Asia's big manufacturing economies are heavily exposed to imported energy products from the Middle East, so both the price rise and supply uncertainty caused by the conflict are alarming.

However, there were tentative signs that markets elsewhere are taking a breather, as investors await further developments. Both U.S. and global Brent crude oil prices were but held below Tuesday's 8-month and 19-month highs, respectively.

Europe's stocks popped up about 0.5% in what after two days of heavy selling. U.S. stock futures were marginally higher too. And the dollar's rise flattened out for the most part, even though government bond yields continued to push higher.

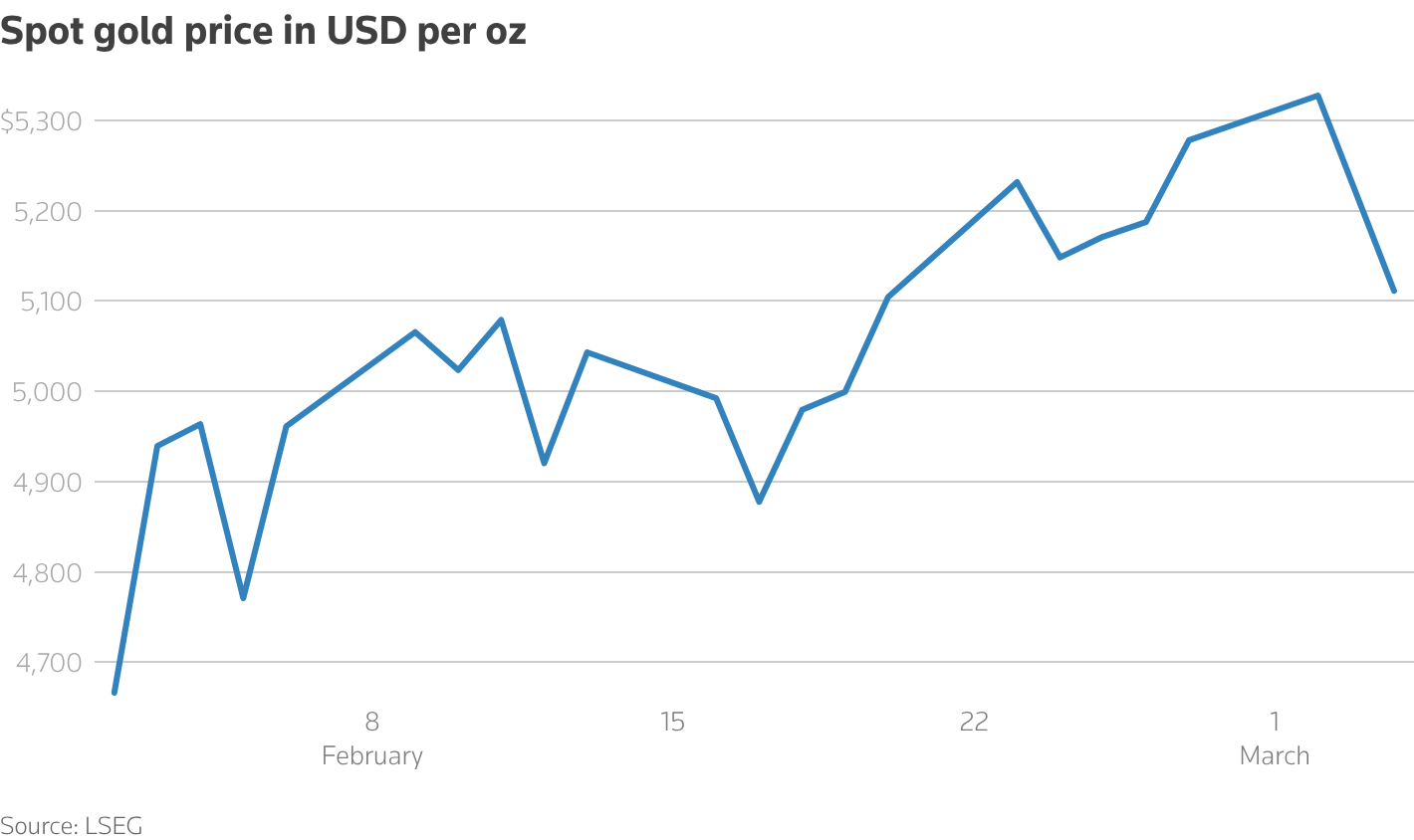

Gold and precious metals, unexpected losers this week during the geopolitical shock, on Wednesday as the dash for cash abated somewhat.

President Trump announced shipping insurance and possible naval support for energy supplies to exit an effectively closed Gulf - and that may be helping at the margins, although these moves could take some time to have an impact. World markets asking when this energy blockage will abate are having to think in weeks rather than days.

The conflict in Iran and across the region is impossible to predict. Many are now focusing on as Supreme Leader following the killing of Ayatollah Ali Khamenei last weekend. Some in markets took heart from a New York Times story that said Tehran officials had made a to Washington over the weekend on how to end the conflict.

But for investors who think the coast will be clear once Gulf tensions ease, there are plenty of other things to worry about. For one, there’s about private credit funds run by the likes of Blackstone and BlackRock.

Today's calendar sees more routine issues back on the radar, with the ADP's private sector jobs report and ISM's service sector survey both coming out. The former may be looked at more closely in light of the big U.S. payrolls report due on Friday.

And with that, onto today's column.