Having zoomed up on the escalator, the worry is now that gold and silver markets are hurtling down in the lift as investors unwind their trades. Silver is currently down another 5.5% and after Friday's 30% plunge is headed for its biggest two-day loss since at least the 1980s. Gold has dropped another 3.4% too after its 9% Friday meltdown marked its biggest single-day decline since 2013.

Dealers say pressure on a number of silver futures funds in China added to the rout late last week and the mood hasn't been helped today by news that CME had raised margin calls on some of its key gold and silver futures contracts.

Adding to the commodity crunch, oil prices are also down nearly 5% after Trump said over the weekend that Iran was "seriously talking" with Washington, perhaps lessening the risk of a U.S. military strike on the country, at least in the coming days.

It has all started to knock the equity markets. Wall Street's Nasdaq futures are off nearly 1% while the so-called VIX "fear gauge" is rising toward the 20 level again.

About one quarter of the S&P 500 is set to report this week, and growth in earnings per share was running at 11% on the previous year, when consensus had been for 7%. Scrutiny will be razor sharp on tech majors Alphabet, Amazon and AMD, particularly on their costs and how they see the benefits of AI in the wake of Microsoft's poorly received results last week.

European stocks are showing some signs of stabilisation - around 30% of the STOXX 600's constituents report earnings this week. But Asia saw the "bubbly" South Korean stock market tumble 5.5% as its big name chipmakers got whacked by the persistent AI jitters and Hong Kong's Hang Seng also fell over 2% after data over the weekend revealed China's official PMI fell back below 50 again. Japan's Nikkei also dropped more than 1% despite a brief push into the green on an opinion poll suggesting Prime Minister Sanae Takaichi's Liberal Democratic Party was likely to score a landslide victory in next week's lower house election.

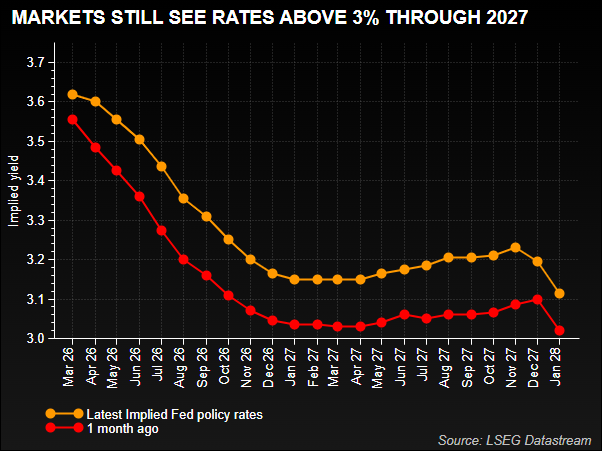

The coming week also has a deluge of U.S. macro data. Monday kicks things off with the January ISM manufacturing index although the main event will be Friday's non-farm payrolls report, with consumer sentiment figures and the latest Treasury’s quarterly refunding details keeping the interest up in between.

Also on the menu are policy meetings by the Reserve Bank of Australia, European Central Bank and Bank of England.

The RBA is an outlier in that markets imply around a 75% chance it will raise interest rates by a quarter point to 3.85%, so reversing one of three cuts delivered last year, in an attempt to quell resurgent inflation.