|

MAIN FEATURE

The Financial Planners Who Didn't Realize They Could Retire NOW

A couple flew in from the East Coast. They run a financial planning business.

They came to learn how to optimize a couple small things. But on day two they came in beaming.

The husband said, "Last night we were double checking some of the numbers we ran during the day, and we realized we can actually retire right now."

I was so excited for them. They came looking for some little tweaks and left knowing they never have to work again.

The awesome part was that they're not taking their foot off the gas. They were more fired up than ever to help their clients. They said they realized they've been using the wrong retirement model the whole time, and now they want to share this new model.

Here's how the new model worked for them, and how you can use it too...

They had assets. But everything was locked up. Retirement accounts they couldn't touch. Home equity doing nothing. A portfolio they never considered borrowing against.

They were asset-rich but control-poor.

So we ran the numbers. We mapped out their liquidity layers. We stress-tested drawdown scenarios.

I showed them how if you borrow against assets that appreciate faster than your cost of debt, and you roll that debt annually, you can access liquidity indefinitely. Without ever selling, without ever triggering taxes, without ever resetting compounding.

That's the game.

Here's the simple version:

Let's say you own $1 million in Bitcoin.

You borrow $150,000 against it.

Bitcoin has been averaging 50% per year. So in year 2 it's worth $1.5M.

Now you borrow $300,000, you pay off the original $150,000 and pay off the rest.

In year 3 you have $2.25M of Bitcoin, you borrow $450,000, pay off the $300,000 of debt, and live off the rest.

You roll the debt every year. And as long as the asset appreciates faster than the cost of borrowing, you can do this forever.

In fact you can pass on your assets, and your debt, to your kids.

By this point you'll be giving them tens of millions of dollars of debt... but against hundreds of millions of dollars worth of Bitcoin.

It's not that you're piling up infinite debt. You're renting liquidity against an asset that's growing faster than the cost of that liquidity.

The compounding never stops. The tax bill never comes. The balance sheet never shrinks.

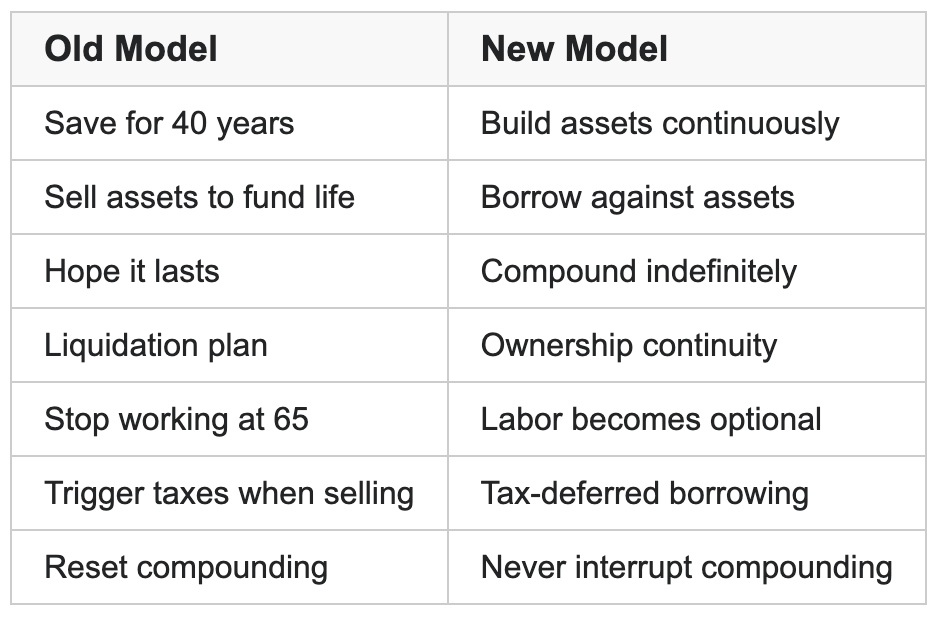

Compare that to the traditional model:

If you sell $150,000 of Bitcoin to fund your lifestyle:

- You lose the asset – your compounding base shrinks to $850,000

- You trigger taxes – capital gains take 20-30% ($30-45K immediately)

- You lose the future – that $150K would have been worth $7.6 million in 10 years at 50% growth

Selling resets everything. Borrowing preserves everything.

The new model: Own assets. Borrow against them. Never sell.

|