|

|

|

|

In my last newsletter from a couple of weeks ago, I linked to a sample retirement plan that financial planner Robb Engen had published on his site. One reader got in touch with a question that, I thought, deserved a thorough answer. |

|

|

|

|

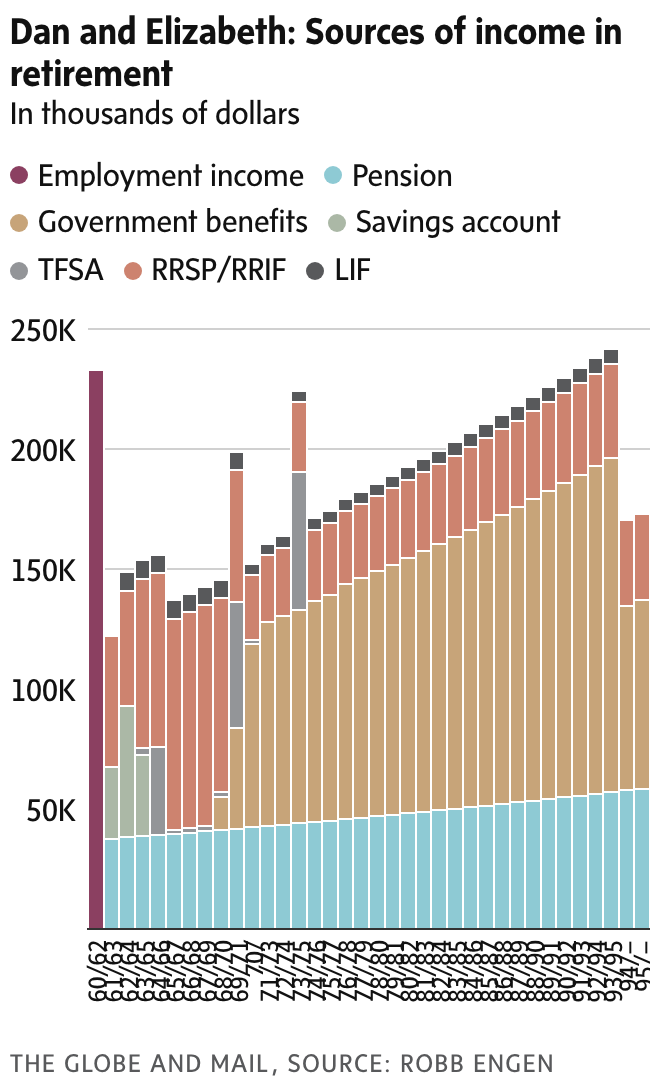

The sample plan features Dan and Elizabeth, a couple in their early 60s who are about to retire. It assumes Dan will die at age 95, which is a reasonable supposition. At 60 years old, Canadian men have a 25 per cent chance to make it to 94. |

|

|

|

|

But what happens, the reader wondered, if Dan defies the prognostications of the actuarial tables and goes on to live much longer? Does the couple risk running out of money? |

|

|

|

|

The short answer is, no – one big job of a retirement plan is to make sure your money lasts as long as needed. So, first, let’s take a look at how that happens in this example. |

|

|

|

|

|

|

|

|

Turning your retirement savings into lifetime income |

|

|

|

|

The chart below shows Dan and Elizabeth shifting from relying heavily on withdrawals from their investments in the earlier years of retirement to depending mostly on employer pensions and government retirement benefits later on. |

|

|

|

|

|

|

The plan is for both of them to defer their Canada Pension Plan (CPP) and Old Age Security (OAS) payments until age 70. This means that, in the first few years, they can draw plenty of taxable income from their investments without worrying that CPP and OAS, which are also taxable, will bump them into a higher tax bracket. |

|

|

|

|

But, crucially, it also means that, from age 70 on, their retirement is mostly funded by sources of income – pensions and benefits – that are guaranteed for life. |

|

|

|

|

(You’ll notice a couple of large withdrawals from the couple’s tax-free savings account: Those are to cover one-off expenses such as a new vehicle purchase and a home renovation. It makes sense to use a TFSA for those because those funds are not taxable.) |

|

|

|

|

By deferring CPP until age 70, the couple will get 42 per cent more than if they’d started it at 65. Similarly, by delaying OAS, they stand to get 36 per cent more. Those are big boosts to payments that will last as long as Dan and Elizabeth will. |

|

|

|

|

Not only that, but CPP and OAS are adjusted for inflation. Many employer pensions also guarantee at least some protection from rising prices. This means less worrying about keeping up with the cost of living. |

|

|

|

|

|

|

|

|

|

|

I called Mr. Engen to discuss a few of the “what if” questions I’m sure he gets frequently from clients. Here’s the big one: What if Dan, Elizabeth or both of them, need at-home care or to move to a long-term care facility in the last year of retirement? |

|

|

|

|

In this example, the couple have hundreds of thousands of dollars in their tax-free savings accounts by the time they hit their 80s. They’ve only used those savings for rare, one-off expenses, kept the money invested and restarted contributing to those accounts later in retirement. |

|

|

|

|

Their retirement plan also intentionally excludes as sources of income a small inheritance Dan and Elizabeth expect to receive and their paid-off home. Those, along with the TFSAs, can be used to deal with late-in-life spending spikes, Mr. Engen said. |

|

|

|

|

More ‘what ifs’: Some clients may have a few centenarian ancestors, what would happen if they also lived to 100 and beyond? Or, at the other end of the longevity-concerns spectrum, what if they died in their mid-70s? |

|

|

|

|

Mr. Engen said he often gets those questions and will run the numbers to show what would happen in different reasonable scenarios. |

|

|

|

|

In general, a plan drawn up when clients are about to retire is a starting point. It can be tweaked as the years go by and things change, he added. |

|

|

|

|

The second, and often forgotten, job of a retirement plan |

|

|

|

|

Hopefully this post gives you a better idea of how financial planners work with assumptions and stress test their strategy against life’s inevitable surprises. |

|

|

|

|

Here’s one last thought. One important job of a retirement plan is to ensure you don’t run out of money. The other is to show you how far your hard-earned savings can go, so you’re not underspending unnecessarily. |

|

|

|

|

As Mr. Engen puts it, running the numbers is also about helping you live your best retirement, at least money-wise. |

|

|

|

|

Subscribe to the On Money newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for On Money here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| The end of the starter home

Back in March of last year, I wrote about how falling condo prices meant many young people who’d bought them as starter homes couldn’t upsize.

About a year later, not much has changed. | | |

| BMO fined over fees

Canada’s federal financial watchdog just slapped BMO with a $4-million fine for charging clients millions of dollars in monthly fees that should have been waived or reduced. A good reminder to double-check your bank statements. | | |

|

Travel to Cuba

Donald Trump is the reason many Canadians have crossed off Florida and Arizona from their list of sun destinations. That may now extend to Cuba as well. Ottawa updated its Cuba travel advisory this week, warning of prolonged power outages, along with shortages of food, water and medicine that can also affect resorts. The country’s economy was already in a deep rut. But things have gotten worse since the U.S. moved to cut fuel supplies to the island earlier this year. The country only has 15 to 20 days worth of oil left, according to The Financial Times. |

|

|

|

|

|

|

|