|

|

|

|

|

|

|

|

|

Kathryn Chisholm was eyeing an early retirement after 20 years at Stemcell Technologies, until AI advances made much of her work redundant. Isabella Falsetti/The Globe and Mail

|

|

|

|

|

Good morning. We’re digging into how late-career layoffs can throw a big ol’ wrench into a well-laid retirement plan. Plus, we’ve got some smart credit card tips to help you navigate your finances. Read on! |

|

|

|

|

Late-career layoffs: When retirement plans hit pause |

|

|

|

|

Getting laid off is brutal at any age, but when it happens in your 40s, 50s or 60s, it can feel like someone pulled the rug out from under your retirement. That’s often when you’re earning your peak salary, have the most debt, and are mapping out your next chapter. |

|

|

|

|

Curious how Canadians are navigating this, we asked readers to share their stories — and the floodgates opened. People told us about the financial stress, the mental health toll, and the unexpected reinventions that followed. |

|

|

|

|

Many blamed forces such as tariffs, automation and advances in AI for their layoffs. |

|

|

|

|

Take Kathryn Chisholm, 52, from Vancouver. After 20 years at Stemcell Technologies, she was eyeing an early retirement with her husband. But last year, AI advances made much of her work redundant. Overnight, her nearly $200,000 salary vanished and her retirement clock got pushed back by at least five years. “This change will definitely delay the start of our retirement,” she says. |

|

|

|

|

Then there’s Paul Whiteley, 51, who’s been laid off three times, with the most recent being about 2½ months ago. The first time was devastating, but this time, he’s using it as a chance to explore a new career as a financial planner. |

|

|

|

|

Losing a job late in life can feel like an unwanted detour. But it can also be a pivot point — a moment to rethink priorities, explore new paths, and reshape what retirement might look like. For example, Tonya Archer, 53, is piecing together freelance gigs while she makes a career shift from a program manager to career coaching. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

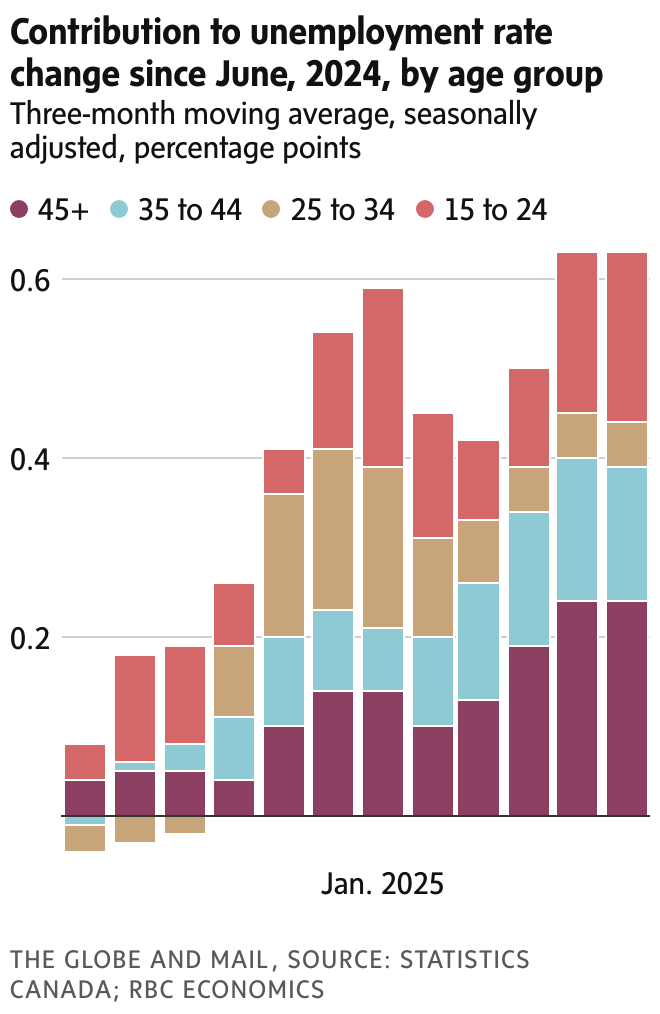

Late-career job losses are on the rise. According to Statistics Canada, workers aged 45 and older made up nearly 40 per cent of the increase in the unemployment rate over the past year as of June. |

|

|

|

|

Plus: Economic ups and downs have nudged some retirees back into the workforce, with more Canadians 55 and up actively looking for work after recently leaving the labour market. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mike and Miriam need advice on how to deal with the unrealized capital gains on their stock portfolio and how to pass the wealth to their only daughter. Jennifer Roberts/The Globe and Mail

|

|

|

|

|

Now with $4-million, what’s the best way for Mike, 68, and Miriam, 66, to handle their capital gains and pass on wealth? |

|

|

|

|

The numbers: The retired couple was in Financial Facelift five years ago with combined savings and investments that totalled $2.5-million. Today, that has grown to $4-million. |

|

|

|

|

The situation: With no pensions, their income comes from government benefits, dividends, interest, and, eventually, mandatory RRIF withdrawals. They want to spend about $100,000 a year after tax and leave plenty to their 22-year-old daughter. They want to sell some stocks now, gift part of the proceeds for a down payment, and manage withdrawals to avoid large tax bills later. |

|

|

|

|

Key steps, from a financial planner: In the years before they have to start taking mandatory withdrawals from their RRIFs, they can sell off some of their stocks, keeping their taxable income low enough to avoid the highest marginal tax rate, and gift the proceeds of the stock sales to their daughter for a down payment. |

|

|

|

|

|

|

|

|

|

|

|

|