| | In this edition, why prediction markets will ultimately fix their insider trading problem, and US Tr͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Business |  |

| |

|

- Global bond selloff

- A shadow stock market

- CEOs are stressed

- NextEra’s AI bet

- Joe Weisenthal is not a doomer

Trump withdraws fresh Iran threat … Chinese looksmaxxing … Cramer glitches over Trump stock trades |

|

Kalshi and Polymarket have either a massive insider-trading problem or the appearance of one. It doesn’t really matter which. But my bet is that they’ll fix it — because it’s in their financial interest. For starters, people don’t want to participate in a market they think is rigged. Military, political, and corporate insiders cashing in on things they have knowledge of drives off the users these platforms need to grow. But the bigger motivation for self-policing is what Kalshi and Polymarket could become: key backbones to the biggest capital markets in the world. Today, a trader who thinks Home Depot will beat earnings estimates has to cobble together a clunky position: long HD, short a competitor like Lowe’s, maybe add some lumber hedges for comfort. On Polymarket, you just click “yes.” Home Depot can do the same to, say, hedge its exposure to lumber. Huge swaths of what happens in regulated financial markets today should be happening over there. Polymarket is worth far more as the platform where companies like Meta hedge their future AI compute-pricing risk than as an OTB window for US black-op nighttime raids. The New York Stock Exchange, which invested $2 billion in Polymarket last year, will only be coaxed into acquiring a serious player in institutional finance. It will pay zero dollars to acquire a vibes casino. Maybe that’s just the millennial finance reporter in me, but you knew what you were getting when you signed up for this newsletter — the idea that actually, this buzzy zeitgeist Geiger counter is more interesting as an enterprise-scale platform for institutional investors to express contrarian views on corporate earnings. (Some intellectual backup: Bloomberg’s Joe Weisenthal, our guest on Compound Interest this week, agrees with me.) But to get there, Kalshi and Polymarket need to entice market-makers like Citadel Securities and Jane Street to take the other side of whatever bet these platforms’ vibe-surfing users want to make. Citadel Securities is intrigued by prediction markets, its president told me last month. But it won’t show up if it thinks insiders are across the table. One caveat to this: I might be discounting a different incentive that Kalshi and Polymarket have, which is that they need to be right. Betting platforms have to call outcomes accurately or they’ll get dropped from the cable-news scroll, and insiders nudging odds toward correct answers help with that. It’s a real tension, and not a small one. Still, companies aren’t good or bad. They follow incentives, which usually encourage them to chase profits and foist the negative externalities on the rest of us. This is a rare instance where it’s in their interests to do the right thing. |

|

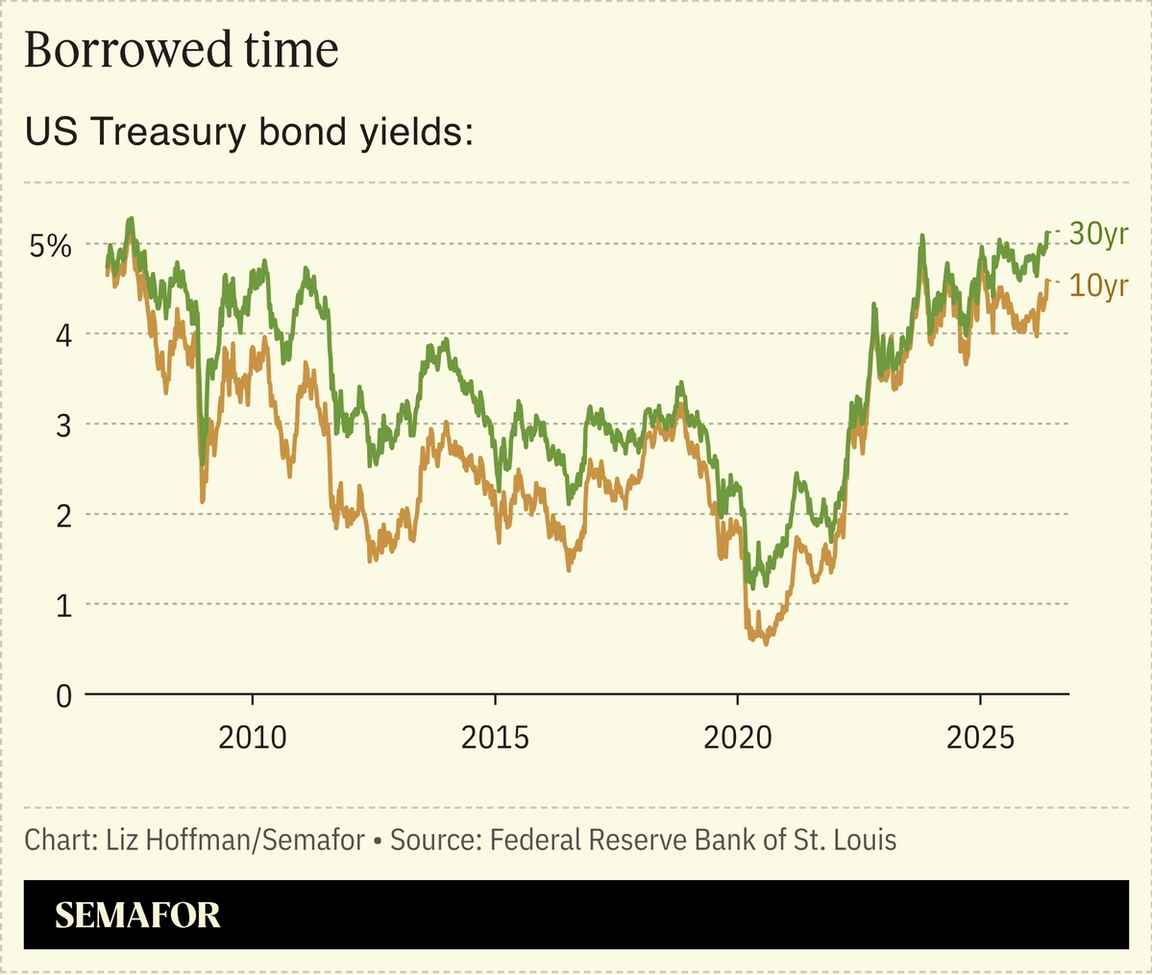

Governments’ borrowing costs surge |

US Treasury yields are flirting with levels last seen in 2007. It’s the result of a global bond selloff driven by inflation, war spending, fears of sustained high oil prices, and a glut of competition from corporate bonds that’s been building for weeks but seems to have just punctured the optimism that’s been driving global markets. The rout is being led by 30-year bonds, the most vulnerable to the compounding effects of inflation and least controllable by the Federal Reserve, which only sets overnight rates. It’s not just the US: The yield on Japan’s 30-year bond hit 4% last week for the first time since Tokyo started issuing them in 1999, and borrowing costs are also surging in Germany and the UK. (In a reminder that governments can be as bad as companies at buying and selling their own securities, the Bank of England has continued selling its own holdings of gilts into the drubbing.) The global selloff is an acute problem for the Trump administration and incoming Fed Chair Kevin Warsh, who will be sworn in on Friday. Interest payments on federal debt are set to crack $1 trillion this year, more than the government will spend on defense or Medicare. Foreign governments are trimming their holdings of Treasury bonds to protect their currencies (in Japan’s case) and because the Iran war has stopped the oil-for-dollars trade (in the case of Saudi Arabia and the UAE.) A bond-market revolt drove Trump back from his “Liberation Day” tariffs last year. Will they force a climbdown in Iran? |

|

Andrew Kelly/File Photo/Reuters Andrew Kelly/File Photo/ReutersWelcome to the wrapper economy, where “ownership” is replaced by “exposure.” The Trump administration is expected to start allowing digital versions of stocks that track prices but don’t carry the typical voting rights or dividends — and could be issued without the approval of the companies themselves. The new rules, which Bloomberg reports could be released this week, would create a new way to bet on corporate fortunes. We already have a way to do that using prediction markets, which strike me as a cleaner and more transparent alternative to the stock market (see the argument above). My bigger concern is that the rise of shadow stock markets could crowd out the real thing: The stock markets exist to connect companies with capital, helping them grow faster. Why would investors bother to buy shares when they can get a token, especially if it’s cheaper? Passive investors don’t care much about voting rights, anyway. And many companies have shifted from paying dividends toward stock buybacks, the benefit of which would likely be captured by tokens. Finance history is full of synthetic products that track economically useful ones, and it rarely ends well. — Liz Hoffman |

|

Chip East/File Photo/Reuters Chip East/File Photo/ReutersCEOs are using earnings calls as talk therapy. Hudson Labs has pulled together a list of the most stressed-out CEOs around the world, putting an AI twist on the practice of combing through earnings reports for signals on where the global economy is heading. The firm’s analysis filtered out explicit mentions of “stress” and instead combed transcripts for more coded language: “disappointment,” “delays,” the agency-less “out of our control,” and the hilariously deflective “mistakes were made.”

Norwegian Cruise Line’s John Chidsey is worried the Iran war is going to make it more expensive to move people and ships around; Daniel Florness of Fastenal, which makes screws, tape, and other construction materials, is stressed about high prices. Builders FirstSource CEO Peter Jackson cited “rumors of [customers and rivals] not being able to pay bills.”

Equity research analysts have long tracked mentions of certain phrases to try and divine how corporate America is feeling, but AI supercharges the process to go deeper into that sentiment. — Rohan Goswami |

|

NextEra’s $67B deal pokes the AI bear |

Bing Guan/Reuters/File Photo Bing Guan/Reuters/File PhotoNextEra Energy agreed to a $67 billion deal for rival Dominion Energy, creating the world’s largest utility as AI-driven energy demand soars. The merger is a big test for the uncomfortable fact facing the AI economy: Many people hate it. The deal would create a giant with 10 million customers across four states at a time of rising local backlash to data centers, which are becoming a key customer for electric utilities and — many locals believe — jacking up electricity costs. The companies also have to figure out how to secure approval from at least six different regulators, in some cases appointed by governors and state legislators who are themselves trying to manage thorny AI politics. But if the deal goes through, it could set a new standard for how utilities are navigating the AI age and allow it to chase cheaper capital. The Trump administration’s appetite for deal-making has tempted railroad, food-services, and entertainment CEOs into striking combinations that wouldn’t previously have passed antitrust muster — the “endgame consolidation” we’ve written about before. NextEra and Dominion’s combination is bigger than any of those, and correspondingly thornier. — Rohan Goswami |

|

Joe Weisenthal is not an AI doomer |

Semafor/YouTube Semafor/YouTubeJoe Weisenthal responds to the dire predictions of what AI will do to jobs, wealth inequality, and even human literacy with the sunny curiosity that will sound familiar to listeners of Odd Lots, the hit finance show he co-hosts on Bloomberg with Tracy Alloway. “There’s going to be this sustained, if not growing, number of people who want to hear from people,” he said on the latest episode of Semafor’s Compound Interest show. He doesn’t see a future where his and Alloway’s bots are interviewing the guests’ bots on a free Odd Lots feed, with a paid premium version for listeners who want the real thing. (For one thing, AI can’t interrupt people, though that might be changing.) Weisenthal greeted news that Charles Schwab will provide AI financial advice to less wealthy people less as a warning sign of a two-tiered economy than a way to expand the pie of who gets financial advice. He’s also sanguine about AI’s effect on white-collar jobs, including his own: “I don’t think AI is still as good with numbers and finance as many of the hype people would say.” “A lot of the criticisms that people have towards the emerging AI world really just feel like descriptions of the past,” he said. “My impulse is to just try to not be too rigid in my expectations.” |

|

➚ BUY: Close friends. Xi Jinping and Vladimir Putin are meeting today in Beijing, with a long-delayed energy pipeline on the agenda. ➘ SELL: Closer enemies. Demis Hassabis, the founder of Google DeepMind, was an early investor in Anthropic. (Google competes fiercely with Anthropic, though Anthropic CEO Dario Amodei considers Hassabis a role model, the FT reports.) |

|

Companies & Deals- AI job watch: Standard Chartered plans to slash 15% of its workforce by 2030 as it replaces some roles with AI, which may be turning from an excuse for corporate layoffs into the real reason.

- Chipping in: Blackstone is fronting $5 billion to create an AI cloud company with Google, which will use the tech company’s chips to rival CoreWeave.

- Case closed: Elon Musk lost his case against Sam Altman for turning OpenAI into a for-profit, clearing the way for the AI giant’s much-anticipated IPO. “The reality is that everybody lost” in a case that “revealed the worst side” of Silicon Valley, Semafor’s Reed Albergotti wrote.

Watchdogs- Social capital: New York City Mayor Zohran Mamdani met with the CEOs of Goldman Sachs and JPMorgan, trying to thaw a frosty relationship with the business community. No word on whether Ken Griffin is taking the mayor’s calls yet.

- Boomerang economy: Australia ordered six investors with links to Beijing to sell their stakes in a rare earths firm, the latest sign of Western governments protecting key assets from Chinese influence.

- All bets are off: Minnesota lawmakers passed a bill to ban prediction markets in the state, the first in the country.

|

|

|