|

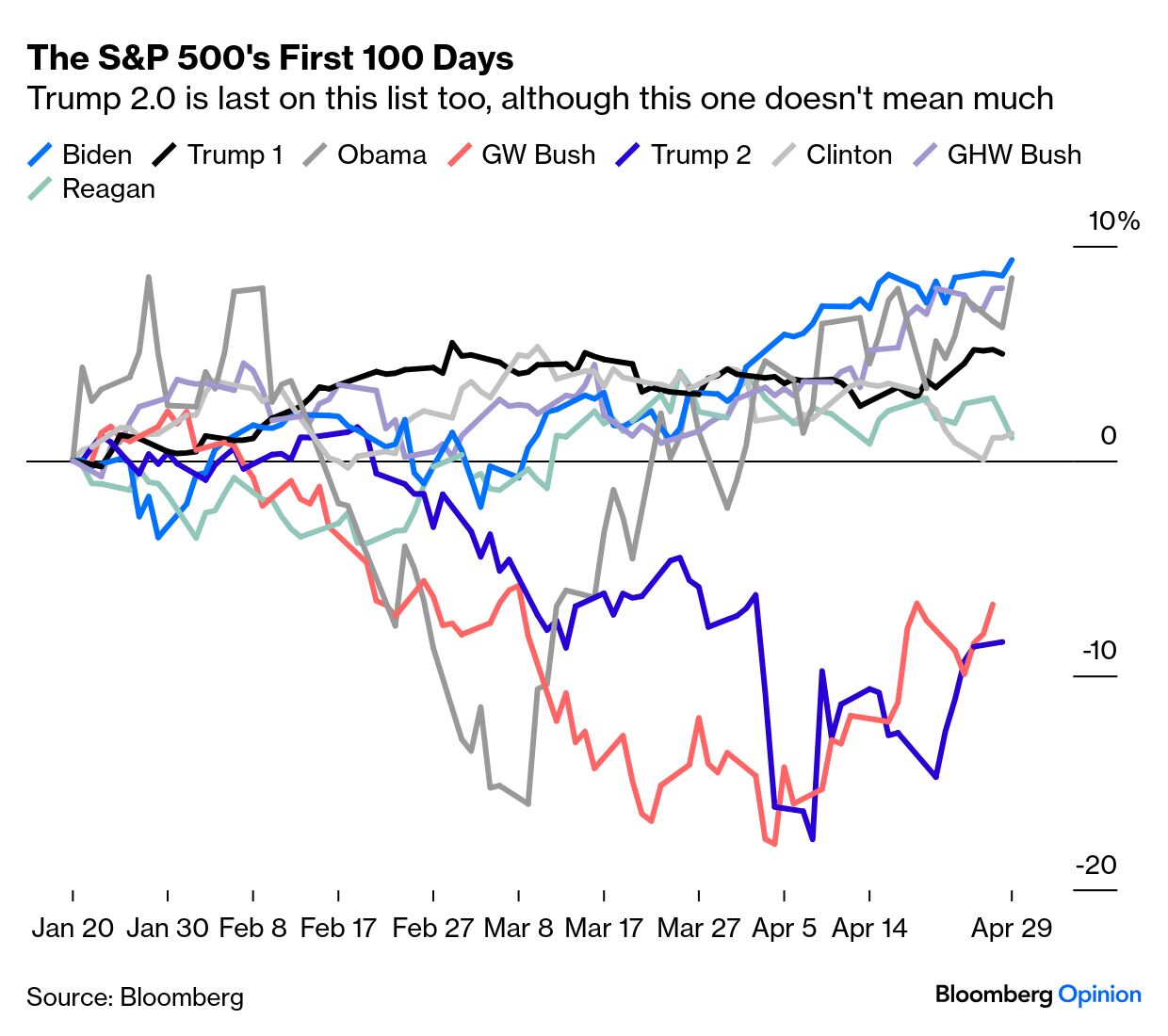

Donald Trump has reached his 100th day in office, the landmark at which all presidents since FDR have been gauged, and the dollar already has a strong verdict. The DXY dollar index, against a basket of other developed market currencies, has given up almost 10%. This is by some way a record in the five decades since Richard Nixon unpegged the dollar from gold in 1971. Trump 2.0 has now become a mirroring outlier for Ronald Reagan’s first 100 days, when the index rose by 10%:

By a curious quirk of fate, Monday was also the centenary of what’s now regarded as possibly history’s greatest currency policy error — Winston Churchill’s decision to return the pound to the gold standard in 1925. That incident laid bare that after a century of dominance, sterling was no longer able to function as the world’s reserve currency. This doesn’t necessarily mean that we should regard Trump 2.0 as a signal that dollar hegemony is over, although it lends itself to that probably overdone narrative. As Capital Economics’ Neil Shearing points out, roughly 90% of cross-border transactions are denominated in dollars – which is far more than would be implied by the US share of global GDP or trade. “In effect, the US provides the financial plumbing for the global economy. This gives it enormous influence.” In another critical difference with Churchill, there is no clear contender waiting in the wings, thanks to the euro’s institutional problems and China’s reluctance to lift capital controls. But it makes ample sense to ask whether this is the beginning of one of the dollar’s long bear cycles — and whether the loss of confidence can be reversed. Taking inflation into account and comparing against a broad range of other currencies, the dollar has a well-established habit of moving in long cycles. The current one started when confidence in the US economy hit rock bottom in the wake of Standard & Poor’s downgrade of US sovereign debt, and it’s now the longest upward trend since the end of the gold peg. A bear market looks overdue: If the Liberation Day tariffs have provided the catalyst to take down the dollar, that would make sense; the uncertainty surrounding US trade policy now makes it far less appealing. It’s also prompted several leading houses to lower their forecasts and even to proclaim the beginning of a dollar bear market. This is from Deutsche Bank AG’s George Saravelos: What has changed since the start of the year? The list of superlatives is

long – the largest shift in US trade policy in a century; the biggest pivot in German fiscal policy since reunification; the most significant

reassessment of US geopolitical leadership since World War II, to name a

few. Our view on all these factors is that the preconditions are now in place for the beginning of a major dollar downtrend.

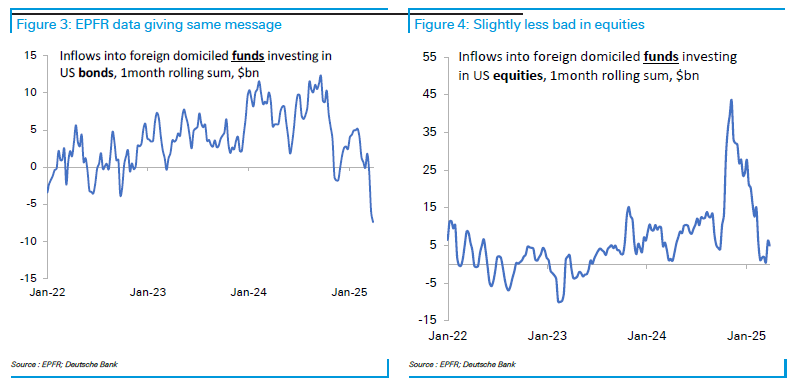

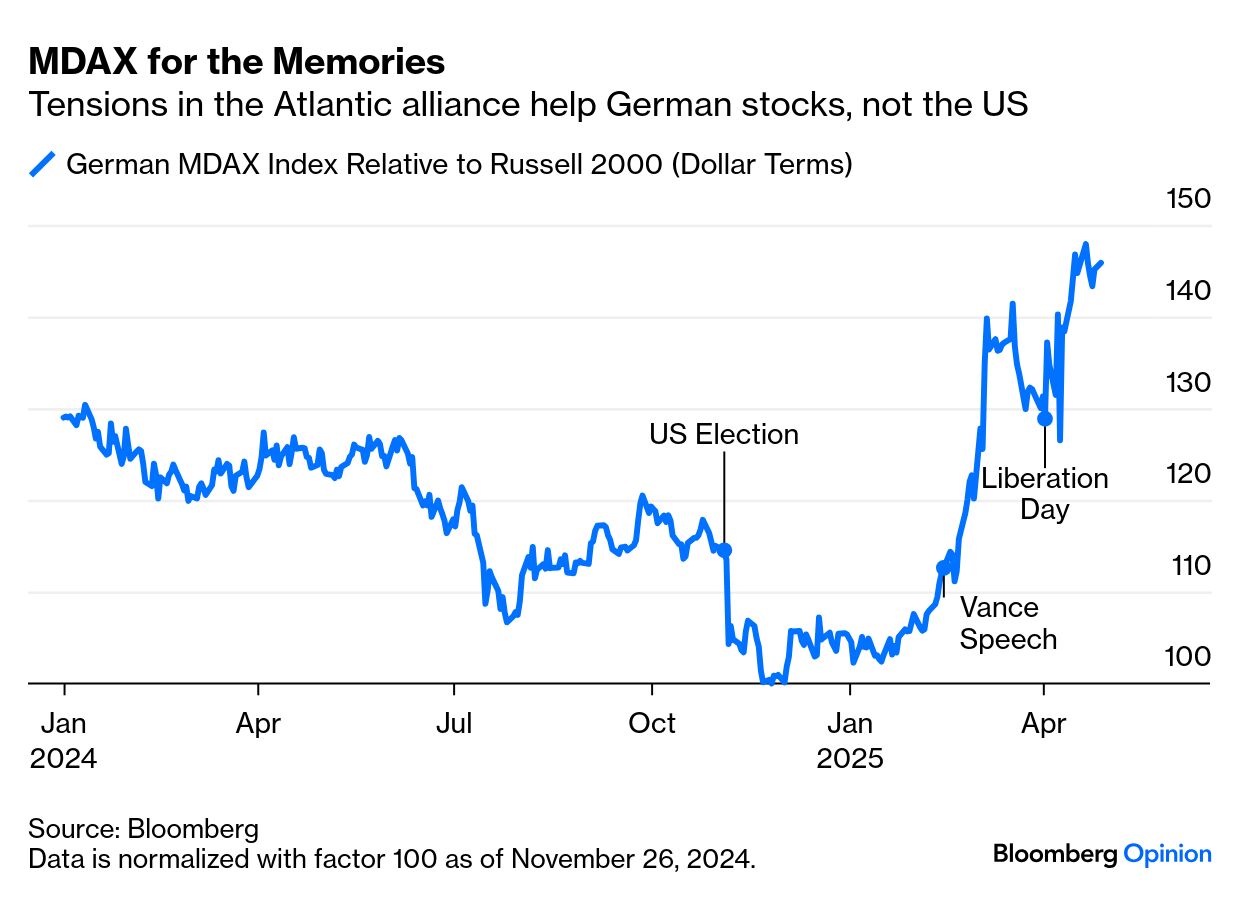

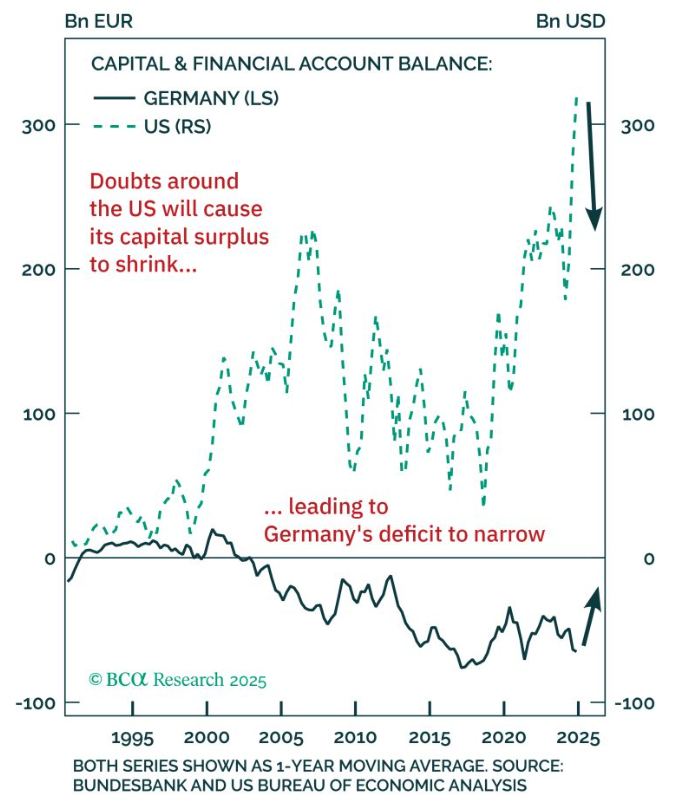

Deutsche expects the dollar to trend ever closer to the $1.30 level at which it has purchasing power parity with the euro over the remainder of this decade. At present, the euro stands at $1.14. While stocks, bonds and commodities have all enjoyed significant rebounds since the post-Liberation Day selloff, the dollar hasn’t joined in. That implies that foreigners have been doing much of the selling, while domestic investors must still be buying: In doing so, however, foreigners are continuing a trend that has been underway for a while. The reserve managers of Japan and China have been reducing their holdings of US Treasuries for years, as this chart from Mansoor Mohi-Uddin, chief economist of the Bank of Singapore, makes clear: Mohi-Uddin adds that US investors could themselves drive future dollar weakness. “If US managers also start raising their foreign assets in response to this year’s shocks,” he says, “the USD will keep trending lower, too.” Of late, the dollar’s problem is centered on individual foreign investors, many of whom are affronted by the Trump administration’s tactics. Saravelos shows below that flows into foreign-denominated exchange-traded funds holding US assets have been sharply negative (although in the case of equities this is largely a function of the extreme enthusiasm that followed Trump’s election): There’s no sign of any recovery among foreigners in the last couple of weeks as the US stock market has rebounded. If the tariff climbdowns have buoyed confidence, it’s been at home, not abroad. EPFR’s data for foreign-domiciled US funds not traded on exchanges shows a broadly similar pattern, although the data do reflect a slight return of demand for equities in recent days: The selling has mostly come from Europeans. Goldman Sachs’ David Kostin offers this chart showing that they’ve staged a dramatic exit from US equities while other foreign investors have generally held on. These figures incorporate both mutual funds and ETFs: That can be explained by the confluence of foreign policy and an overpowering need for economic balance. Vice President JD Vance’s speech in Munich was a watershed moment that convinced Germany (and others) that American support could no longer be relied on, and that it was necessary to rearm. Lifting the constitutional brake on borrowing led to a remarkable surge. That’s clearest from indexes of smaller companies most directly exposed to their home economy, the German MDAX and the US Russell 2000. The former has outperformed the latter by 45% since its brief decline following the US election: For a generation, Germany has been borrowing too little and the US too much. That’s led to a huge accumulation of capital in the US. Rebalancing, as this chart from BCA Research demonstrates, is healthy for all concerned — and there is a lot further to go: Treasury Secretary Scott Bessent has hailed German rebalancing as a positive development. He has a valid point that it might not have happened without the hob-nailed US foreign policy. If there’s a domestic political lesson from the way the dollar is reacting now compared to Reagan’s 100 days, it’s that change in the US happens within parties, not between them. Southern Democrats instituted segregation, and it took a Southern Democrat, Lyndon Johnson, to do away with it. Reagan ushered in a model of assertive free markets, globalization and foreign policy, which added up to a strong dollar. Now, another Republican is championing intervention in the economy, aggressive protectionism and isolationism. Bill Clinton and Barack Obama, both brilliant Democratic politicians, might have had the chance to undo Reaganism, but didn’t. Instead, the job has fallen to a Republican. And it’s obvious what the foreign exchange market thinks of his first 100 days. |