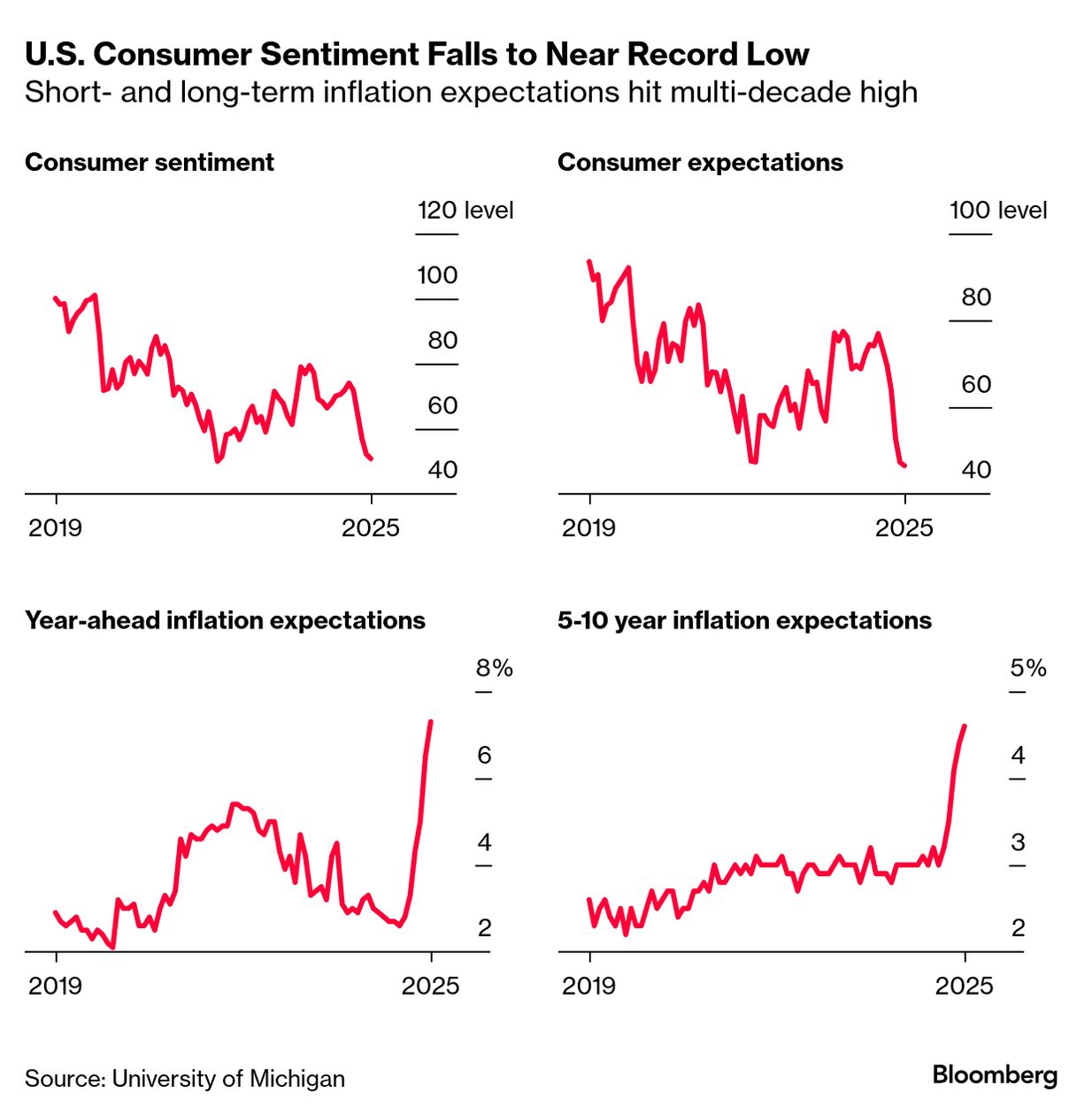

| The US was downgraded by Moody’s Ratings on Friday thanks to government debt that’s approaching a mind-numbing $37 trillion. It was a dramatic move that cast further doubt on the polarized nation’s status as the world’s highest-quality sovereign borrower. Moody’s lowered the US credit score to Aa1 from Aaa, joining Fitch Ratings and S&P Global Ratings in grading the world’s biggest economy below the top, triple-A position. The one-notch cut comes more than a year after Moody’s changed its outlook on the US rating to negative. The federal budget deficit is running near $2 trillion a year, or more than 6% of gross domestic product, and Congressional Republicans are pushing through budget legislation that could add trillions of dollars more. “While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics,” Moody’s wrote in a statement. Earlier today, new data showed US consumer sentiment has fallen to the second-lowest level on record, and inflation expectations climbed to multi-decade highs. The preliminary May sentiment index declined to 50.8 from 52.2 a month earlier, according to the University of Michigan. That was lower than all but one estimate in a Bloomberg survey of economists. The main reason cited was President Donald Trump’s trade war. Nearly three-fourths of respondents to the Michigan survey spontaneously mentioned tariffs. The topic crosses partisan lines, including a notable share of Republicans bringing it up. The new, sobering survey data comes as inflation data from the Trump administration’s Department of Labor has been unexpectedly upbeat, coming in softer than estimates three months in a row. —David E. Rovella |