|

Hi friend,

I am still in the afterglow of the Berkshire AGM.

I think Greg Abel has the world’s biggest shoes to fill.

The new Berkshire CEO won’t ever be like Warren Buffett.

However, Warren Buffett truly admires Greg Abel.

Here’s what Warren recently said: “I’d rather have Greg handling my money than any of the top investment advisors or CEOs of the United States.”

As an investor, I find this very important.

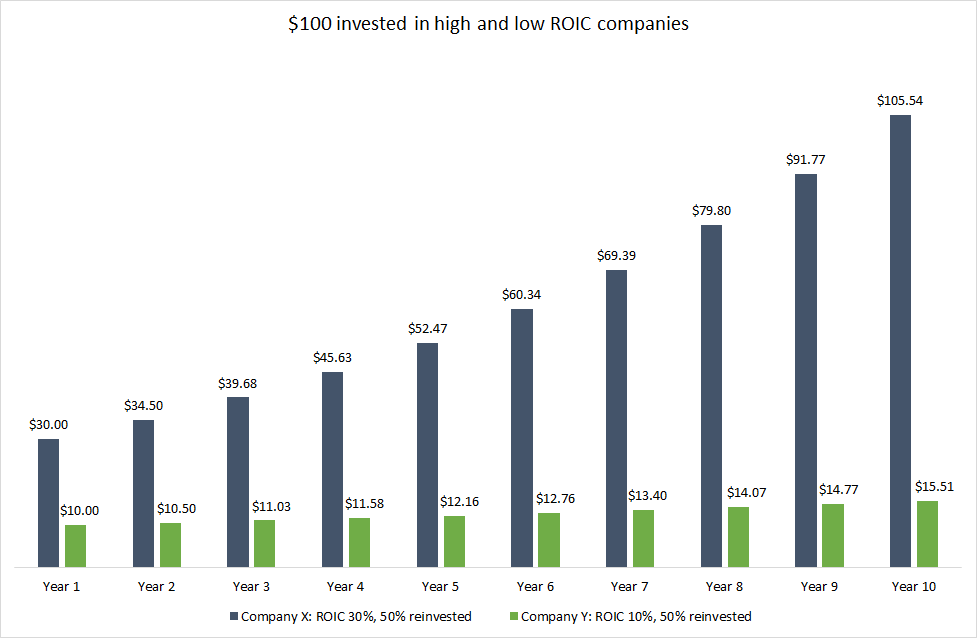

The most important task of management is capital allocation.

You can measure this by the ROIC as an investor.

And you know what?

A high ROIC consistently translates into incredible returns for shareholders.

It’s easy to see why Buffett would trust a smart capital allocator like Greg.

|

Smart capital allocators are contrarian at heart.

They are fearful when everyone else is greedy.

They’re not in a hurry to buy overvalued businesses they don’t understand.

Instead, they wait for world-class businesses to drop below their fair value.

This can sometimes mean doing nothing when other CEOs are buying.

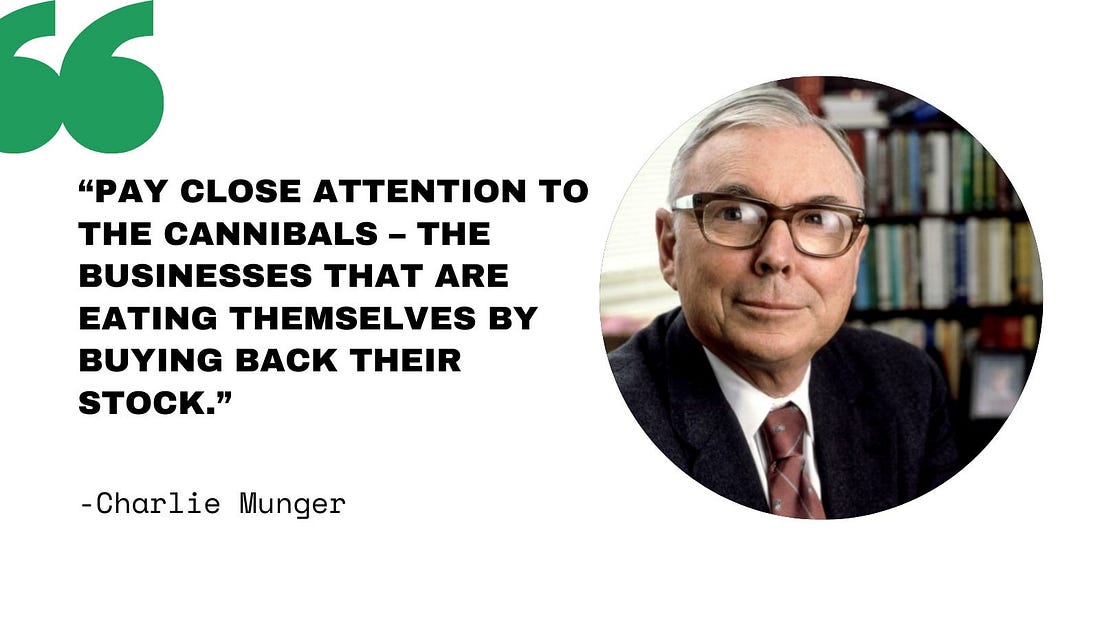

Or, as Charlie Munger would say:

It could mean sitting on your ass for a very long time.

This conservative approach doesn’t appeal to investors looking for constant action.

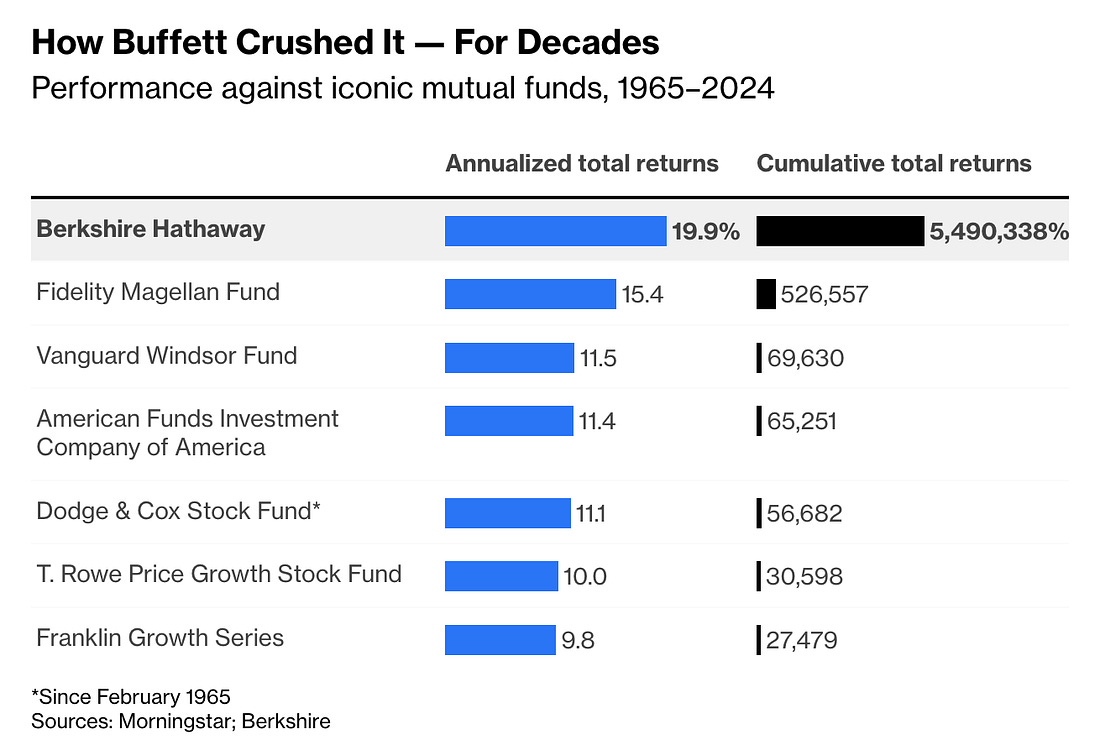

However, as Berkshire’s superior historical returns prove…

Investors who trust smart capital allocators win in the long run.

|

That’s why I’m so confident in the companies inside our portfolio.

Our Companies are run by some of the smartest capital allocators in the world.

That would explain the high returns on invested capital (ROIC).

(And the steady growth in shareholder value since we bought them).

Take the Consumer Staple Stock we added to our portfolio in January 2025.

It’s the perfect example of a serious cannibal.

That’s a company that eats itself by buying back shares aggressively.

If you’re an investor with a long-term view, this can be a good thing.

Why?

Because when a company eats itself by retiring shares…

|

Your percentage ownership of the business grows automatically.

Your Dividends Per Share (DPS) also increase because there are fewer shares outstanding.

That’s been the case with the Consumer Staple I mentioned earlier.

The stock is up 77% since we started buying it in early 2025.

The company also pays a 5% dividend yield.

That’s nearly 3x the market average.

But its new buyback program could create even more value for shareholders.

Around $1.7 billion has been set aside for share buybacks through the end of 2026.

It is a high-margin, consistent cash-cow business that fits our value investing criteria.

And as a Consumer Staple, it’s positioned to perform well even during economic downturns.

With a little guidance, you can buy the stock at a discount while it increases dividends annually.

How?

|

Give Compounding Dividends a try.

With a risk-free trial, you’ll get the full case study of the stock I just told you about.

We focus on companies that consistently increase dividends for shareholders.

How are they able to do this regardless of economic conditions?

There are several reasons, but I’ll give you 3.

Industry dominance, low costs, and high-profit margins.

This unique combination lays a strong foundation for incredible long-term returns.

That’s why I’m so confident in the 18 companies we own.

The moment you start your risk-free trial, you get full access to our portfolio.

You’ll get detailed investment cases for all our positions.

You’ll also get the reports for any new investments we make.

This way, you can follow along and be up-to-date on everything we do.

So, how much are you investing today?

Normally, you pay $499 for access to Compounding Dividends.

But Pieter and I returned from Omaha feeling very inspired.

|

Personally, I’ve learned a lot from Warren Buffett.

He’s been the biggest inspiration for my most successful investments.

And to show my gratitude, I want to give you a serious discount.

Here’s what this means.

If you act now, you pay only $399 for Compounding Dividends.