| | Signals are piling up that the Trump administration’s “energy dominance” paradigm is reaching its li͏ ͏ ͏ ͏ ͏ ͏ |

| |  | | | CERAWeek Special Edition |

| |

|

- Low optimism, high prices

- Massive repair bill

- China’s peak demand

- Bullish on renewables

- Weak emissions target

Second-hand EV sales jump, and gas imports to Ukraine drop. |

|

Signals are piling up that the Trump administration’s “energy dominance” paradigm is reaching its limits. The message Energy Secretary Chris Wright is spreading at CERAWeek, for example, is a bit contradictory. On one hand, the war in Iran is “a short-term disruption” that shouldn’t worry consumers. Yet in closed-door meetings with energy executives in Houston this week, he and other US officials have prodded them to increase production, according to people with knowledge of the conversations. “‘Drill, baby, drill’ is a big part of energy dominance,” Jarrod Agen, who chairs the White House Energy Dominance Council, said during a side event here. “We haven’t heard any pushback on wanting to produce more.” But oil companies learned hard lessons during the shale boom of the 2010s about the risks of chasing short-term price signals, and more pushback could be coming soon. “We’ll have to see how this situation resolves itself, and when, and what are the leftover ramifications from that,” Clay Gaspar, CEO of independent driller Devon Energy, told the conference on Wednesday. “The one thing I know for sure is adding and subtracting rigs is absolutely value-destructive.” Beyond the uncertain price signal itself, the deeper issue is that energy dominance can ultimately cannibalize itself, Jeff Currie, chief strategy officer of energy pathways at private equity group Carlyle, told me: “The higher the volatility, the less incentive to invest, which then creates under-investment, which increases the volatility. It’s a vicious cycle.” There are other worrying signals: The oil market is now firmly in ‘backwardation,’ a condition in which near-term contracts are priced far higher than long-dated ones. That’s one indication that physical shortages, rather than bad vibes alone, are being priced in (the reverse effect happened during the pandemic, when spot prices plunged because of evaporating demand). And the widening spread between prices in Asia and those in the US means the US, with plenty of its own production, is increasingly an energy island, isolated from the global market. In one sense, that could be a sign “energy dominance” is working: The US can do what it wants and suffer relatively light consequences, and I doubt the White House will shed any tears about higher prices in China. But the market tightness is spreading, Currie said, and he predicted it will hit Europe by next week. That undermines the argument Wright has often made — that energy dominance offers protection to allies, too. |

|

Dwindling optimism, rising prices |

Alaa Al-Marjani/Reuters Alaa Al-Marjani/ReutersOil prices swung back above $105 a barrel amid signs of protracted disruptions to global energy flows and dwindling optimism of a ceasefire. Tehran dismissed the 15-point US proposal to pause the war and issued its own counterproposal. The economic fallout from the conflict is biting, with fuel shortages spreading worldwide and companies grappling with the consequences of rising prices and disrupted supply chains. Analysts have revised down the global LNG outlook for this year. Iraq’s oil production has plummeted as the country is unable to export crude through the Strait of Hormuz and storage levels are reaching capacity. Meanwhile, Reuters estimates that at least 40% of Russia’s oil export capacity is at a halt following Ukrainian attacks on energy infrastructure and the seizure of tankers. The Trump administration is looking at what the fallout for the economy could be if oil prices spiked as high as $200 a barrel, according to Bloomberg, though the White House has denied it is doing so. |

|

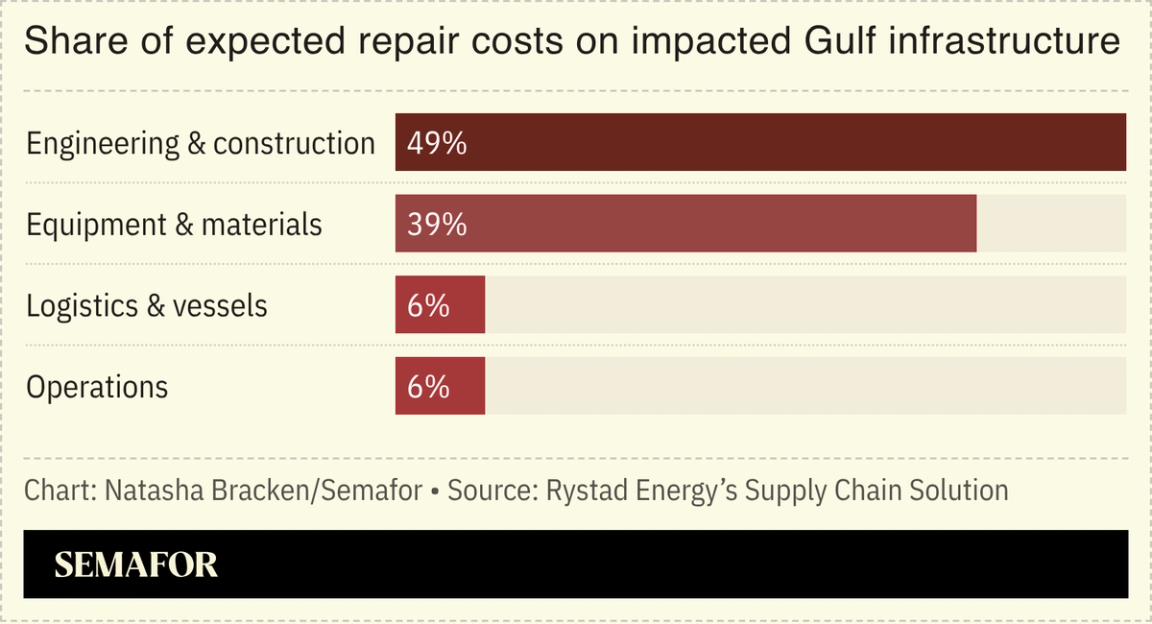

Repair costs from reported damage and shutdowns hitting fossil fuel infrastructure in the Middle East could amount to at least $25 billion. Rystad Energy expects the bill for restoring LNG trains, refineries, fuel terminals, and key gas-to-liquids facilities to climb even further, largely driven by engineering and construction costs, and to a lesser extent by equipment and materials. The costliest attack hit Qatar’s Ras Laffan Industrial City, where the destruction of LNG trains has reduced capacity by 17%, and full recovery will likely take five years, as the gas turbines needed to power LNG main refrigeration compressors were already in high demand for data center electrification and coal plant retirements. “The Gulf region’s recovery will be defined less by financial capital and more by structural constraints,” said Audun Martinsen, the head of supply chain research at Rystad Energy. “While some assets may be restored within months, others could remain offline for years.” |

|

China’s oil demand could peak sooner than expected, a senior executive at a major state energy firm said, as the Iran war accelerates the turn away from fossil fuels. The country is the world’s second-largest oil consumer, but demand growth has slowed as it shifts to EVs and renewables. CNOOC’s deputy chief economist doubled down on the risks associated with relying too heavily on a single source of energy, especially as rising prices caused by the effective closure of the Strait of Hormuz hit countries dependent on oil imports the most: Hong Kong’s aviation giant Cathay Pacific, for example, said Thursday it was raising fuel surcharges on all flights by 34% to compensate for rising oil costs. Similar dynamics are playing out elsewhere: Used EV purchases in Europe are up as fuel prices rise; one French retailer told Reuters that it doubled EV sales between February and March. And a UK electricity firm boss said solar panel sales had risen 50% since the war began. |

|

| |  | Tim McDonnell |

| |

Daniel Cole/Reuters Daniel Cole/ReutersSome of the largest renewable energy investors are still bullish about the US market despite antagonism from the Trump administration. Private equity giant Brookfield on Wednesday spent $6.5 billion, alongside Caisse de Depot et Placement du Quebec, to acquire the Canadian renewable energy company Boralex, which has a 4-gigawatt pipeline of projects under development globally, including many in the US. Meanwhile, Sandhya Ganapathy, CEO of EDP Renewables North America, told Semafor at CERAWeek that the company plans to increase the US share of its global capex from 45% to 60% in the next few years, representing $5 billion in new project investments. Much of that is driven by data centers. “I’ve been doing this for more than 15 years, and I’ve never seen demand this good,” she said. “It’s a fantastic time to be on the generation side in spite of all of the policy challenges and the backlash that we have.” The biggest obstacles now, she said, are slow permitting and an underdeveloped grid. That view was shared in a separate interview with Andrew Flanagan, CEO of RWE Americas, which said last week it will plow $20 billion into new renewables and gas projects in the US. “The US is still a great market,” Flanagan told Semafor. “We take a long-term view, and we can’t overreact to the short-term variability in policy.” |

|

This April, Howard Lutnick, US Secretary of Commerce, will join global leaders at Semafor World Economy — the largest gathering of top CEOs and officials in the United States — to sit down with Semafor editors for conversations on the forces shaping world markets, emerging technologies, and geopolitics. See the full lineup of speakers, including Global Advisory Board members, Fortune 500 CEOs, and officials from the US and across the G20. |

|

Amit Dave/File Photo/Reuters Amit Dave/File Photo/ReutersIndia’s much-delayed 2035 climate plan underestimates the country’s clean energy potential and allows for an acceleration of emissions growth, according to analysts. The plan aims to reduce the emissions intensity of its GDP by 47% from 2005 levels and increase the share of its electricity capacity from nonfossil sources to 60% by 2035. The reduced carbon intensity target would, however, still allow India’s carbon emissions to increase by 70% over the next decade if GDP grows at a target rate of 7% per year, Lauri Myllyvirta of the Centre for Research on Energy and Clean Air told Semafor. That would translate to emissions growth of 5.5% per year, above the average rate of 3.5% over the past decade. India is also on track to achieve its clean power capacity target well ahead of time: Its Central Electricity Authority projects that nearly 70% of power capacity will come from nonfossil sources by 2035-36. “India’s booming clean energy industry is highly likely to deliver much faster progress than policymakers were prepared to commit to,” Myllyvirta said. Disruptions to oil and gas flows caused by the Iran war and the competitiveness of clean energy could strengthen the case for accelerating renewable deployment. |

|

New EnergyFossil Fuels - Several African countries, including Kenya and Uganda, face fuel shortages within weeks as heavy reliance on energy imports leaves them vulnerable to oil and gas supply disruptions, while producers such Algeria, Angola, and Nigeria may benefit from higher oil prices.

- Europe could face an energy and fuel shortage as soon as next month if the Strait of Hormuz doesn’t reopen to oil and gas shipping, warned Shell’s CEO Wael Sawan.

- The UK has allowed its military to board and detain Russian ships entering its waters, which London says are part of a shadow fleet that allows Russia to export oil despite sanctions. The UK government has also blocked a £1.5 billion Chinese wind farm in Scotland over national security concerns.

Finance- A growing number of ESG-focused funds are being liquidated in the US, with 91 shutting down last year and just nine new ones launching.

- The US has caused $10 trillion worth of global climate damage since 1990 — a quarter of which it inflicted on itself, researchers at Stanford University have found.

Tech- Traders in Europe are turning to AI and machine learning to forecast the weather and profit from anticipating the next shift in temperatures before gas and power prices change.

Politics & Policy |

|

|