|

APRIL 21, 2026 |

|

Gen Z consumers are how much more likely than the average consumer to want financial advice from AI? |

|

A) 43% B) 53% C) 63% D) 73% |

|

|

Was this email forwarded to you? Sign up here. | | | |

|

ARTIFICIAL INTELLIGENCE |

|

|

|

More than half (55%) of US consumers used AI for financial tasks in the last 12 months, according to a Plaid study. |

|

AI is becoming part of the norm for financial tasks, and consumer uses are expanding. It is not just a research tool: 30% are using AI for recommendations and 33% for budgeting, investing advice, or to solve customer service issues. Half (52%) of consumers expect fintech apps to use AI, and 50% say managing money without AI would feel outdated. |

|

|

|

| | | |

|

BUY NOW, PAY LATER |

|

|

|

More than half (54%) of US buy now, pay later (BNPL) users say they wouldn’t have been able to make ends meet without installment loans, per a Lending Tree survey. That includes 62% of parents with young children who use BNPL and 59% of millennials who use BNPL. |

|

The share of BNPL users who pay for groceries with installments has doubled since 2024, rising to 29% of US BNPL-using households. Major BNPL for grocery users include Gen Zers (38%), parents (34%), and consumers making more than $100,000 (33%). |

|

|

|

| | | |

|

BANKING |

|

|

|

A newly released ServiceLink study reveals that home price offer and negotiation is the top stressor in the homebuying process (cited by 19% of buyers). But other factors are also bunched at the top, including understanding the paperwork (15%), the closing process (12%), and securing a good mortgage rate (12%). |

|

Some issues are related to general finances, including the down payment (which is tied to savings), securing a good mortgage rate (credit score, alternative credit, and income), and coming up with the fees and/or closing costs (savings again). |

|

|

|

| | | |

|

REPORT |

|

|

|

As payments reach ubiquity and differentiation collapses, growth is shifting to digital wallets that influence, orchestrate, and embed commerce across the customer journey. Banks and providers that move first will shape the next era of consumer engagement. This report explores the three shifts reshaping the wallet landscape, from payment utilities to commerce enablers, orchestrators, and, ultimately, ambient commerce. |

|

Key question: Where does growth come from after payments become a commodity, and how do wallets position themselves to capture it? |

|

Key stat: Mobile wallets are reaching saturation, with 76.5% of US smartphone users expected to use them by 2029. Wallet providers instead must look for growth in influencing where consumers shop, their payment method choice, and purchase management. |

|

(EMARKETER subscription required to read the full report) |

|

|

|

| | | |

|

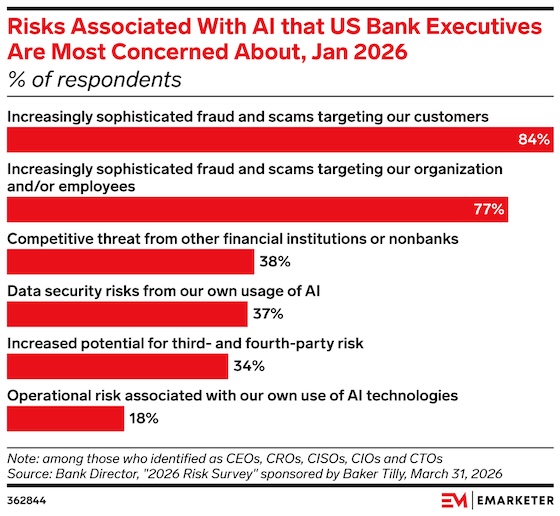

CHART OF THE WEEK |

|

|

|

Key stat: US bank executives are most concerned that AI will enable increasingly sophisticated fraud and scams targeting both their customers and their organization/employees, according to a January 2026 survey from Bank Director sponsored by Baker Tilly. | | | |

|