|

|

|

|

|

|

|

|

|

The Home of the Week is a Gambier Island escape that still keeps you close to Vancouver. Alena Machinskaia/Alena Machinskaia/InFrame Films

|

|

|

|

|

This week: Another steady interest rate brings more mortgage uncertainty and the loan trouble brewing for more Toronto homeowners. Plus, why AI can’t be trusted to write a will about who inherits your home, and one property worth a look. |

|

|

|

|

|

|

|

|

|

|

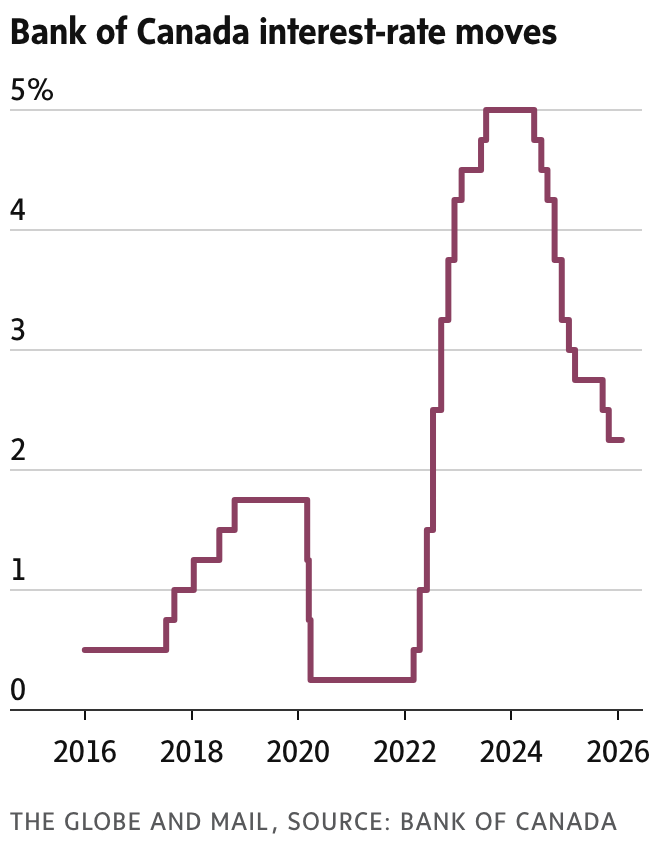

What the BoC’s decision and our ‘anything could happen’ rate future means for your mortgage |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

“If high oil prices tied to the Iran war start to translate into broader inflation, the central bank signalled it’s prepared to hike,” Erica wrote. “If trade tensions with the U.S. worsen and the Canadian economy weakens further, it may decide to cut rates to stimulate growth. On the other hand, if inflation pressure remains limited to the energy sector and trade negotiations keep muddling, expect more rate holds.” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Should you let AI help with your will? Homeowners, be careful |

|

|

|

|

|

|

|

|

|

AI chatbots can help with basic estate planning research, but using them to write your will is a recipe for added grief. useng/iStockPhoto / Getty Images

|

|

|

|

|

Who gets your home when you die? If you want your will to be clear, don’t let AI write it for you. More and more people are turning to platforms like ChatGPT to help with their estate planning, and as Zarif Sinha was surprised to learn, estate lawyers are optimistic about it – “especially about how it could help clients better understand their needs before meeting a lawyer,” he told me. |

|

|

|

|

But using AI chatbots to entirely replace lawyers in the tricky process of will-writing could cause more grief down the road, particularly for homeowners. In a recent experiment, Hannah Solmon, an estates litigator with Scion Law LLP in Vancouver, asked ChatGPT and Microsoft Copilot to draft a will for a scenario similar to a recent court battle in Ontario. Both of them failed to use precise-enough language about the home to avoid the ambiguity at the centre of Mansour v. Girgis, which locked the estate and deceased’s siblings in a 12-year dispute. |

|

|

|

|

So while AI can help with basic research, make sure you’re talking to a lawyer before signing anything. “The last thing anyone wants is go through a lengthy lawsuit over a house or property when they’re also grieving the loss of a loved one,” Zarif said. Too true, and it’s why, even if the technology improves by the time Zarif is ready to plan his estate, he says he’ll still be talking to a lawyer. |

|

|

|

|

This week’s lowest fixed and variable mortgage rates in Canada |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nearly 1 in 10 Toronto mortgage-holders won’t be able to refinance next year, BoC says |

|

|

|

|

|

|

|

|

|

Homeowners in the Toronto area are defaulting on their mortgages at a faster than across the country, and depressed home values could mean more missed payments are ahead. Melissa Tait/The Globe and Mail

|

|

|

|

|

Depressed home values in Toronto aren’t just a problem for homeowners looking to sell. If they remain at current levels, 9 per cent of mortgage-holders in the area won’t be able to refinance or renew their loans with a new lender in 2027, the Bank of Canada estimated in a new report. As Rachelle Younglai reports, that’s more than double the estimated national rate of four per cent. |

|

|

|

|

Home prices have been declining for the last four years, and the Toronto region has seen some of the steepest drops. The typical home price is 33 per cent below the peak in March, 2022, and those who took out a five-year mortgage will have to renew next year at a higher rate, one the BoC has warned could climb even higher. |

|

|

|

|

And as homeowners in Toronto default on their mortgages at a faster pace than the rest of the county, more missed payments lie ahead if values don’t increase, according to the BoC. The loan-to-value ratio, a key lending metric, has worsened for those borrowers whose homes are now worth less than when they bought them. Any ratio above 80 per cent is considered risky, and those in the higher range won’t have the option to refinance by taking equity out to pay off some of their debts, lengthening the term of the mortgage or simply renewing with a different lender. Read the full story about the BoC’s estimates here. |

|

|

|

|

|

|

|

|

|

|

The Canadian roots of the chair on every patio – and three elevated alternatives |

|

|

|

|

|

|

|

|