|

|

Hi Friend 👋,

Yesterday I told you about my trip to Berkshire Hathaway.

It’s amazing how much talent is in Omaha during this weekend:

Hedge fund managers like Bill Ackman.

Tim Cook, Apple’s CEO

François Rochon, founder of Giverny Capital

And many more

As my AirBNB was only 15 minutes away from Warren Buffett’s house, I decided to go for a run and visit his house:

|

I took a lot of notes during the Berkshire weekend.

And I want to share a lesson with you.

Since Buffett announced his retirement, you might have asked yourself: Will Berkshire Hathaway outperform over the next 10 years?

I am quite sure they will.

And I’ll give you my reasoning.

It is something few people pay attention to.

I’m talking about Berkshire Hathaway’s float.

The float is the secret sauce of Berkshire Hathaway.

It’s what makes them outperform the market.

Let me explain it to you.

Float is something common with insurance companies.

It is the money they receive today, but don’t have to pay out until later in the future.

For example, customers pay premiums upfront to insure their health, cars, houses, pets, etc.

But you only pay if something bad happens.

In the meantime, Berkshire Hathaway can invest this money.

It’s exactly what makes them so valuable.

This explains Berkshire’s incredible returns over the years.

|

I believe the performance will remain strong with Greg Abel at the helm.

As Buffett told investors recently:

“Greg is doing everything I did and then some. He’s doing it better in all cases.”

In other words, the core business principles have not changed.

Berkshire Hathaway will continue to thrive in the years ahead.

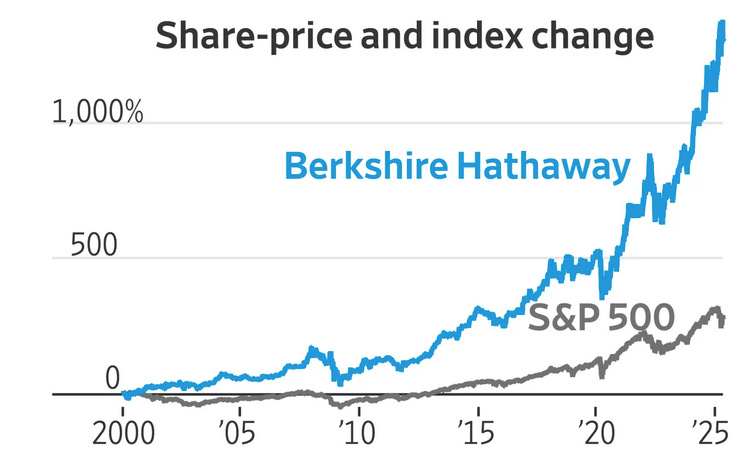

Now, in the past year, Berkshire has underperformed the S&P 500 by around 40%.

The last time something like this happened? In 1999.

The years thereafter they massively outperformed the market.

Berkshire was sitting on a pile of cash back then (just like today).

In the midst of the dotcom bubble, Berkshire refused to buy mediocre businesses at unreasonable prices.

But as soon as valuations reconnected with business fundamentals…

The company started buying world class businesses trading below their fair value.

The results?

If you invested $10,000 in Berkshire in 1999...

Your investment would be worth around $400,000 today.

That’s a 40-bagger!

That’s an unparalleled investing record.

But what about the future?

Can we expect similar returns in the years ahead?

Berkshire is sitting on a record cash pile of almost $400 billion.

|

Like Buffett, Greg is only interested in buying the best companies at a fair price.

Most of the businesses Berkshire could buy are still overvalued today.

This explains his patience, and the company’s cash pile.

It is a conservative approach that doesn’t appeal to most investors.

But when you look at Berkshire’s historical returns, you know it works.

The “Other” Berkshire.

But it gets even better.

I found a company I believe will be The Next Berkshire Hathaway.

Over the past 3 decades, it has returned +14,000% to shareholders.

That’s a return of 18% per year.

|