The trigger for the ongoing selloff in global software stocks was actually news from last Friday that AI firm Anthropic had launched a new AI “agent” for automating work tasks. The fact that it took almost two full trading days to land shows how much it blindsided investors, even though recent months have seen markets discriminate much more ruthlessly between winners and losers from AI in the digital and tech space.

Alphabet's results after Wednesday's bell will test the mood further. After major Wall Street indexes lost about 1% or so on Tuesday, Nasdaq futures remained in the red early today. Around the world the tech herd was similarly scattered, with hardware and chip firms in Asia continuing to do well but software firms in India also getting caught in the downdraft.

Elsewhere, European pharma giant Novo Nordisk slumped almost 20% after the Wegovy maker warned about this year's profit outlook amid fierce competition in the weight-loss drugs world.

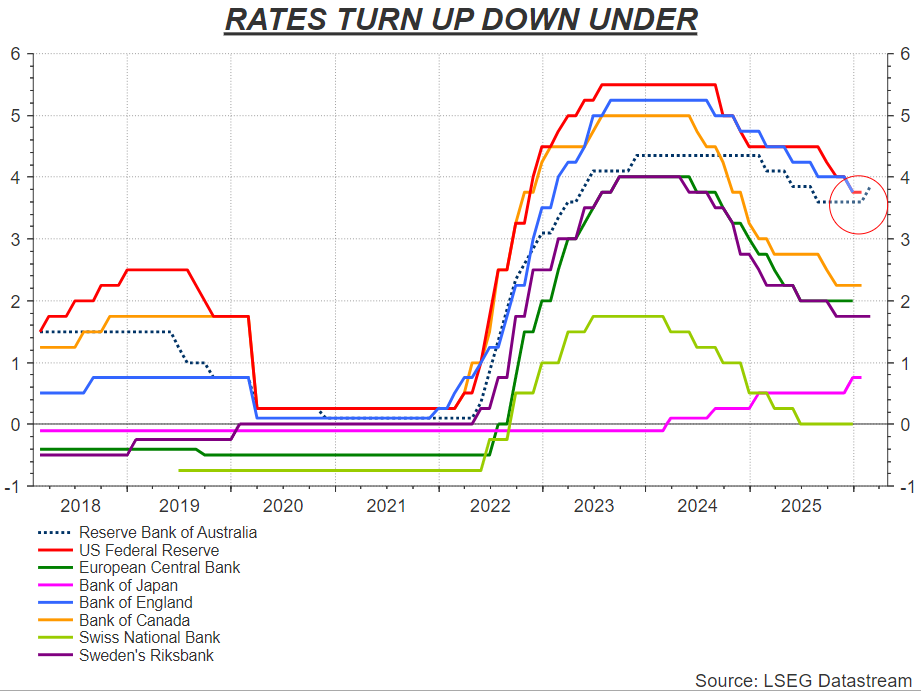

Back in macro markets, investors are trying to parse signs of an acceleration in economic activity flagged by the sharp jump in ISM's manufacturing index, brisk business loan growth in the Fed's quarterly loan officers survey and even the slightly jarring sight of Australia raising interest rates this week.

ISM's service sector report for last month is due later, with ADP's private sector jobs report also due. Even though the House of Representatives voted on Tuesday to end this week's partial government shutdown - at least for another 10 days - it's too late to ensure a full January employment report this week.

Overseas, service sector surveys were slightly below forecast in Europe, but they picked up steam in Japan and China.

With one eye on tomorrow's European Central Bank and Bank of England policy meetings, currencies were a bit calmer. But the yen fell again ahead of weekend elections in Japan, and China's yuan briefly strengthened to its best levels in almost three years as the Lunar New Year holiday nears.

Gold continued its recovery and oil spiked amid a fresh flare-up in U.S.-Iran tensions that saw the U.S. military down an Iranian drone on Tuesday. Bitcoin struggled to stabilize after hitting its lowest level since before the U.S. election in 2024.