| Where is the tariff inflation? A growing number of macho-pessimists are convinced, much like Arnold Schwarzenegger’s “Terminator,” that rising prices will soon be back. The US has been slapping tariffs on a range of imports for a few months, and that’s already shown up in a sharp increase in the money being paid in import duty: That is real money for Uncle Sam, and it has been paid by someone. But who, ultimately, will bear the price? President Donald Trump’s weekend outburst against Walmart Inc. suggests that the issue is already politicized: Between Walmart and China they should, as is said, “EAT THE TARIFFS,” and not charge valued customers ANYTHING. I’ll be watching, and so will your customers!!!

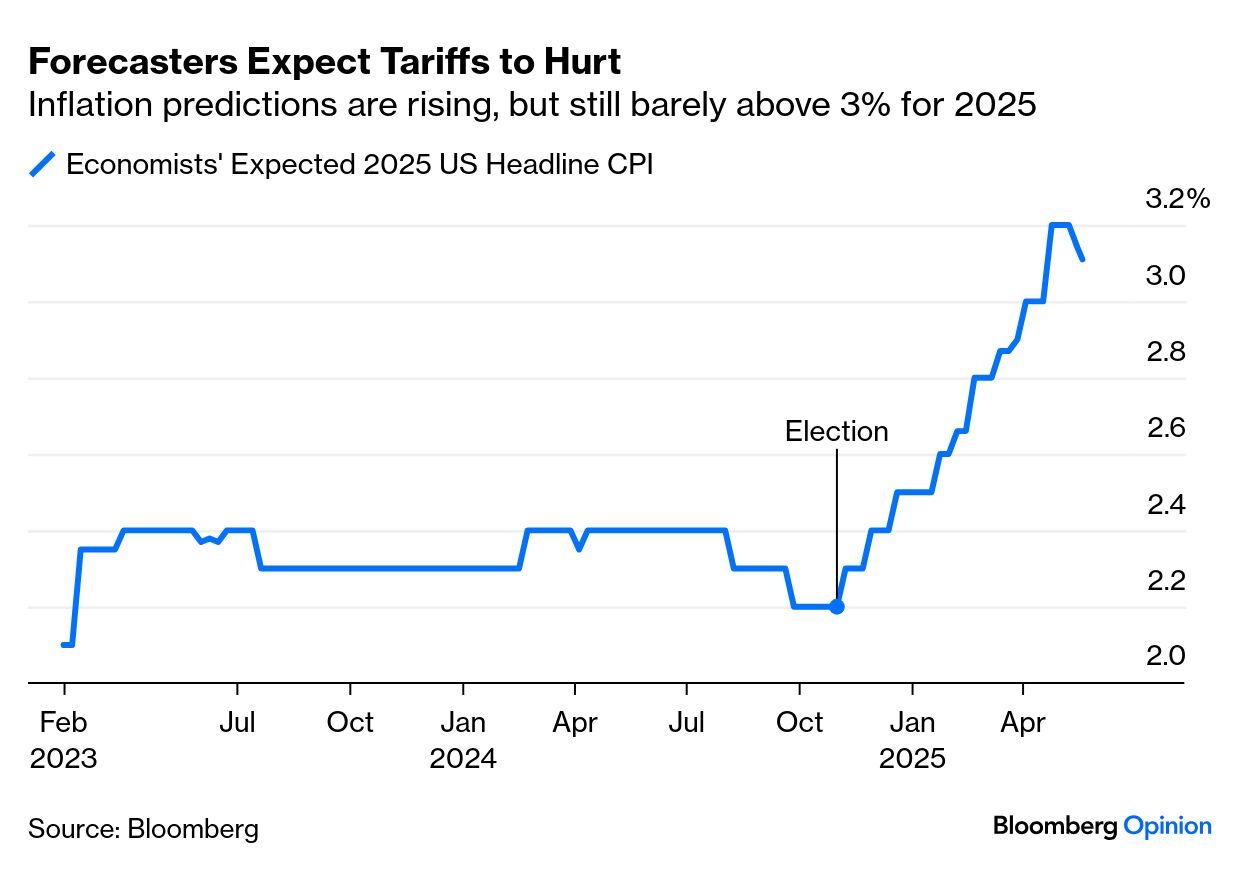

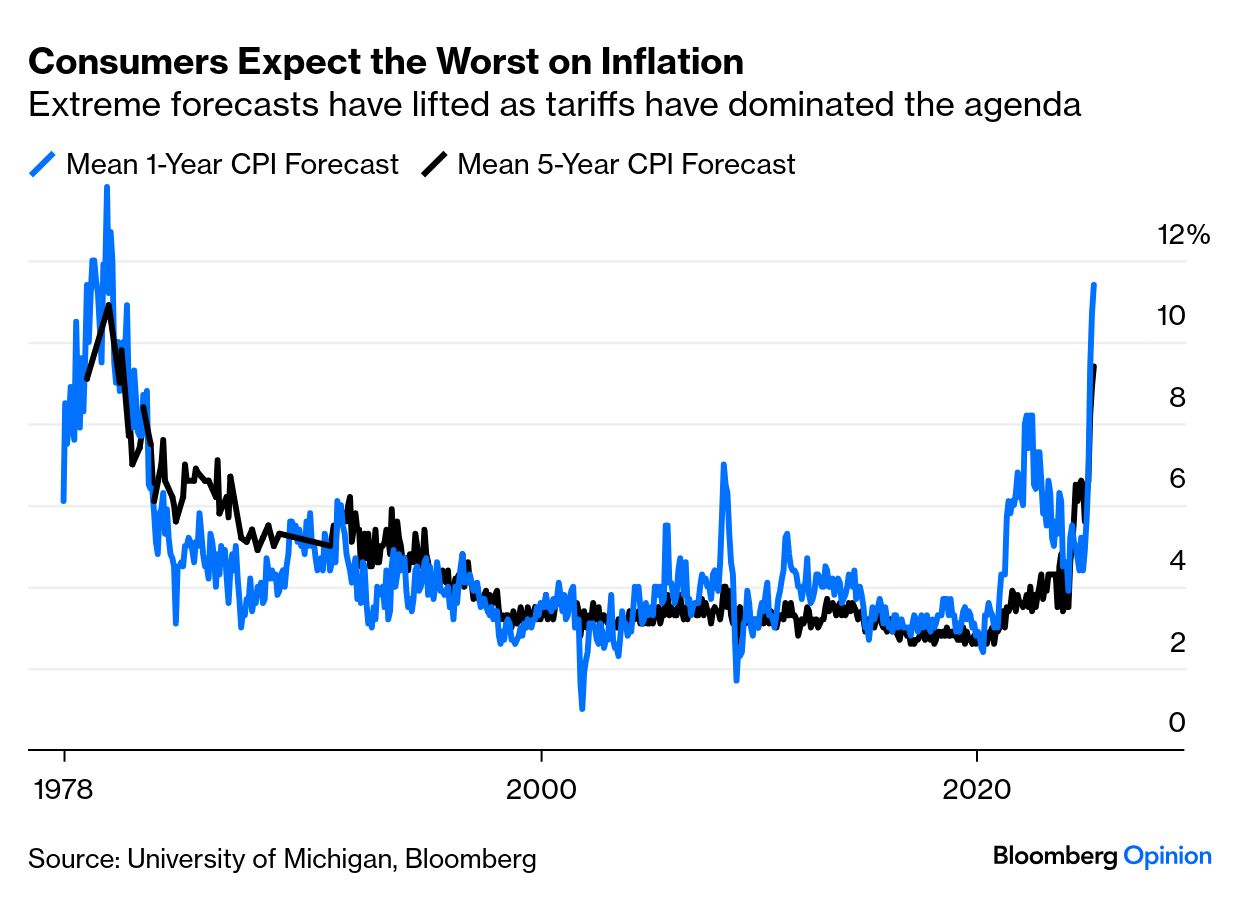

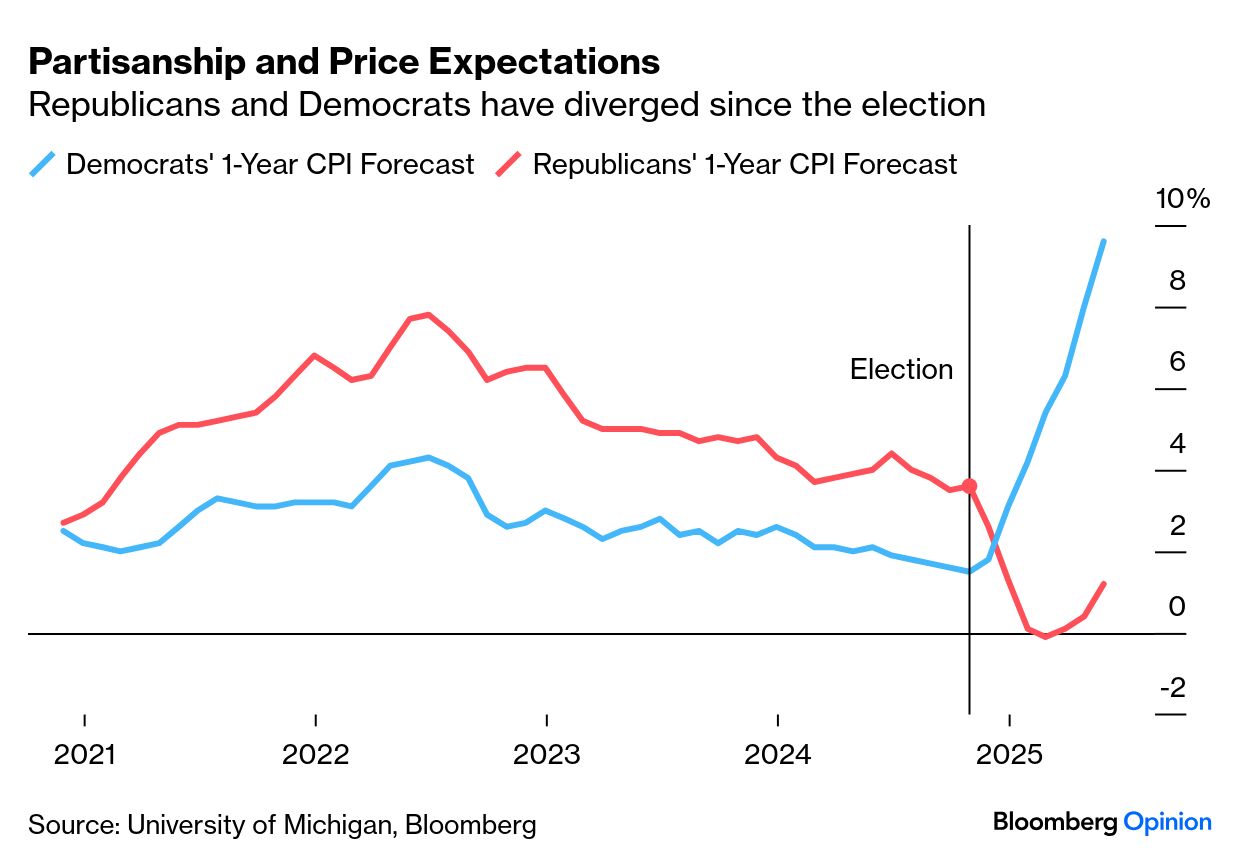

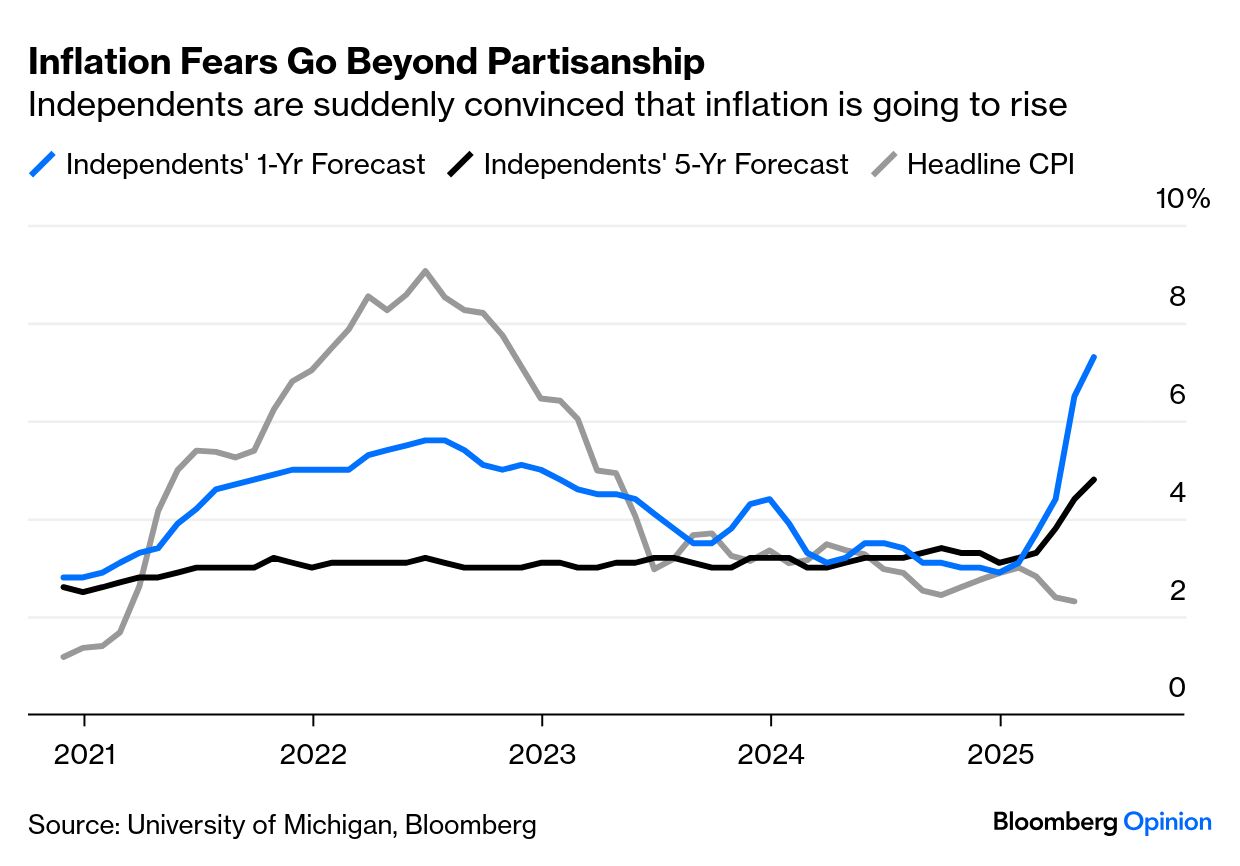

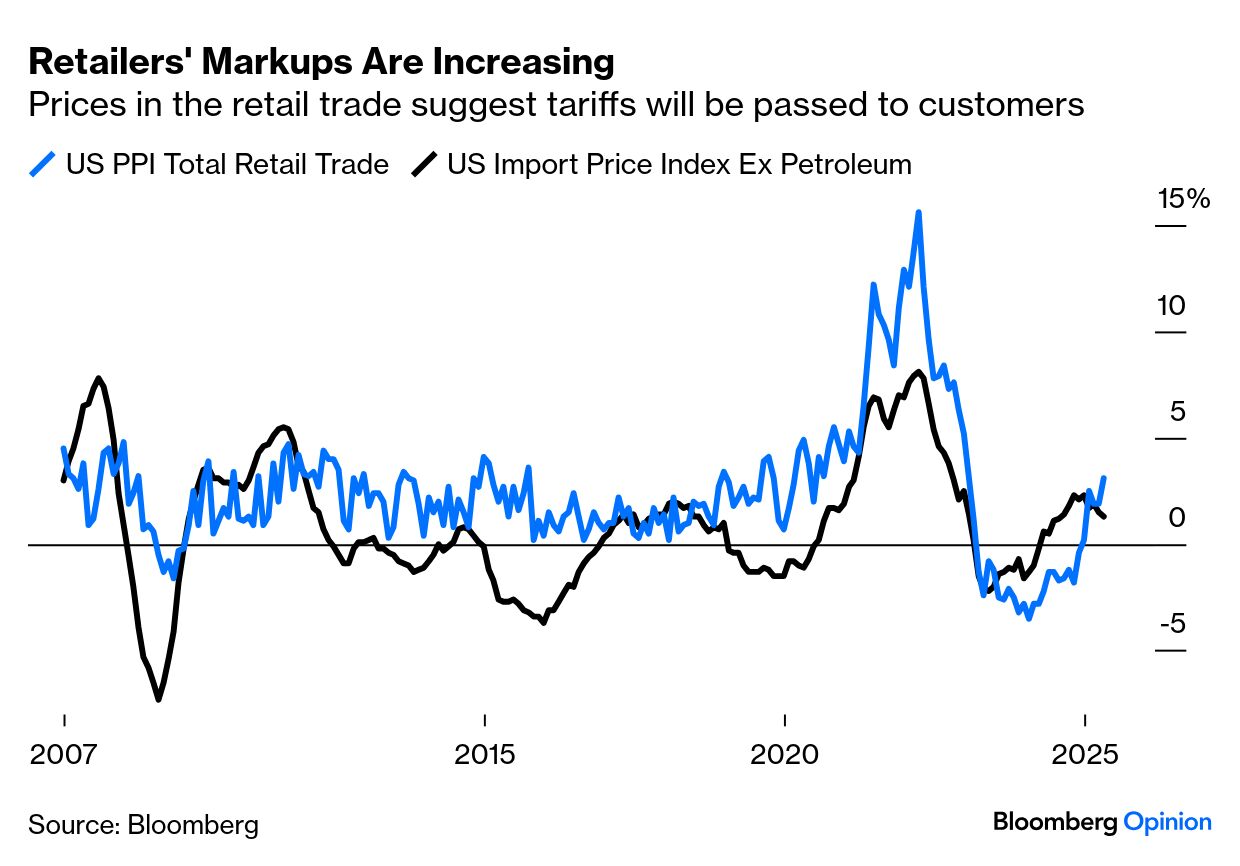

Those with long memories might recall Kamala Harris calling to ban price-gouging during the presidential campaign — retailers have enemies across the political spectrum. Walmart knows that, and also understands that its most crucial constituency is its customers (as Andrea Felsted points out). As a whole, companies have been using earnings conferences to prepare shareholders for tariffs to have a negative impact on profits, so they aren’t expecting to pass them all on to customers. But there are limits to how much shareholders can eat. Economists seem convinced that customers won’t escape without paying “ANYTHING.” Bloomberg’s survey of professional forecasters shows CPI estimates ticking up ever since the election. They’re only a little above 3%, so this isn’t extreme, but the shift is clear: More alarming, for all concerned, is a form of inflationary machismo that has taken hold of the population. Average projected inflation rates reported to the University of Michigan’s long-running survey are flabbergasting, reflecting a degree of fatalisticrelentlessness that would make a Terminator blush (if it could). The average consumer expects inflation of more than 11% over the next 12 months: This looks like madness. Some of it is due to polarization as Americans’ political identity increasingly dominates their opinion on all issues. Michigan has been logging inflation expectations by partisan identity since 2020, and the swing in the last few months has been spectacular. Trump Derangement Syndrome affects both ends of the spectrum, with Democrats expecting double-digit inflation, while Republicans think price rises could be abolished: The depth of division is disquieting. But Michigan also polls independents, who suggest something more worrying for the administration. Their forecasts have shot up since the election, even as actual inflation has fallen. Reasonable people, then, expect tariffs to cause inflation: With tariff revenue already shooting upward, how then is inflation still falling? It does take a while for products to move along the supply chain. And there are now signs that retailers are beginning to increase markups to account for duties. Omair Sharif of Inflation Perspectives LLC offers this handy explanation: Since the item sold to the consumer is typically a finished good (i.e. it does not undergo any transformation), the [Bureau of Labor Statistics] considers a retailer as a supplier of services. Thus the output of a retailer is measured by the difference between the sale price of the item and its acquisition cost. So, retail trade services indexes reflect a retailers’ margins.

With this in mind, the rise in retail trade producer prices measured this way is discomfiting — the highest since early 2023, with the bulk of the tariff shock still in the future: What looks more encouraging on this chart is that import price inflation has declined slightly. Unfortunately, this doesn’t mean that tariffs won’t hit consumers, because US import prices exclude tariffs. Dario Perkins of TS Lombard in London says: “If Chinese exporters were absorbing them, US import prices would be falling much more sharply. Stability in these metrics means China ISN’T paying.” Apparently calm figures are a reason to expect the tariffs to show up in inflation soon. Another reason for the delay is that imports were brought forward to the first quarter to front-run tariffs. Benign producer price inflation might suggest that tariffs have had little effect, but again that’s misleading. Perkins explains: Producer prices EXCLUDE IMPORTS… Once tariffs raise the cost of producing domestic goods and services, that’s when they will appear in the PPI. Given that US companies were accumulating inventories in Q1, it is not surprising that these metrics haven’t moved – YET.

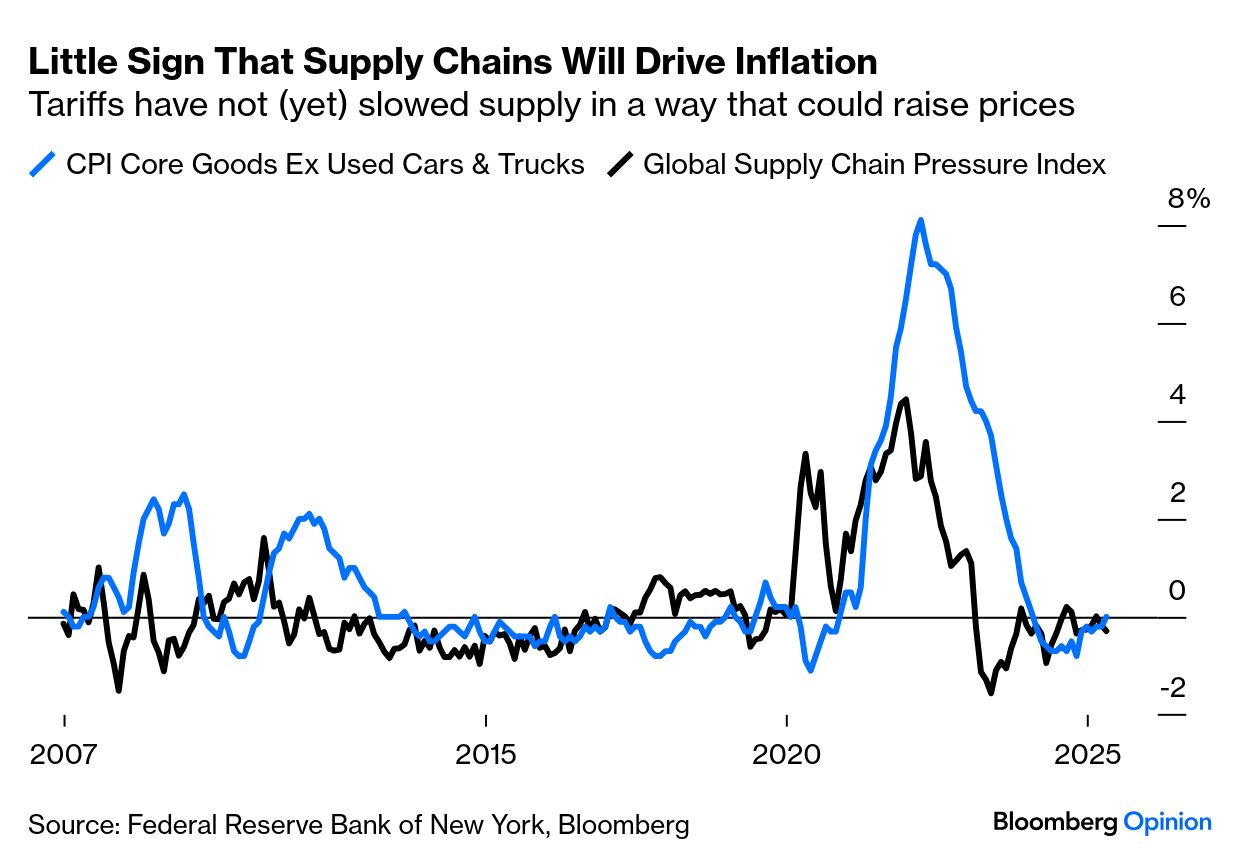

A further potential driver is also yet to appear. Snags in supply chains after the pandemic led to shortages and serious inflation with a lag of a few months. So it’s reassuring that so far, the tariff hostility hasn’t put stress on supply chains: The upshot of all this: Tariff uncertainty will persist even though actual tariff rates should be stable this month and next. It’s politicized, feeds into a febrile consumer environment, and will confront businesses with some excruciating decisions. Get ready. |