|

The Best Retirement Account in America Is Hiding in Your Health Plan

It's called an HSA. Almost nobody uses it for what it's actually worth.

Quick question for you. What if I told you there’s a retirement account that does all three of these things at the same time?

•Lowers your taxable income the year you contribute.

•Grows tax-free for decades.

•Comes out tax-free when you spend it.

Sounds fake, right? It’s not. There’s no waitlist, no income cap that locks you out, and your employer is probably already offering it. You’re just walking past it because it’s wearing a costume that says “health insurance.”

Welcome to the Health Savings Account.

The triple tax advantage, in plain English

A 401(k) and a Roth IRA each give you two tax breaks. The HSA gives you three:

•Money goes in pre-tax (federal, and in most states).

•Investments grow with zero tax drag.

•Withdrawals for qualified medical expenses are tax-free, forever.

No other account in the U.S. tax code does all three. Not even close.

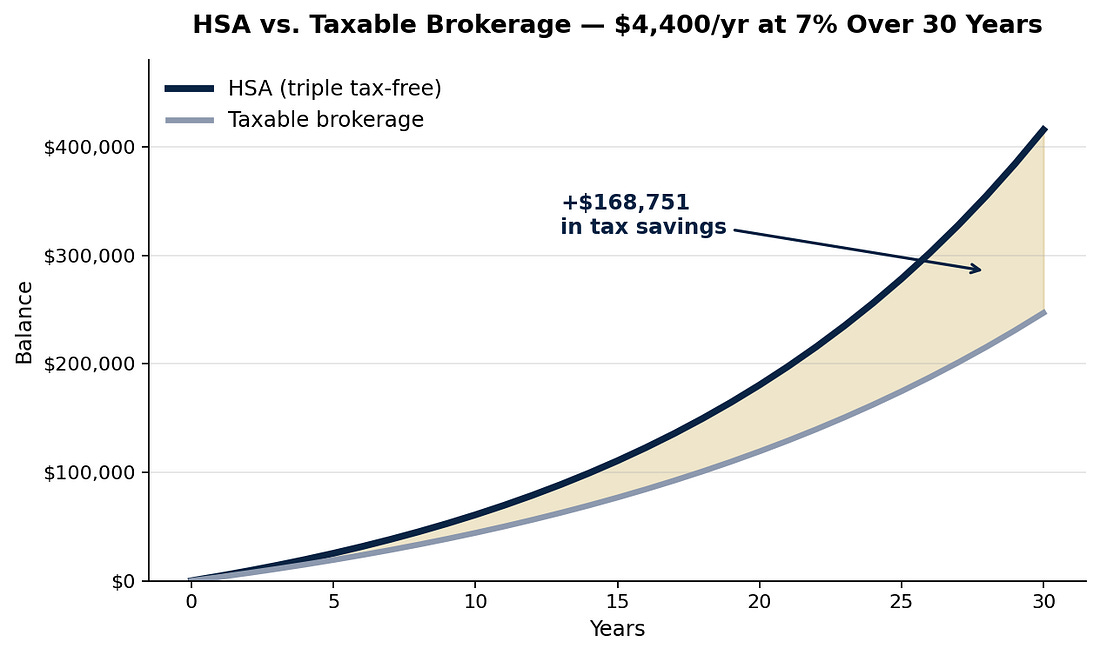

|

That gold band is tax savings, compounding for three decades. While your coworker is paying capital gains every year on their taxable account, your HSA is quietly stacking.

The catch (and why most people miss it)

To contribute, you need to be enrolled in a high-deductible health plan (HDHP). In 2026, the IRS lets you put in $4,400 if you have self-only coverage and $8,750 for family coverage. People 55 and older get an extra $1,000 catch-up.

Here’s the part nobody tells you: most people who have an HSA use it like a checking account. They contribute, then immediately swipe the debit card at CVS. That defeats the entire point.

The “shoebox method” wealthy people quietly use

Pay your medical bills out of pocket. Save the receipts. Shove them in a shoebox (or, you know, a Google Drive folder).

Let the HSA invest in index funds for 20 to 30 years. Then, in retirement, you can reimburse yourself for those old receipts — tax-free — and pull cash out anytime. There’s no expiration date on the receipts. It’s effectively a stealth Roth IRA wrapped in a medical disguise.

Action this week: Check if your health plan is HSA-eligible. If yes, max it before maxing your IRA. If your HSA is at a no-investing custodian (Optum, HealthEquity at default), transfer it to Fidelity — zero fees, full brokerage. Takes 15 minutes.

Why this actually matters

Healthcare in retirement is projected to cost the average 65-year-old couple roughly $315,000 over their remaining life. The HSA is the only account specifically designed to crush that bill — tax-free, on both ends.

Most people will retire and pay that bill out of taxable money. You don’t have to.

Sources

•Fidelity — 2026 HSA contribution limits — https://www.fidelity.com/learning-center/smart-money/hsa-contribution-limits

•IRS Publication 969 — Health Savings Accounts — https://www.irs.gov/publications/p969

•Fidelity Retiree Health Care Cost Estimate — https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

Disclaimer

Affluent Notes is for educational and entertainment purposes only. Nothing in this newsletter is financial, tax, legal, or investment advice. The numbers, charts, and strategies discussed are illustrative; your situation, tax bracket, plan rules, and risk tolerance are different. Past performance does not guarantee future results. Talk to a licensed CPA, CFP, or attorney before acting on anything you read here. The author may hold positions in securities or accounts mentioned.