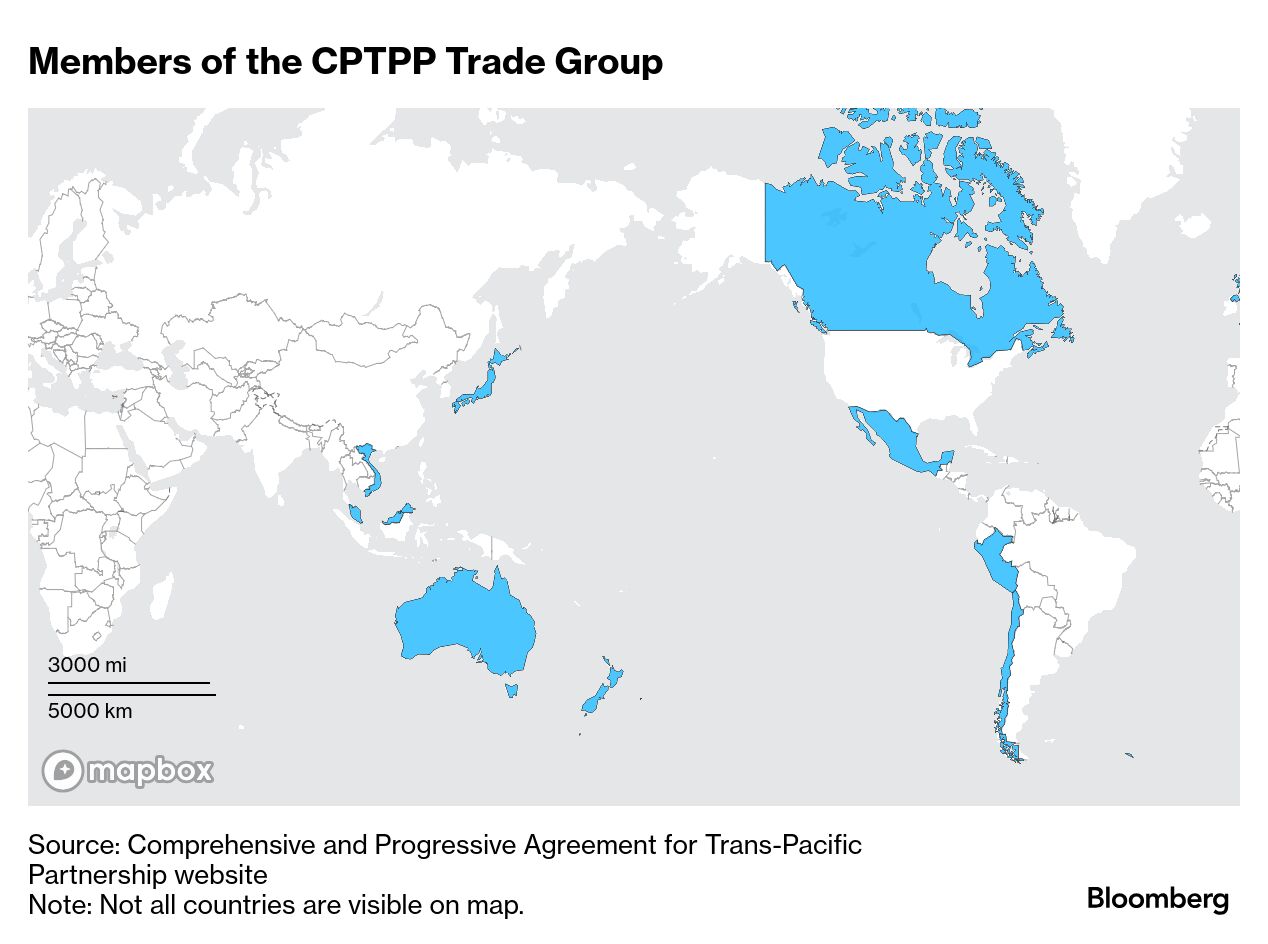

| Timothy Adams, who heads an association of the world’s biggest financial institutions, likens the current shakeup of the global economic system to finding a new operating system on your smartphone. “People are trying to figure out how it works,” he says. One thing the previous OS certainly lacked was leadership from the European Union. Even when not in crisis, the bloc has struggled to make its massive economic weight felt by influencing global behavior. Now that the US, long known as “leader of the free world,” is heading in another direction, the EU is the sole big, rich, open market left. “There’s a lot of excitement about Europe — Europe really has an opportunity,” says Adams. He’s president and chief executive of the Institute for International Finance (IIF) and previously served as the US Treasury’s undersecretary for international affairs. Part of that opportunity is stepping up on defense and building out capacity that would make European leaders’ pronouncements mean more in Moscow. Another angle is economic. If US markets are, under President Donald Trump’s tariffs, no longer the opportunity they once were, Europe’s giant middle class suddenly becomes more important. If the EU’s main members could somehow rise to the occasion, it would be possible to envision the euro as a major global reserve asset and see Brussels as a key driver of international trade rules. Unlikely? Perhaps. But it’s worth remembering (once again) the words of Jean Monnet, one of the founders of the European project: “Europe will be forged in crises.”  Timothy Adams, president of the Institute of International Finance Photographer: Qilai Shen This week in the New Economy | A key point of discussion in financial markets this month has been the central role of the dollar and the $29 trillion US Treasuries market after both tanked alongside American equities. Those moves ran counter to the typical haven bids the dollar and Treasuries get when stocks are plunging on Wall Street. “Absolutely” there’s been a narrative of diversifying away from US assets, Adams said in a Bloomberg Television interview Friday. There are a whole lot of challenges to displacing the dollar’s supremacy in the global financial system, of course. When the euro was created more than a quarter century ago, the question arose as to whether it might rival the greenback. Then-Federal Reserve Chair Alan Greenspan was pressed on the prospect by members of Congress, and even delivered a speech on the euro in which he anticipated a time when foreigners would limit their appetite for dollars. But it's still no rival today. Trouble is, the euro nations failed to craft a single capital market. There’s no benchmark pan-European 10-year note in the way there’s a benchmark 10-year Treasury (every quarter, the US sells some $120 billion of those). There’s a German bund, a 10-year Italian BTP, a 10-year French OAT, and so on, each with distinct sovereign ratings. That fragmentation limits liquidity and thus how easy it is to trade them. Not ideal for a global reserve currency.  Photographer: Alessia Pierdomenico/Bloomberg If Europe increases its integration efforts, the euro could become an alternative to the dollar as a reserve currency, European Central Bank Vice President Luis de Guindos said this week. German Finance Minister Joerg Kukies earlier this month also saw an opening for greater use of the euro when it comes to trade invoicing. “Europe needs its own payments systems, and the euro needs closer financial integration to achieve deeper, more liquid capital markets,” Rogier Quaedvlieg, a senior economist at the Dutch bank ABN Amro, wrote in a note Thursday. “These are both clearly articulated policy objectives, although progress is slow. The US government’s actions are accelerating these developments.” And then there’s the trade front. For decades now, the EU has struggled to forge agreements with other economies around the world. Talks with Mercosur, the South American group including Brazil and Argentina, began in 1999 and a final deal is still pending. But in recent weeks, the European Commission, which handles trade matters for the EU, has been urging capitals to get on board with the bloc’s trade agenda and speed up the approval process for accords, Bloomberg reported this month. An out-of-the-box idea, says Jacob Gunter, lead analyst at the Berlin-based, China-focused research group MERICS, would be for the EU to join the Pacific Rim trade deal that Trump walked away from in 2017 — now known as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). “It could rejuvenate the power and the legitimacy of this trade bloc” in the wake of the American exit, Gunter said in a podcast this week. Joining a group that currently includes Japan, Australia, Canada and a number of Southeast Asian and Latin American nations, the EU would be “by far the biggest player.” This would give it the power to dictate rules and standards. While the CPTPP’s name ties it to Asia, it’s already taken on a global character with the entry of the UK, Gunter pointed out. Brussels could also make its joining conditional on China being excluded, he says. After all, the original point of the TPP was to address problems with the Chinese model. Beijing’s focus on state-supported exports arguably helped generate the overcapacity problems that contributed to Washington’s pivot to protectionism in the first place. “It could be a bold kind of approach” for the EU to jump in as a champion of trade liberalization by joining the CPTPP, Gunter says. “It’s something that could be done comparatively quickly if there’s political will.” Adams, the IIF chief, sums it up: “This is Europe’s moment. We’ll see if they actually seize it.” —Chris Anstey Qatar Economic Forum: Join us May 20-22 in Doha, where since 2021 the Qatar Economic Forum powered by Bloomberg has convened more than 6,500 influential leaders to explore bold ideas and tackle the critical challenges shaping the global economy. Don’t miss this opportunity. Request an invitation today. |