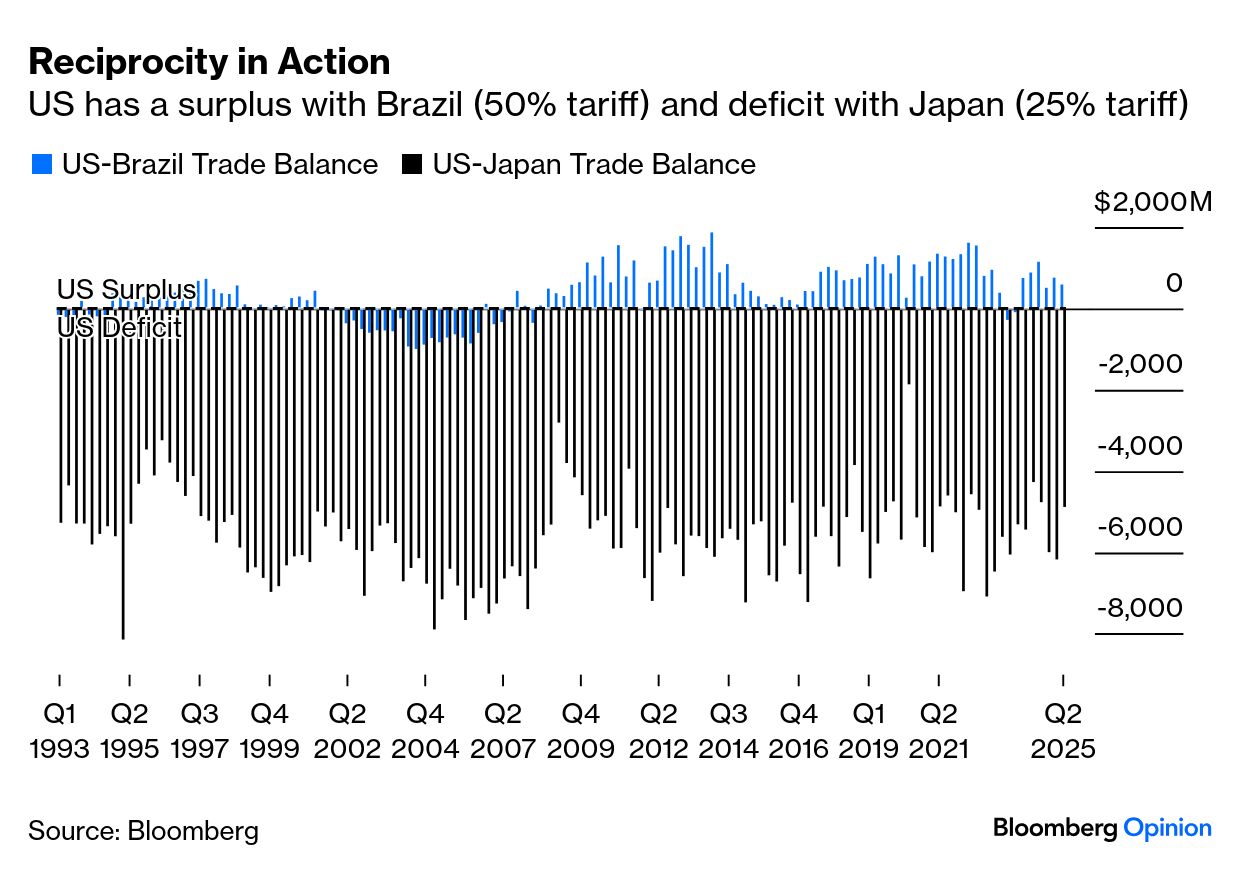

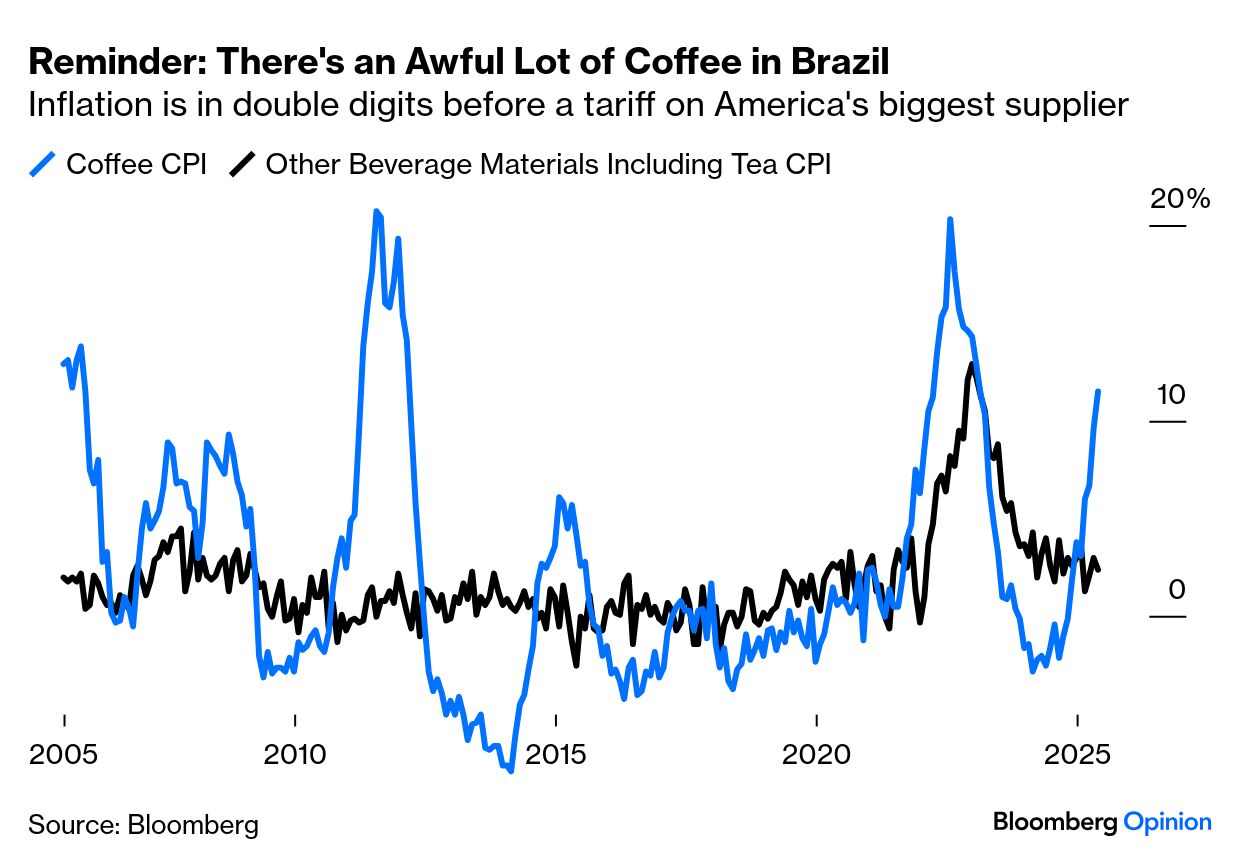

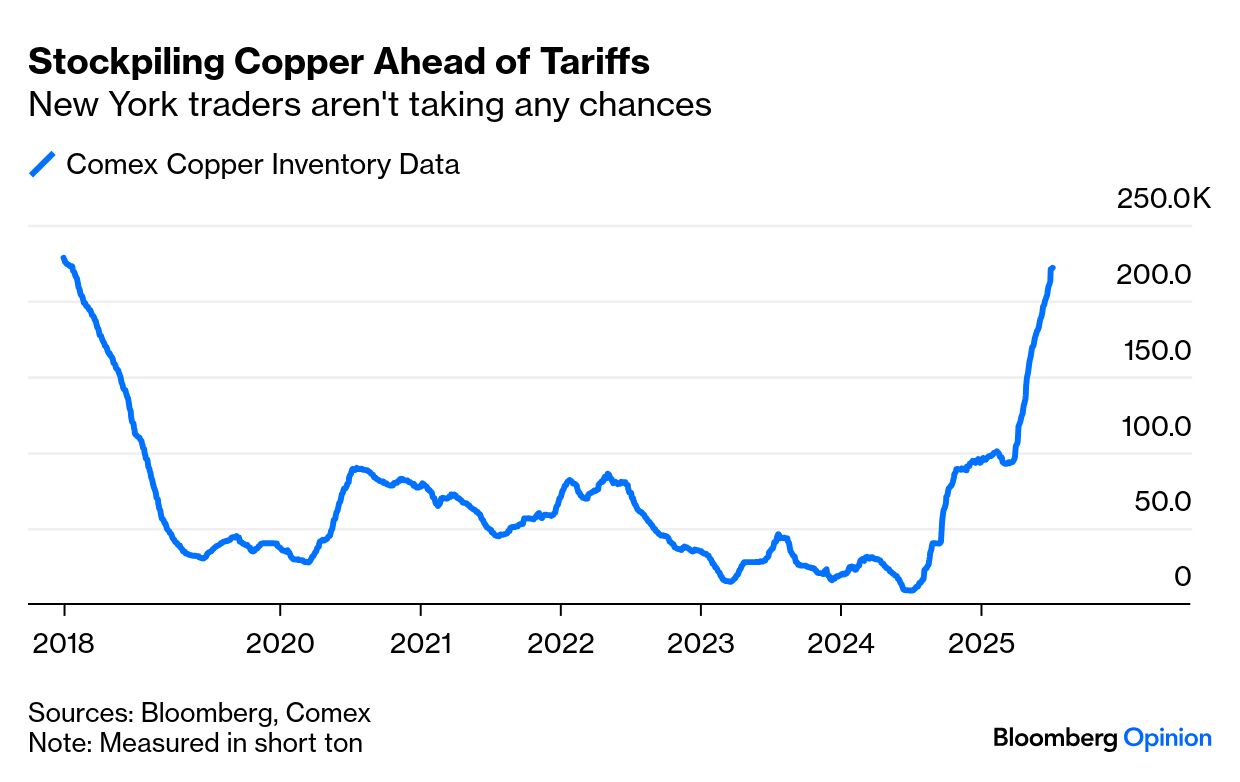

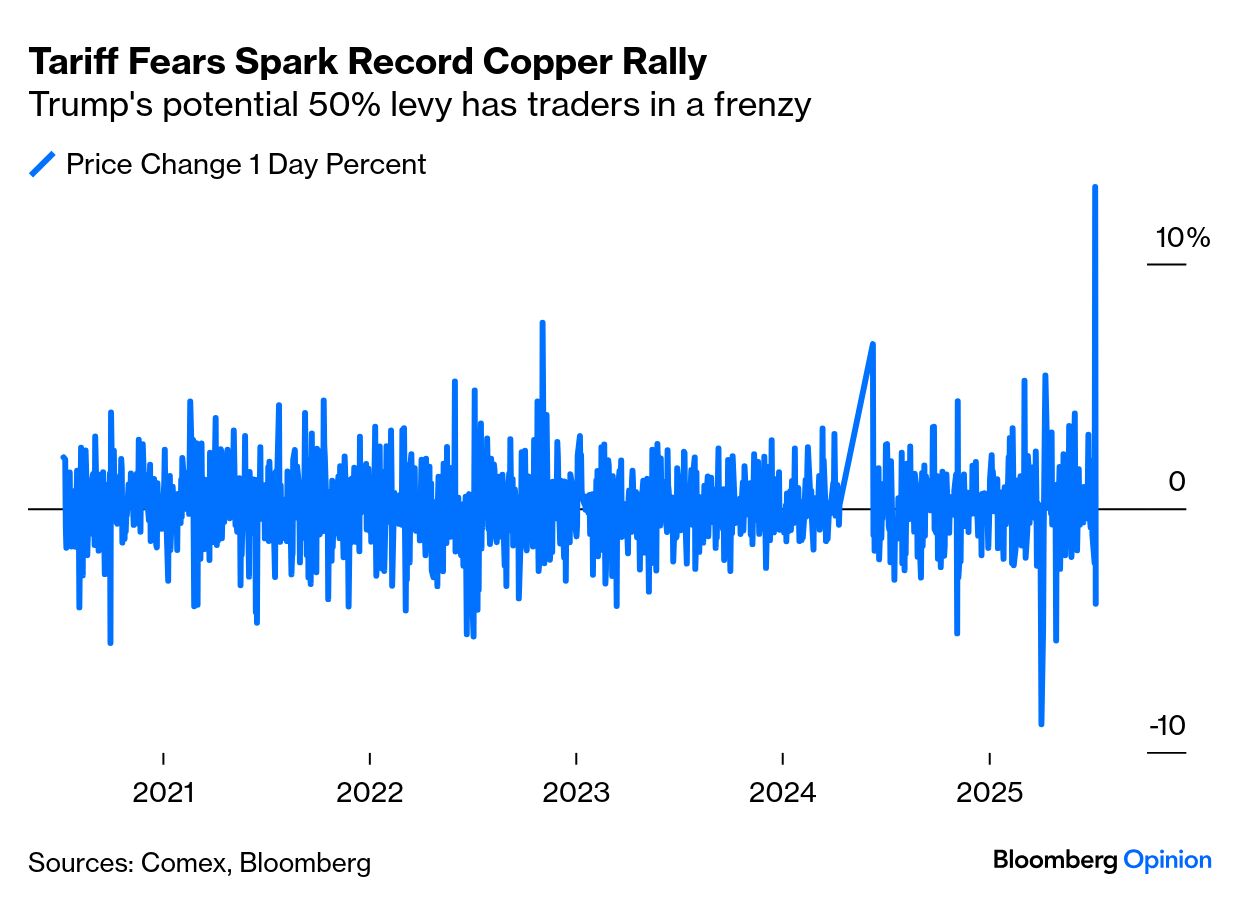

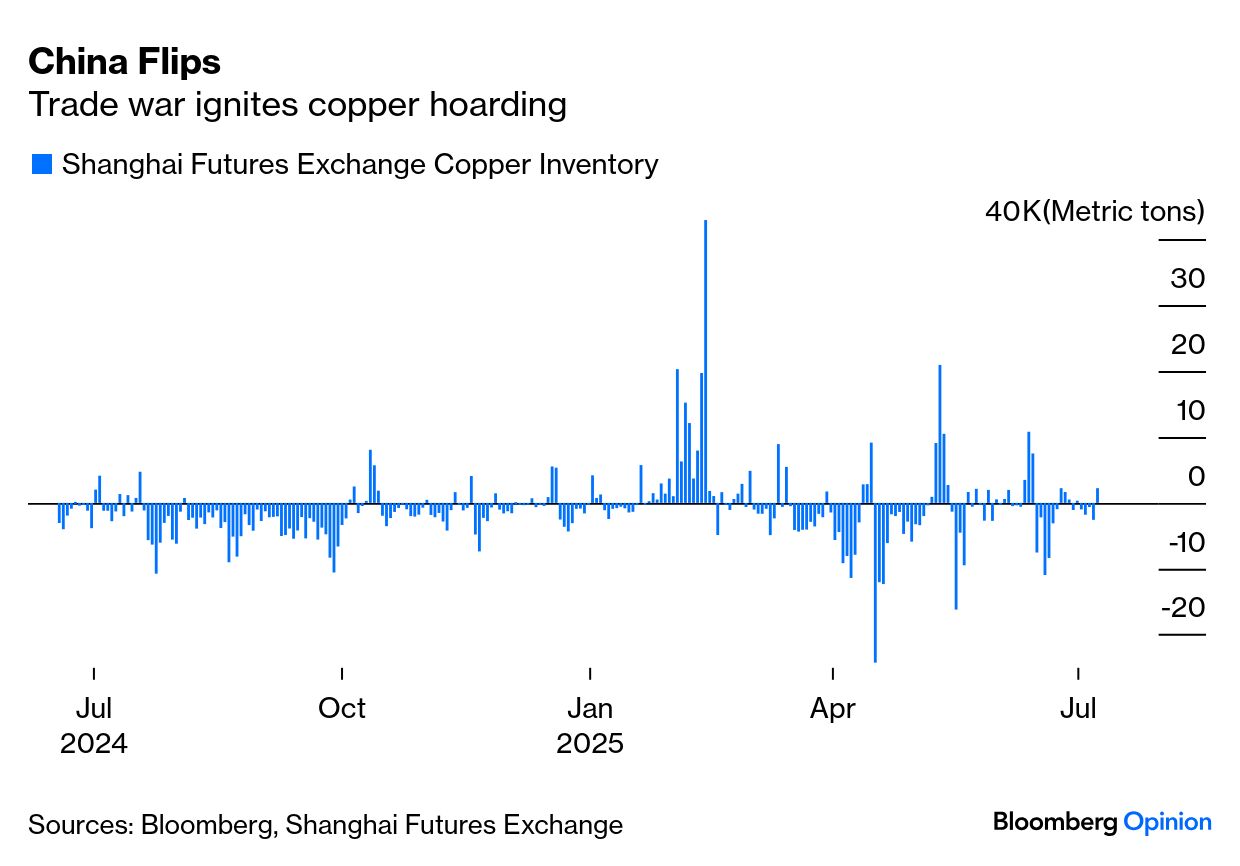

| The global copper industry saw President Donald Trump’s proposed 50% tariffs from a mile away. As early as February, he mooted the idea on national security grounds. That day of reckoning is fast approaching, barring a TACO U-turn, and the way the copper market is dealing with the issue — including a bizarre race to make deliveries to Hawaii and Puerto Rico to beat levies — has pointers for Brazil, hit with only a 10% overall levy three months ago, but now singled out for 50%: Brazil In this letter, Trump explains his reasons: This is about politics. Trump intends the levy to punish what he sees as bad political behavior. Importers won’t be happy. But the most important implication is that the Trump political victories of the last few weeks — along with the lack of any serious negative effects from the tariffs to date — have left him freshly empowered. The president might “chicken out,” but it will need a market dive or bad economic data to force him into it. As Brazil will find it hard to concede to Trump’s demands, the threat of a drawn-out conflict is real. The Liberation Day tariffs announced April 2 were driven to the exclusion of all else by trade deficits. The higher a country’s surplus with the US, the higher its tariff. A 90-day pause later, and that has changed. The US enjoys a surplus with Brazil. By Liberation Day logic, it’s Brazil that should be imposing a levy. Just compare the US trade balances of Brazil and Japan (25% tariff): Levies now have nothing to do with the economy. They’re an exercise of power, made despite the risk of pain for the US. Putting tariffs on “any and all Brazilian products” would be inflationary. Brazil is the US’ largest coffee supplier, accounting for 35% of Arabica supply. This is a commodity many Americans simply cannot do without. Coffee inflation is already in double figures: The US could substitute from other suppliers, but that will take time. People want their coffee fix now, and American tastes are more discriminating than they used to be. Brazil also accounts for 55% of US iron ore imports. That’s not great for manufacturers, whom the tariffs are supposed to protect. That brings us to copper. Copper The 50% tariff came via a presidential off-the-cuff comment (formally confirmed Wednesday), but Comex inventory data make clear that traders were prepared for it. Stockpiles were at levels not seen since 2018: Regardless, copper rallied by more than 10% Tuesday. The subsequent slight retreat could be down to a belief that the tariff will be reversed or slashed. It’s also possible that traders believe there's enough stockpile to meet immediate demands. Whatever the reason, the reaction shows sudden presidential interventions won’t be ignored: The panic is equally unsettling in China, the world’s biggest copper consumer. Historically low inventories spiked earlier this year in response to Trump’s initial musings. This is how warehouse stocks have changed each day, according to the Shanghai Futures Exchange: TD Securities’ Daniel Ghali says the trade war catalyzed US-China competition to secure raw materials. The latest shock will drain global inventory below critical levels needed for market functioning: Incentives are being driven by the threat of US tariffs, and separately, by Chinese stockpiling with strategic hues. Both are constraining metal availability. However, in contrast to prior years, frictions in market rebalancing mechanisms are now also preventing physical metal flows from naturally finding equilibrium.

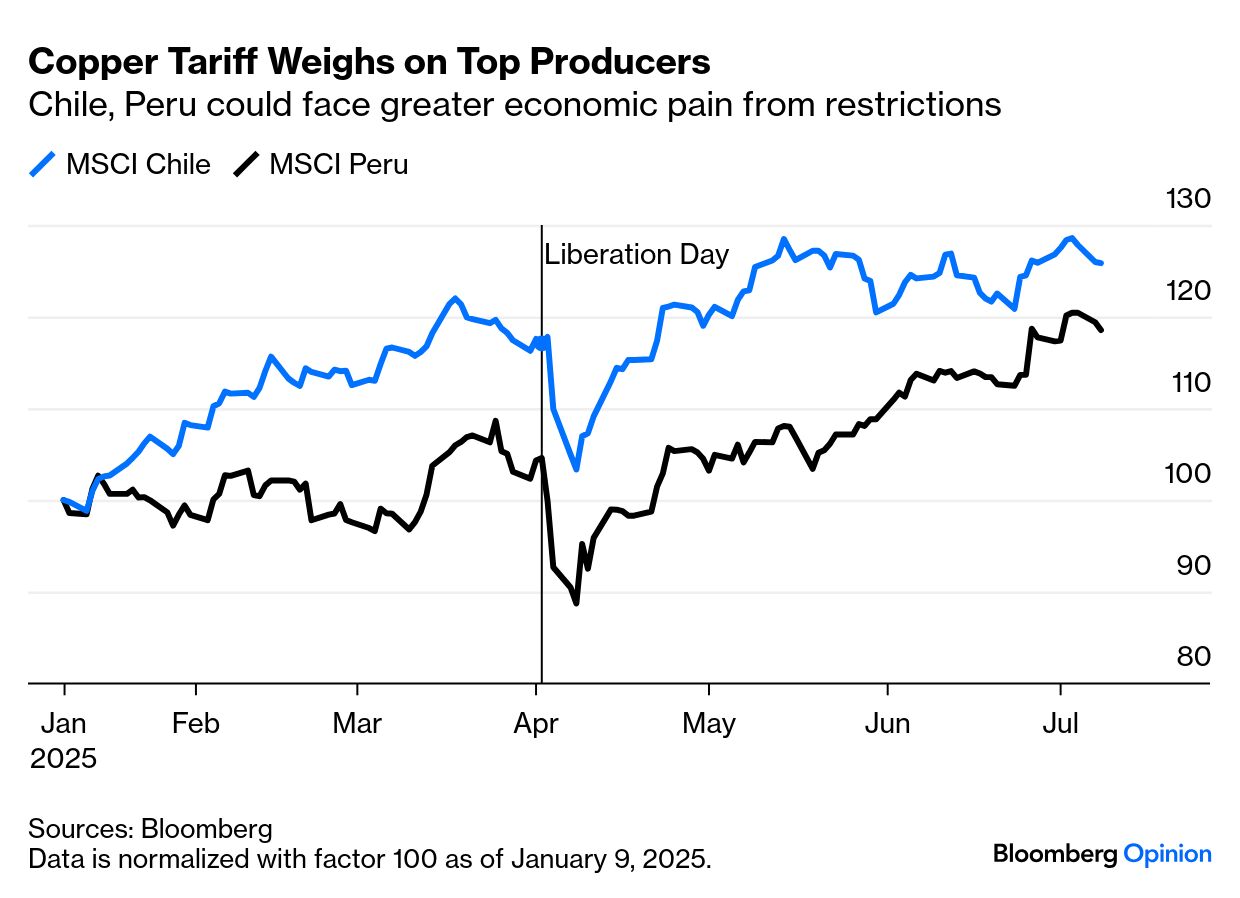

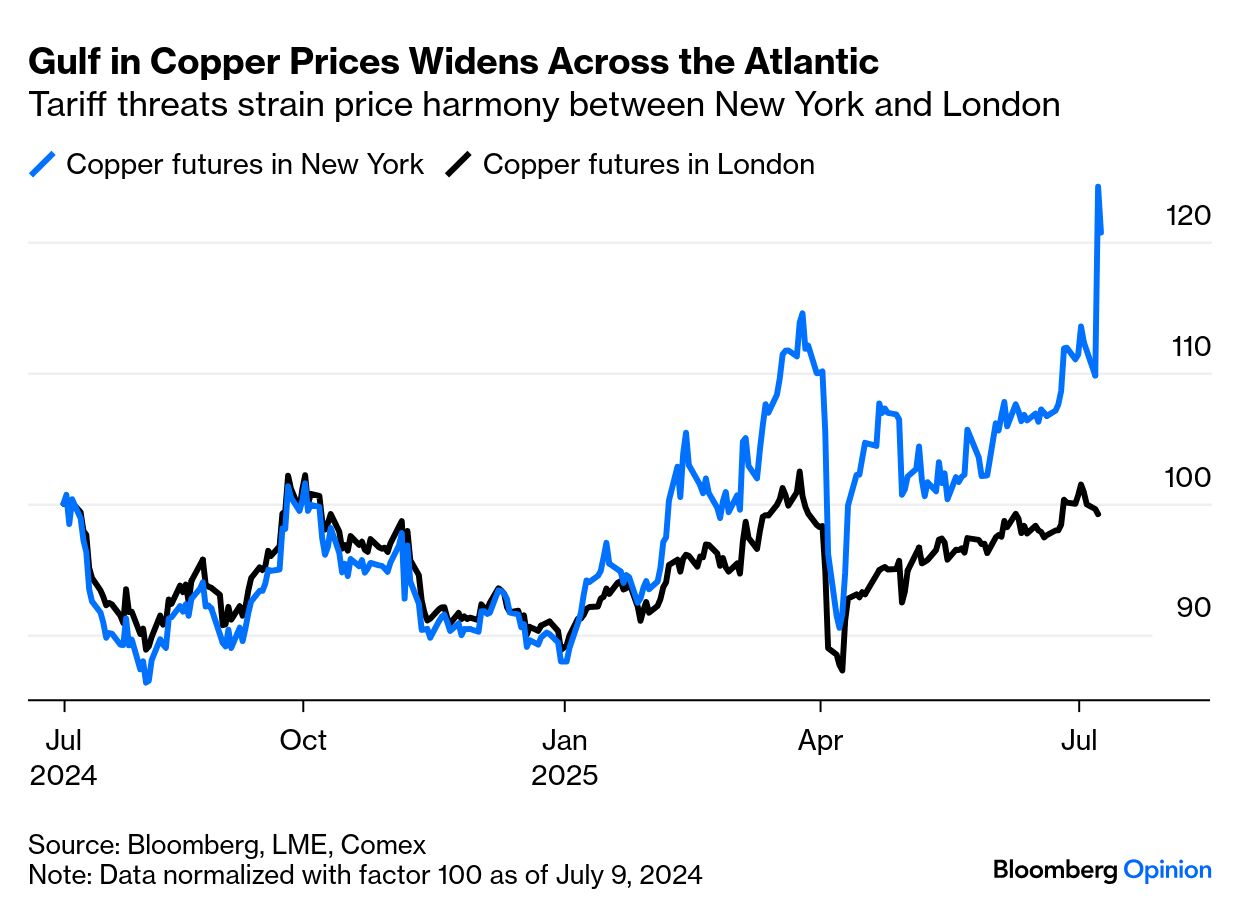

Beyond the scramble to build buffers before the tariff takes effect, there are concerns surrounding how countries like Chile and Peru — two of the world’s largest producers — will be able to cope. So far, the verdict doesn’t look pretty. MSCI indexes show investors’ anxiety. The countries have been spared “reciprocal” tariffs for the time being, but 50% on copper could bite just as much: Bloomberg Economics’ Jimena Zuniga suggests producers can ride the storm, given copper’s inelastic demand. Industrial use of copper is widespread and it’s difficult to replace with other materials. She argues that the greatest impact could fall on the US. That’s certainly suggested by the widening gap between the prices in London and New York: New York’s unprecedented 25% premium over the London price suggests that investors believe tariffs will not be imposed across the board, but on selected top producers. There’s also the question of whether this can possibly help Washington’s ambition to reinstate America’s manufacturing might. As Jefferies LLC’s Christopher LaFemina notes, the US doesn’t have nearly enough refinery capacity to be self-sufficient in copper. Thus tariffs would likely sustain the ongoing record price premiums in the US — and put manufacturers there at a competitive disadvantage. A short-term fix, as Bloomberg News reports, requires boosting production from copper scrap, which has traditionally been shipped to processors overseas. The surge in Comex prices invariably fed into scrap. That might now turn out to be a lifeline, even if temporary, while policymakers await the broader impact from tariffs. —Richard Abbey |