|

MAIN FEATURE

THE 5 ELEMENTS OF A SELF-SUSTAINING WEALTH FLYWHEEL

Wealth is not something you accumulate.

People think you earn money, you save money, you invest money, and eventually you end up with enough of it. And the fact that that's how people think wealth works is precisely the reason why they don't have very much of it.

The truth is wealth is something you engineer. And the difference between someone who earns a lot and someone who builds a lot comes down to one thing: the velocity of their money.

A dollar sitting still is dying. A dollar in motion creates wealth.

But you've heard that before. Get your money working for you. Sure. So you buy some stocks. Maybe some equipment for the business. And that's fine, but that's not the point. The point isn't just to do something productive with your money.

The point is to build a system.

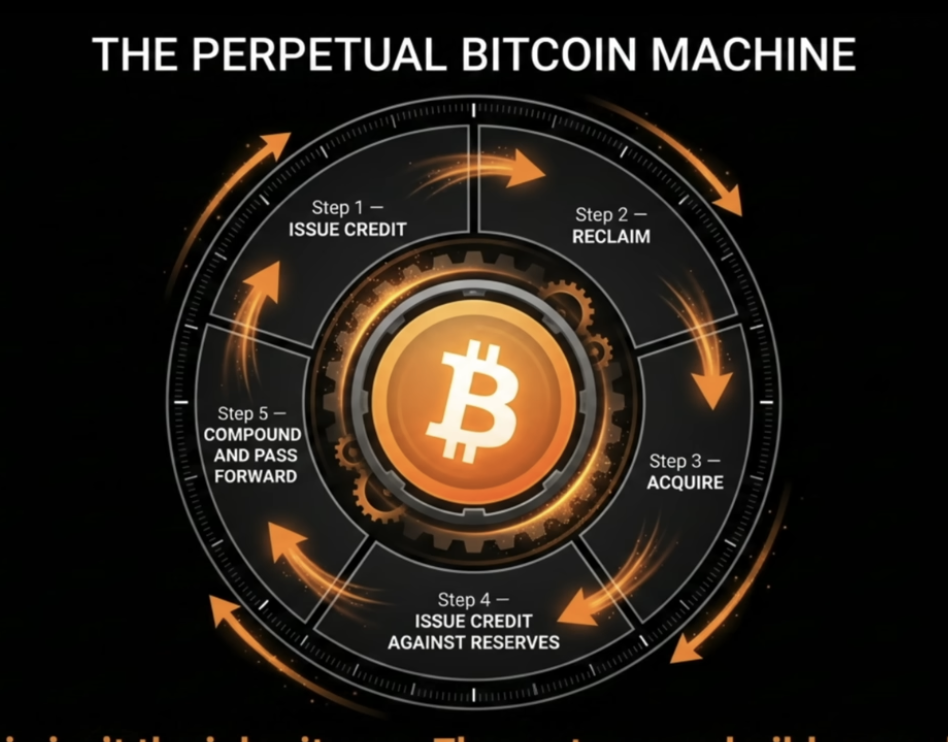

There are five steps in a wealth system. I call it the Wealth Flywheel.

Step 1: Issue Credit

Having money and having access to money are not the same thing.

We live in a debt-based monetary system. What the wealthy understand is that it's not about making more money. It's about knowing how to unlock liquidity to access capital.

Capital has a price. If you can deploy it at a return higher than that price, the spread belongs to you. Consumer debt works against you. Credit deployed into assets that produce more than they cost builds wealth. Same instrument, completely different outcome.

Step 2: Reclaim

The whole goal of a wealth system is to fund your life with assets instead of income.

Inflation is going to continue driving asset prices up. If you unlock liquidity against your assets to fund your lifestyle, rising prices become a good thing. So the name of the game is accumulating enough assets to fund your lifestyle as fast as possible.

Most people hear that and think, “OK, Bitcoin is at $80k right now so if I want to buy another Bitcoin I have to come up with another $80k.”

That’s a big task.

But the average person reading this right now probably pays that much in taxes every year. What if instead of figuring out how to make more, you just reclaimed what you're already giving away?

The tax code is not written to punish you. It's a list of incentives. A list of behaviors the government wants more of, and will reward you for doing.

People who understand this use those incentives to legally reduce their tax burden and redirect that capital into assets instead. They didn't make a single dollar more. They just stopped letting so much of it leave.

Step 3: Acquire

Most people treat a tax refund as a bonus. Spend it, enjoy it, you earned it.

What we do is different. That reclaimed capital is how we get ahead. We deploy it into appreciating assets instead. You didn't get a raise. You didn't land a new client. You just stopped letting capital that was already yours walk out the door and put it to work.

Step 4: Issue Credit Against Reserves

Here's where the flywheel begins.

Accumulation is linear. The flywheel is not. Once you own appreciating assets, the financial system will lend against them. Those assets become collateral. New credit gets issued without selling the asset, without giving up the appreciation, without breaking the position. The asset grows, the credit capacity expands, new capital enters the machine, and the cycle starts again.

You're not spending the asset. You're using its growth to fund the next rotation.

Step 5: Compound and Pass Forward

The traditional model says you save and invest, then retire by slowly selling your assets. You spend down the portfolio and hope you die before you hit zero. And then you leave nothing to your kids.

The problem is compounding isn't linear. The moment you start selling is precisely when compounding is accelerating the fastest. You're killing it at its peak.

The flywheel keeps compounding intact. You never have to sell. Every year your returns get bigger. And then you pass it forward, not just the assets but the system. The knowledge. The understanding that you never sell. Their kids do the same. And their kids after that.

That's not an inheritance. That's a legacy that changes the course of a family forever.

Nearly everyone I work with all have one thing in common: they work really hard for their money and they wonder, "Am I doing the most I can to put it to use or am I leaving money on the table?"

I can't answer that for you. Every situation is different.

But these five jobs are the starting point. Figure out what jobs your money is currently doing. And whatever is not getting done, now you know where to start building.

|