|

MARCH 31, 2026 |

|

Helping hand: In which area do lenders believe AI will have the strongest impact on their commercial lending process? |

|

A) Portfolio management B) Underwriting/approval C) Application/proposal D) Post-closing |

|

|

Was this email forwarded to you? Sign up here. | | | |

|

ARTIFICIAL INTELLIGENCE |

|

|

|

American Express recapped its 2025 highlights and laid out plans for agentic commerce readiness in its 2026 shareholder letter. |

|

CEO Stephen Squeri believes Amex is particularly adaptable to agentic commerce because of its: |

-

Membership model. Amex is betting on embedding its lifestyle and business assets into AI platforms and building its own AI infrastructure to ensure quality AI service for its cardholders.

-

Closed loop network. Amex has the advantage of control over its relationship with cardholders and merchants alike, with only Capital One boasting the same ability among major card networks. As agentic commerce scales, Amex envisions its richer insights into members’ preferences can drive more spending, loyalty, and retention with AI personalization. |

|

|

|

| | | |

|

REAL-TIME PAYMENTS |

|

|

|

Mastercard will sell the real-time payments segment that it acquired from Nets Group in 2019 for $3.2 billion, per the Financial Times. |

|

This decision puts the network on track to undo its largest ever takeover deal, and likely for a loss, a source told the FT. |

|

At present, the European-based real-time payment unit produces $370 million in annual revenues and $100 million in earnings before interest, taxes, depreciation, and amortization, per the same source. |

|

|

|

| | | |

|

SOCIAL COMMERCE |

|

|

|

Stripe will power a new checkout experience on Facebook, per a press release. |

|

Shoppers will be able to buy items in one click through Meta ads on Facebook, using credentials saved in their Meta wallet. Fanatics, Quince, and other brands are participating in the program. |

|

Instagram shoppable ads will launch in the near future. |

|

|

|

| | | |

|

REPORT |

|

|

|

AI-driven lending uses real-time signals to embed credit into digital journeys, expanding reach and personalization as alternative data broadens eligibility. This heightens risks around timing, borrower behavior, and control as credit becomes continuous and upstream in borrowing decisions. |

|

Key question: How are AI, embedded finance, and alternative credit models reshaping growth, pricing, and credit stability in US consumer lending? |

|

Key stat: Banks’ share of mortgage originations has fallen below a third as of 2024, per the most recently available data from the Consumer Financial Protection Bureau (CFPB)—reflecting how retail lending is shifting toward more distributed, point-of-sale channels. |

|

(EMARKETER subscription required to read the full report) |

|

|

|

| | | |

|

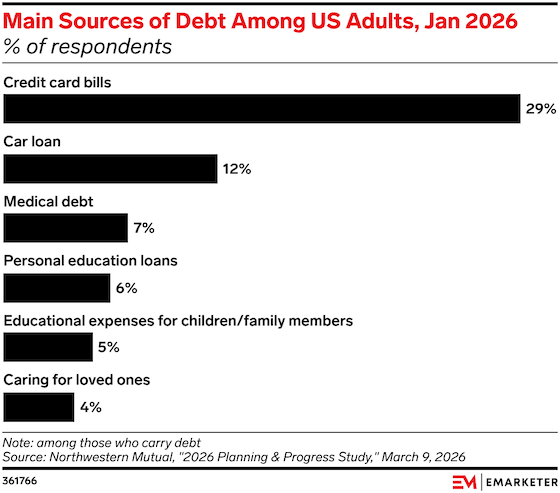

CHART OF THE WEEK |

|

|

|

Key stat: Credit card bills are the top source of debt among nearly a third (29%) of US adults, according to a survey from Northwestern Mutual and The Harris Poll. | | | |

|