|

|

|

|

Oh, hi again. And welcome to the beginning of your long weekend. We have a special guest for today’s newsletter. Please give him a warm welcome. |

|

|

|

|

Rolling out the red carpet |

|

|

|

|

In case you haven’t noticed, The Globe’s personal finance team has grown over the past year or so. I joined the desk, along with consumer affairs reporter Mariya Postelnyak. Most recently, we’ve been lucky enough to add Andrew Galbraith to the mix. |

|

|

|

|

Andrew is our new investment reporter, and boy, has he joined at a great time. He’s stepping in at a moment when Canadians are clearly hungry for smart, independent investing coverage that informs, without the fear of being sold something. I chatted with Andrew to help readers get a sense of what to expect from his reporting. Here’s our conversation: |

|

|

|

|

|

|

|

|

|

Andrew Galbraith, the Globe and Mail’s investment reporter. Fred Lum/The Globe and Mail

|

|

|

|

|

Q: Andrew, can you tell us a bit about your background before joining The Globe? |

|

|

|

|

A: Hey Meera! Thank you for inviting me to your newsletter, which I hope means I’m guaranteed to retire rich. I’m new to The Globe but also, in a way, to Canada. I’ve spent most of my professional life in Shanghai, where I covered the Chinese bond market for Reuters, and earlier worked at Dow Jones Newswires and at a magazine called China Economic Review. My family got caught in the Shanghai COVID lockdowns in 2022, which is when we decided to move to Vancouver. I’ve spent time away from journalism over the years, most recently running a small investment research firm. But I’ve tried all along to focus on making complex topics clear and accessible. |

|

|

|

|

Q: What kinds of stories do you want to dig into on the beat? |

|

|

|

|

A: The stories that most appeal to me are ones that show how global market moves affect the real world, and which I hope give readers something to think about as they consider their own finances. My recent story on how volatility in silver prices has affected coin collecting was a fun one. |

|

|

|

|

Q: The Globe has a pretty savvy investing audience, but also a lot of newbie retail investors who are eager to learn. How do you see your coverage appealing to people in different stages of their investing journeys? |

|

|

|

|

A: I think an ideal story should appeal to both newbies and veterans. There should be stuff in there that’s compelling for people who are plugged in, maybe an interesting pattern or data point from an obscure corner of the market. But it should be written in an accessible way that connects the dots and offers useful ideas for newer investors. So yeah, I might write about speculation in ornamental gourd futures, but I’ll go into it asking, “why should a Canadian investor care? Why does this matter?” |

|

|

|

|

|

|

|

|

Q: What’s one interesting thing you’ve learned about the beat so far? |

|

|

|

|

A: It has been interesting to hear people talk about “the way things are done here” across industries and in financial markets, with the implication that Canada is inherently different. I’ve also enjoyed talking with people involved in finance, but who work far away from Bay Street. While it may seem odd to write about investment three time zones removed from Canada’s financial centre, I think being based in Western Canada gives me a really interesting opportunity to hear different viewpoints. |

|

|

|

|

Q: There’s a lot of traditional investing advice out there, such as “time in the market beats timing the market.” What’s a piece of investing advice that rang true for previous generations, but may not work for people getting into investing today? |

|

|

|

|

A: If I can flip that around, I think a piece of advice that may be more relevant for newer investors is to focus on reducing liabilities rather than trying to boost assets. For older investors who lived through the 15- to 20-per-cent mortgages of the early 80s, rates might still seem pretty low, but 5 per cent interest adds up. That’s especially true if you consider that equity market returns, which have been fantastic, tend to revert to the mean over the long term. |

|

|

|

|

Q: If readers want to reach you, how should they do that? What should they message you about? |

|

|

|

|

A: The best ways are to send me an e-mail at agalbraith@globeandmail.com or find me on LinkedIn, if that’s your thing. But please tell me why you want to connect! Send me your investment ideas, your questions, and your (preferably egg- and dairy-free) weeknight recipes. |

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

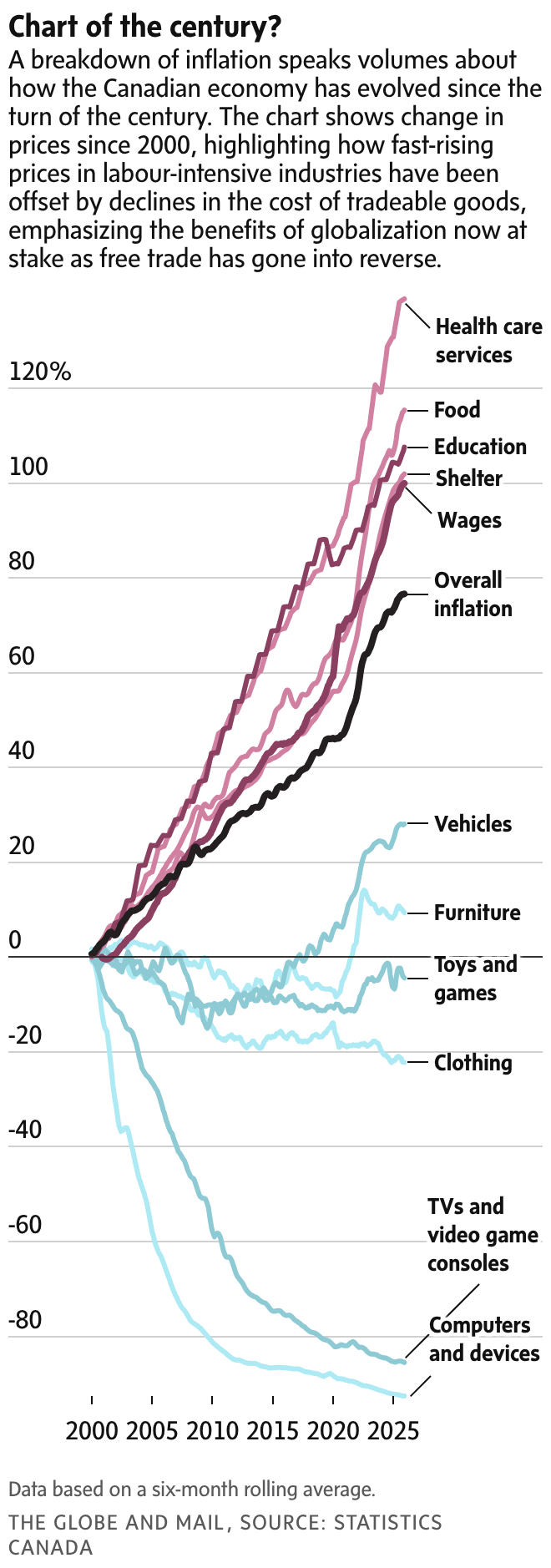

What’s happening: Tradeable goods such as electronics and clothing have barely risen in price – some prices have fallen sharply – over the past 25 years, while non-tradeable services such as shelter and education have surged far faster than overall inflation. Since 2000, prices overall are up about 76 per cent, but the pain is concentrated in essentials. |

|

|

|

|

What they’re saying: Inflation over decades can sting, and that is an important lesson for retirees, who generally need to plan for about 25 years of post-career finances, says Doug Porter, Bank of Montreal chief economist. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The situation: Frank, a retired investor in his 70s, has poured his entire $83,500 in TFSA contributions into a single stock: BlackBerry. Despite years of conviction and continued support from a high-profile investor, his account is down roughly $20,000. |

|

|

|

|

How he approached it: Financially secure with a pension, home equity and diversified registered accounts, Frank treated his TFSA as higher-risk capital. He did his research, believed in the company’s turnaround story and kept adding to his position over more than a decade, accepting the volatility along the way. |

|

|

|

|

Yes, but: Even if the money feels like “fun money,” concentration risk is real. Behavioural traps, such as focusing on a stock’s past glory or hoping to break even, can cloud judgment. For most investors, especially in retirement, a TFSA’s tax-free growth is too valuable to hinge on a single company’s comeback. |

|

|

|

|

|

|

|

|

|

|

|

|