|

|

|

|

|

|

|

|

|

Nuthawut Somsuk/iStockPhoto / Getty Images

|

|

|

|

|

Oh, hi again. And happy day-after tax deadline day! Make sure you take at least 24 hours before you start stressing about next year’s tax filing. Today, we’re getting into how changes to federal worker programs could impact retirement plans. |

|

|

|

|

A pension shakeup is brewing |

|

|

|

|

You may not spend a lot of time thinking about what your retirement income will look like day-to-day. Until something shifts, and suddenly, it matters a lot. That’s what’s happening right now for some federal public servants. |

|

|

|

|

This week, I reported that Ottawa is in talks with unions about changing how federal public-service pensions will work going forward. Unions are warning the changes could mean lower benefits down the line. |

|

|

|

|

Here’s the backstory for the uninitiated: Federal workers build retirement income from two main pieces, the Canada Pension Plan (or Quebec Pension Plan) and their public-sector pension. Together, those are designed to add up to 2 per cent of a worker’s average salary for every year of service. |

|

|

|

|

There’s a wrinkle, though. Between 2019 and 2025, the government expanded CPP benefits but didn’t adjust public-sector pensions to match. The result is workers have been contributing more than needed to their workplace plans and, in return, earning slightly richer benefits. The government has been matching those higher contributions — costs funded by taxpayers. |

|

|

|

|

A report from the Parliamentary Budget Officer estimates the extra contributions to federal pensions from public servants and the government amount to about $2-billion. |

|

|

|

|

Now, the government is looking at ways to bring things back in line with that 2-per-cent target and has presented options to unions on how to get there. |

|

|

|

|

All of this is happening at the same time as a broader push to shrink the public service, with plans to cut tens of thousands of jobs and offer early retirement incentives. |

|

|

|

|

For example, public servants will have until July 24 to apply for an early retirement incentive from the federal government. One report said 3,700 federal workers have already applied for the program. |

|

|

|

|

|

|

|

|

It raises a bigger question: how many federal employees are rethinking their retirement plans because of all this? |

|

|

|

|

If you’re a public servant and this is affecting your decisions, whether you’re considering early retirement or changing your timeline, I’d love to hear from you. Reach me at mraman@globeandmail.com. |

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

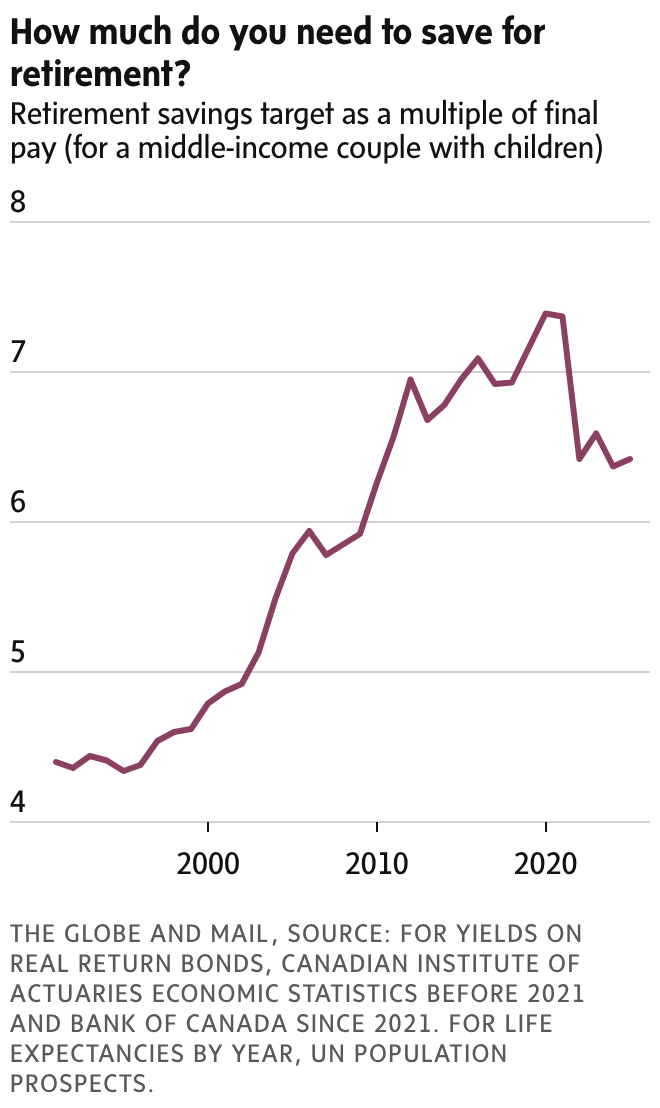

Canadians may not need to save quite as much for retirement as a few years ago, says Frederick Vettese, former chief actuary at Morneau Shepell. A typical savings target is now around 6.4 times final pay, down from about 7.2 times in 2020. |

|

|

|

|

Yes, but: That doesn’t mean retirement is getting cheaper overall. Savings targets can swing widely depending on interest rates and how long you expect to be retired, so relying on a single rule of thumb can still leave you short. |

|

|

|

|

|

|

|

|

|

|

This week, I co-hosted Stress Test (The Globe’s personal finance podcast for Gen Z and millennials) and we took on one of the biggest (and most anxiety-inducing) questions out there: how much do you actually need to retire? |

|

|

|

|

You may have seen that $1.7-million number floating around from a recent big bank survey. It’s large, it’s intimidating, and honestly, it can make it feel like you’re already behind. So we dug into it. |

|

|

|

|

We heard from young Canadians imagining very different versions of retirement, and I sat down with financial planner Moira Rose Váně to challenge the notion there is a one-size-fits-all way to retire comfortably. |

|

|

|

|

Give it a listen and let me know what you think. |

|

|

|

|

|

|

|

|

|

|

|

|