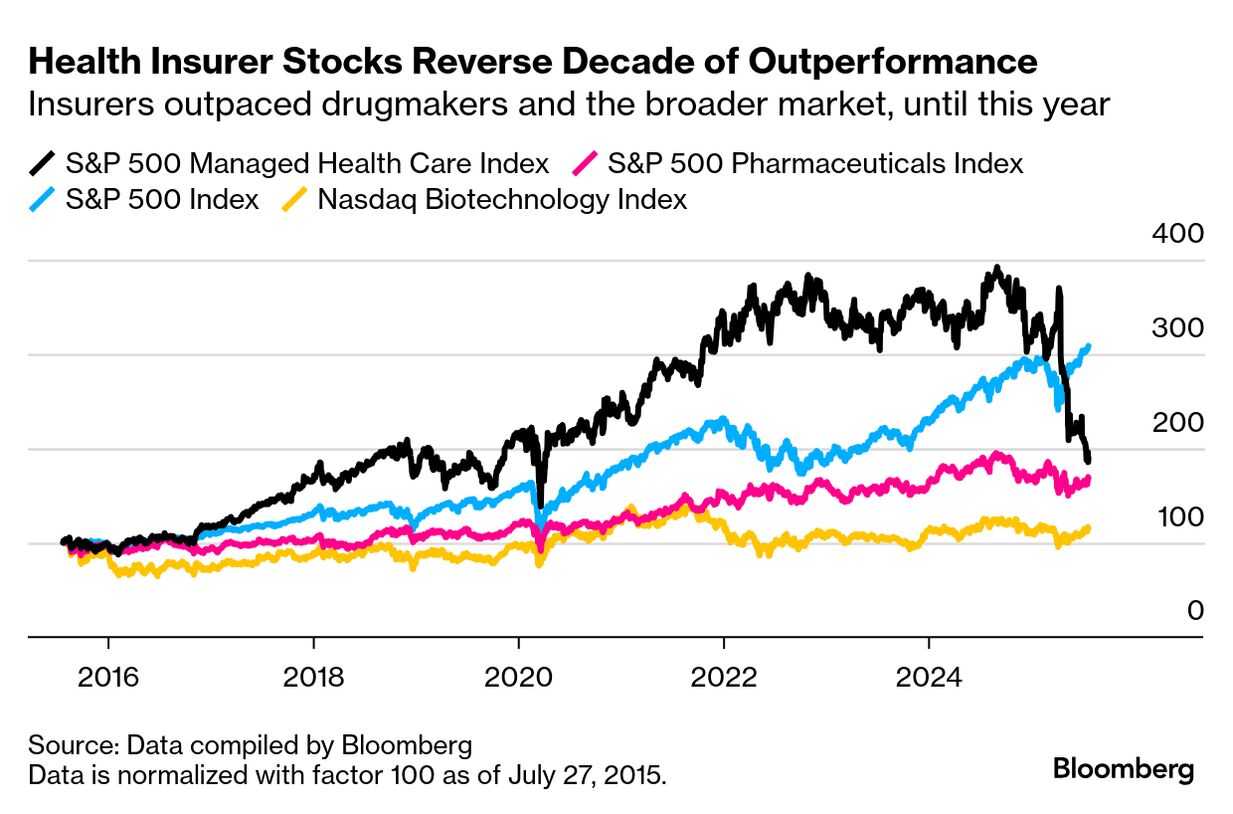

| Every year, number crunchers at US health insurance companies look at their enrolled populations and calculate how many of them will break their arms, require a heart stent or be diagnosed with cancer. They use these figures to determine how much to charge in premiums to be able to cover patients’ medical issues and still make a profit. This year, the number crunchers have been spectacularly wrong — and that means prices are going up next year. On Friday, insurer Centene reported a surprise quarterly loss. That followed disappointing earnings from Elevance Health and Molina Healthcare, also major insurance providers for Medicaid and other government health programs. UnitedHealth, the largest US insurer, withdrew its outlook entirely in May in a move that shocked Wall Street. Centene, Molina and UnitedHealth are some of the worst-performing stocks among large US companies this year. What happened? The companies broadly have cited changes in government programs that squeezed revenue and in some cases kicked members off plans. Some of these changes have been on the horizon for years: - In Medicare, the program for seniors, the government is revamping payment rules that were widely seen as susceptible to being gamed, cutting reimbursements for some insurers.

- In Medicaid, for low-income Americans, millions of people were removed from insurance rolls after states resumed checking eligibility.

- In the Affordable Care Act markets, also called Obamacare, efforts to crack down on improper or fraudulent enrollments are also reducing membership and exposing insurers to unanticipated risks.

On top of the policy changes, health insurance companies say medical expenses are being driven up by expensive drugs, more demand for mental health and substance abuse treatment, and aggressive billing by hospitals and other providers. Medical costs in the broader commercial market are set to rise by 8.5% next year, according to a survey of actuaries by PwC. To cover costs going forward, insurers raise prices. In the ACA markets, they’re requesting the steepest rate hikes in five years, researchers from KFF recently reported, with a typical increase of 15%. Many people who get government subsidies to buy ACA coverage won’t have to absorb that hit directly, though increased prices would still drive up government spending, which is funded with tax dollars. But there are challenges for insurers — and their members — on that front, too: Enhanced subsidies passed during the Biden administration that brought down people’s costs are set to expire after this year. The extra subsidies and lax oversight may have paved the way for widespread fraud and duplicative enrollments, which benefited insurers. The Biden administration took steps to rein that in, and Trump officials are heightening their focus on “program integrity” enforcement that will lower enrollment, potentially leaving insurers with a smaller and sicker — and therefore costlier — pool of people on their rolls. The years ahead will be tricky for insurers to navigate. Congress recently passed cuts of $1 trillion in Medicaid spending over the next 10 years, despite President Donald Trump promising he would not cut the benefits when he was campaigning for president. The Congressional Budget Office says the law will increase the number of people without health insurance by 10 million by 2034, largely driven by new work requirements for people on Medicaid. With future insurance in doubt, patients may be seeking more medical care now while they still have coverage. That’s set to boost medical spending this year, Centene said. It’s another element of uncertainty in a business that hinges on making accurate predictions — and can unravel when they’re wrong. — John Tozzi |