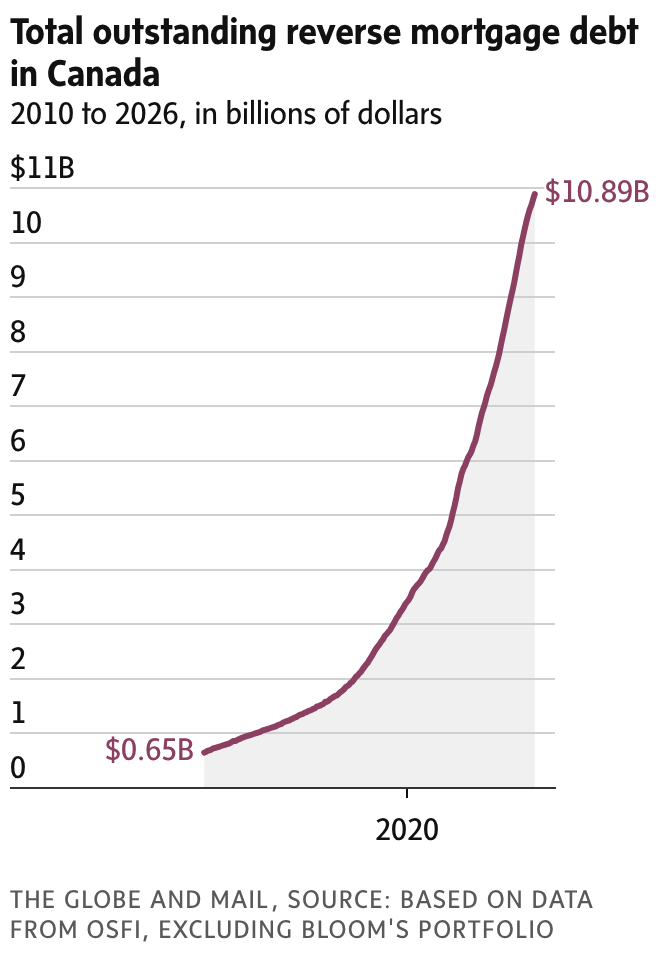

This debt market has quietly grown to almost $11-billion |

|

|

|

|

|

|

|

|

|

|

|

|