| | In today’s edition: Dubai builds a global aircraft leasing giant and Japanese cultural icons mint fo͏ ͏ ͏ ͏ ͏ ͏ |

| |  | | | Global Capital Edition |

| |

|

- Dubai’s plane leasing giant

- Finstreet tackles transparency

- Private credit’s Gulf moment

- Emerging markets surge

Japanese cultural icons like Hello Kitty mint fortunes. |

|

Saudi Arabia posted its deepest quarterly deficit in five years, pushing the 2025 shortfall to 5.5% of GDP. Spending is being reprioritized, megaprojects trimmed, and global oil supply is expected to outpace demand, bringing up echoes of 2015. But this time, it is different. Back then, as crude collapsed and spending surged, Crown Prince Mohammed bin Salman’s team concluded the kingdom could go “completely broke” by 2017. Saudi Arabia was burning through $30 billion a month in reserves. The response — strict spending controls, subsidy cuts, sales tax, and tapping debt markets — stabilized the country’s finances. Now, non-oil revenue makes up a larger portion of government income. It hit 122.6 billion riyals ($32.7 billion) last quarter — nearly matching what the kingdom generated in an entire year a decade ago. Foreign reserves climbed to a six-year high of 1.78 trillion riyals in January. Debt is rising, but from a low base. And capital is still flowing outward: last week, Public Investment Fund’s AI platform HUMAIN said it committed $3 billion to xAI ahead of its SpaceX merger. The US standoff with Iran is also a plus, adding around a $10 premium to oil and helping cushion what was expected to be a supply glut. This sweet spot is fragile. A conflict that disrupts the Strait of Hormuz, through which a fifth of global oil passes, would spike prices while stranding Gulf barrels. If diplomacy prevails, supply and demand will return as the main factors in the oil market, and the Saudi deficit — along with the bottom lines of its Gulf peers — will weigh more on global capital flows. |

|

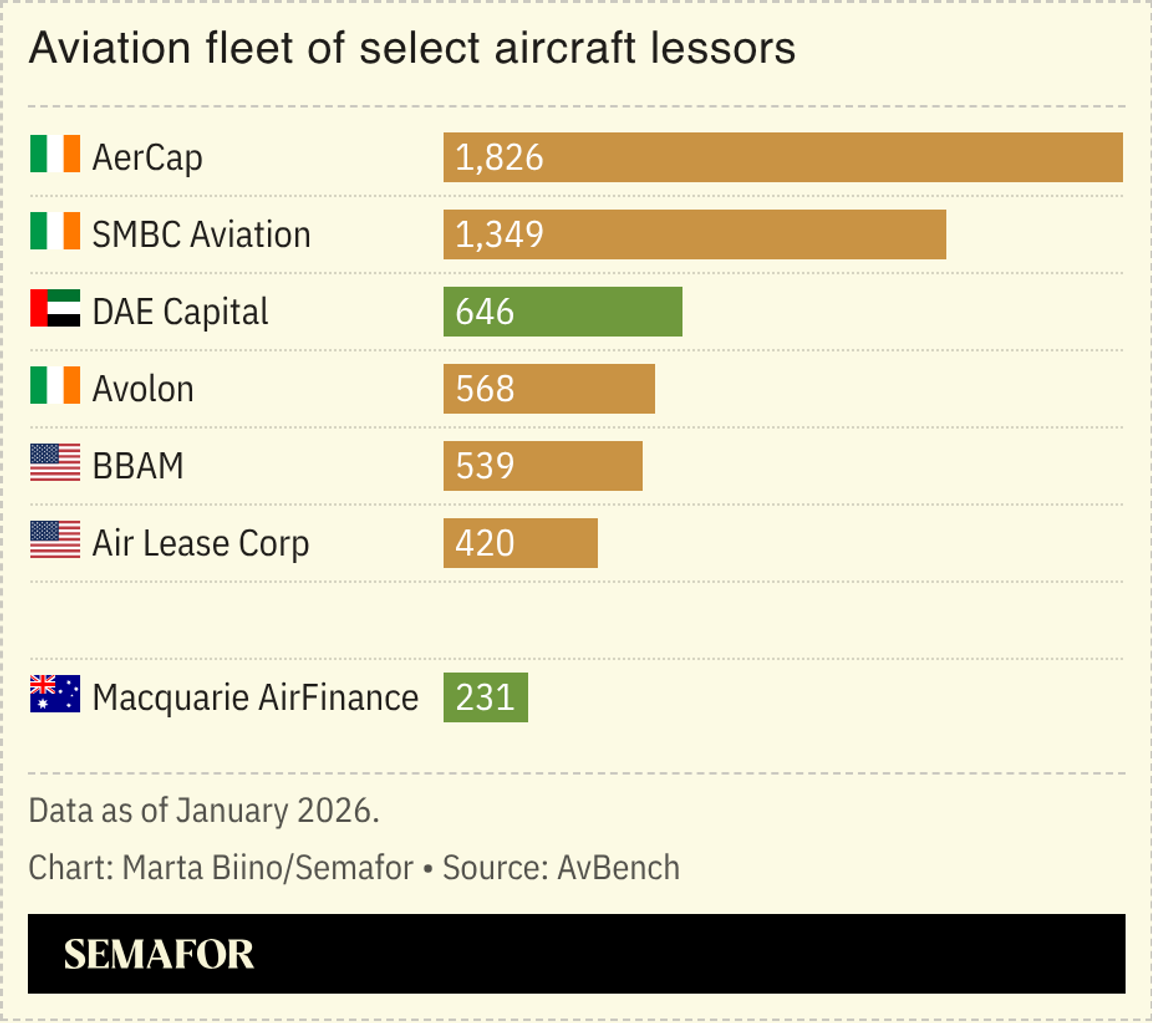

Dubai aircraft lessor climbs global ranks |

DAE Capital is reportedly closing in on a deal to buy Macquarie AirFinance as it seeks to join the world’s top aircraft lessors. The Macquarie unit is valued at about $6.4 billion. Other bidders included Saudi Arabia’s AviLease and Qatar’s Lesha Bank, Reuters reported. Dubai Aerospace Enterprise — owned by the Investment Corporation of Dubai, the emirate’s sovereign wealth fund — is the world’s third-largest aircraft lessor and, like its peers, has expanded through acquisitions. The Macquarie AirFinance deal is part of a consolidation wave that has swept the industry. With Boeing and Airbus struggling to meet airline demand, aircraft values have surged, allowing mid-sized lessors to command premium prices, according to the Irish Times. Over the past two decades, the Gulf has built a global aviation hub linking Asia, Europe, and the US. Regional carriers — led by Emirates, Etihad, and Qatar Airways — have ordered more than 1,500 jets. While the region is known for operating the largest aircraft, demand for smaller planes is rising as short-haul travel grows. In its latest forecast, Airbus said Saudis took an average of 1.5 flights in 2024 and expects that figure to double by 2044, overtaking Americans and Europeans. — Mohammed Sergie |

|

Finstreet at the private capital crossroads |

ADGM in Abu Dhabi. Courtesy of ADGM. ADGM in Abu Dhabi. Courtesy of ADGM.Fintech startup Finstreet, backed by Sheikh Tahnoon bin Zayed’s International Holding Co., wants Abu Dhabi to be the crossroads in the global rush into private capital, offering regulated guardrails in an increasingly crowded market that remains opaque. An estimated $600 billion in private assets across Asia, Europe, and the Middle East are seeking exits, Finstreet co-founder and CEO Sunidhi Pasan told Semafor in an interview. To tap into that dry powder, Finstreet is providing a regulated venue where private assets can be issued, held, settled, and traded more easily. Launched two years ago, the startup aims to provide long-term investors — sovereign wealth funds, large family offices, and institutional asset managers — a more transparent way to manage liquidity, adjust exposure, and redeploy capital without relying on one-off bilateral deals. With a front row seat from its offices in Abu Dhabi’s financial hub ADGM, Pasan sees an opening: Finstreet — working with the likes of BlackRock and Franklin Templeton to develop products — can be a place where buyers and sellers transact, shifting Abu Dhabi from capital allocator to intermediary. Whether that vision materializes will depend on attracting trading volume, Pasan acknowledged, not infrastructure alone. — Kelsey Warner |

|

Gulf on both sides of private credit |

Hamad I Mohammed/Reuters Hamad I Mohammed/ReutersThere may be questions over the health of the private credit market globally, but there’s still plenty of interest from both borrowers and investors in the Gulf. Abu Dhabi’s Aldar Properties recently raised $1 billion from New York-based Apollo Global Management, and Qatar Investment Authority (QIA) is backing 5C Investment Partners, run by two former Goldman Sachs partners. The expansion is in contrast to the strain hitting parts of the private credit industry globally. Firms are taking longer to raise capital, and the shares of major players like Blackstone and KKR have been on the slide after Blue Owl’s decision to halt redemptions on one of its funds sparked a sector sell-off. QIA recently struck a deal with Goldman Sachs worth up to $25 billion for access to private credit and other deals. In Abu Dhabi, Ruya Partners is targeting $400 million for a private credit fund, while climate-focused ALTÉRRA is raising $1.2 billion for deals. — Dominic Dudley |

|

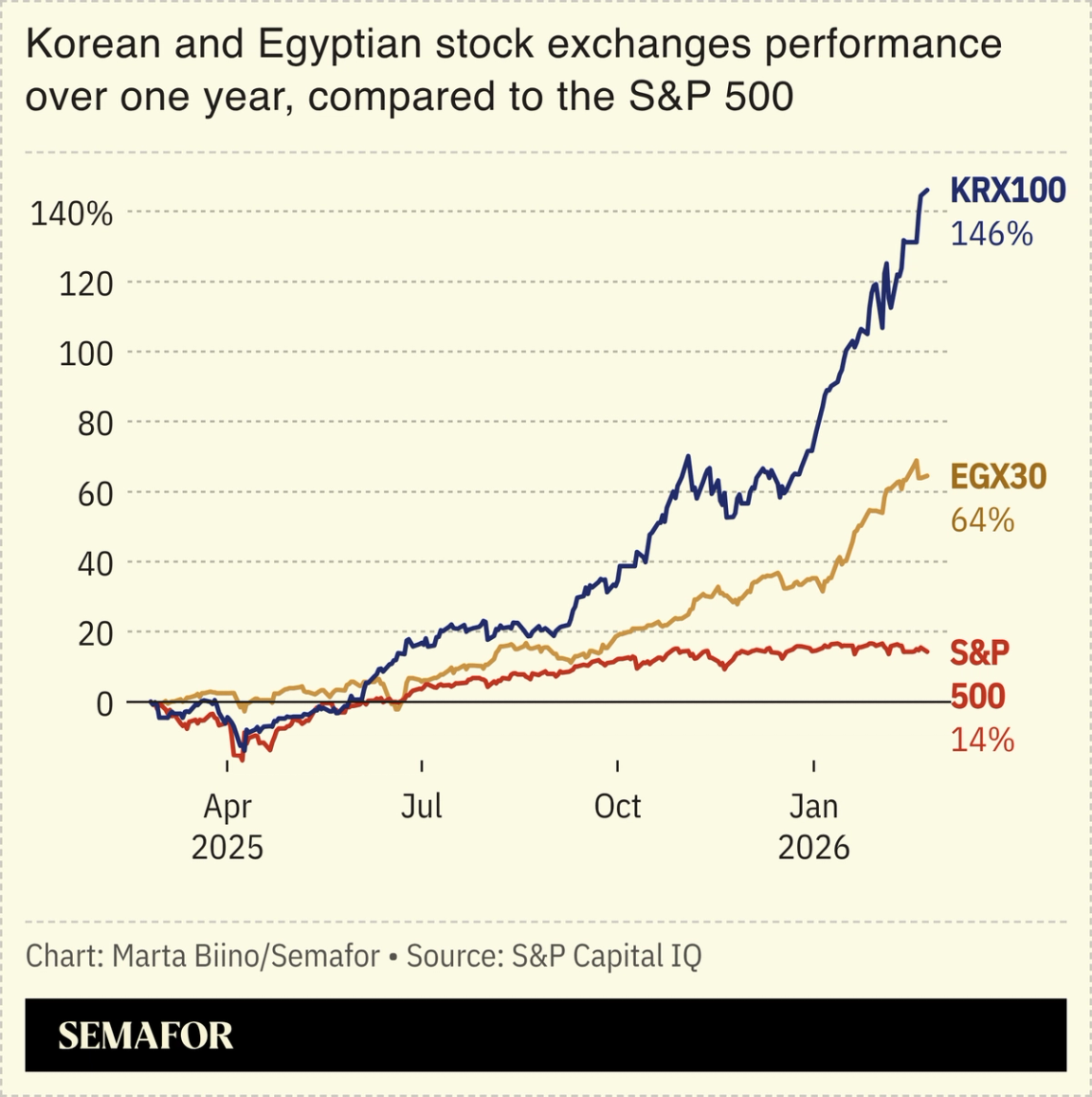

Two places where investor optimism is prevailing: Egypt and South Korea. Egypt’s benchmark stock index is racing ahead of other emerging markets, driven by investor enthusiasm for the government’s efforts to revive the economy. The EGX30 index is up 27% in dollar terms this year, more than double the gain of the MSCI EM equity index, Bloomberg reported. That bullish feeling has been going on for over a year: The benchmark returned 50% for dollar investors in 2025 as efforts to lower inflation and attract foreign investment — sourced largely from the Gulf — are bearing fruit. Meanwhile, the one place where AI ebullience is lingering is South Korea, where key suppliers hail from. During a cabinet meeting last month, South Korean day trader-turned-President Lee Jae Myung said that the long-undervalued capital market is “reemerging as a solid foundation for the growth of future innovative industries and for the healthy accumulation of national wealth.” |

|

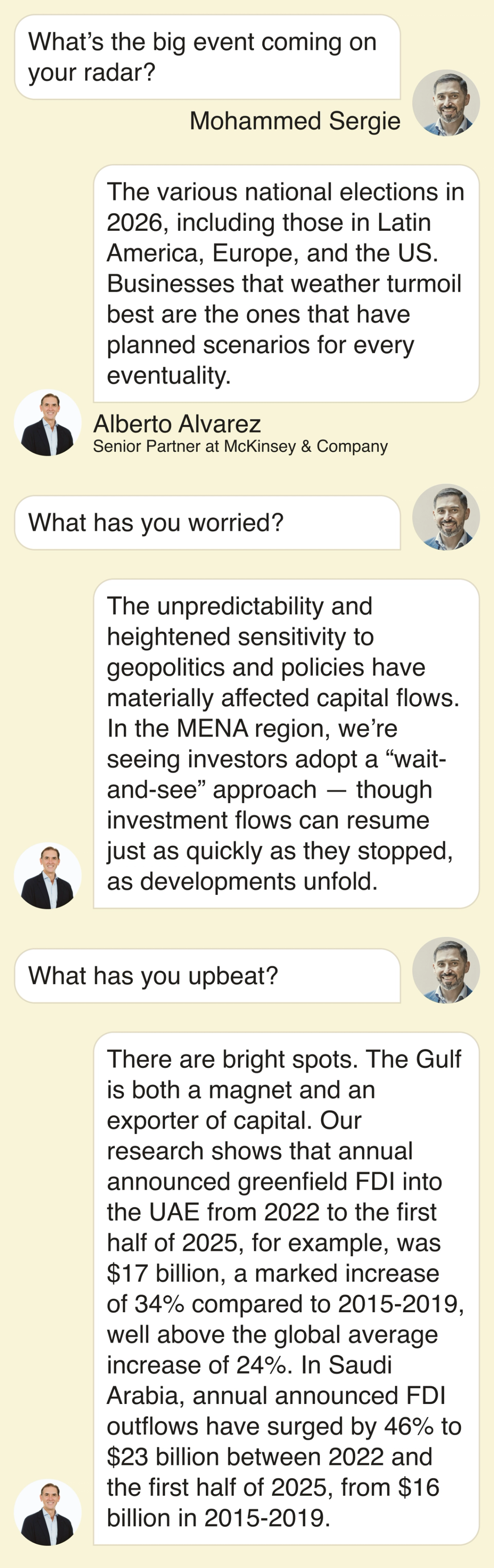

Every week, we ask a different expert what they’re focused on. Today, we’re talking to Alberto Alvarez, senior partner at McKinsey & Company.  |

|

@hellokittyspadubai/Instagram @hellokittyspadubai/InstagramJapanese entrepreneurs have turned cute into wealth. From Hello Kitty to Demon Slayer, characters have become massive assets — and have minted many Japanese billionaires, according to Bloomberg’s latest rich list. Japan’s content exports now exceed semiconductors, and only lag cars. The intellectual property has spawned films, theme parks, and an endless array of gadgets, gizmos, and textiles, potentially compounding riches for decades. The Gulf is a major consumer: Hello Kitty products fly off the shelves and a themed spa in Dubai has 35,000 followers on Instagram. As the region gains global cultural relevance, the question is whether it can follow Japan and turn pop culture into serious industry. One example of a global craze is Dubai chocolate. It has surfaced in Japan and South Korea — as a mochi version — but the treat lacks the IP protection to generate wealth for its original creators. |

|

|