|

Admiral Group has nearly 12 million insurance policies, and structural cost advantages.

Despite record profits, it’s got a yield over 6% because of worries about rising claims inflation and new regulatory pressures.

Is this industry leader a buy? Let’s find out!

: Company Profile, Stock Price, News, Rankings | Fortune") |

Admiral Group PLC

Admiral is a leading insurance provider that uses technology to keep costs low.

It then passes those savings along to customers.

While they are famous for car insurance, they have spent the last few years branching out into home insurance, pet insurance, and personal loans.

They share a lot of the risk with other big global insurance partners through reinsurance agreements.

That allows Admiral to focus on what they do best - using data to pick the safest drivers and give them great customer service.

Company name: Admiral Group PLC

✍️ ISIN: GB00B02J6338

🔎 Ticker: $ADM

📚 Type: High yield stock

📈 Stock Price: £32.39

💵 Market cap: £9.8 billion

📊 Average daily volume: £34 million

Onepager

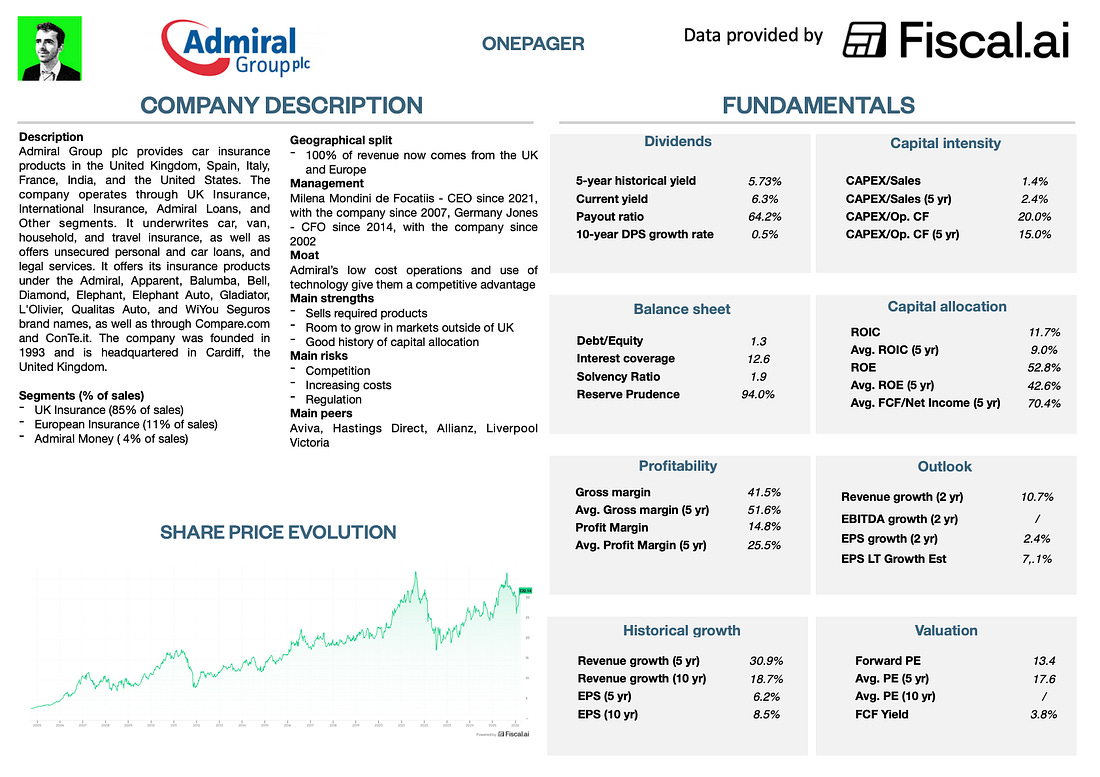

Don’t know Admiral Group?

Here are the basics (click on the picture to expand):

|

Now let’s dive into the full investment case!

1. Do I understand the business model?

Admiral makes most of their money from selling car insurance, but it’s really a data company.

They use over 120 different AI and machine learning models to pick the safest drivers, and figure out exactly how much to charge each person based on their risk of having an accident.

Unlike traditional insurers that keep all the risk on their own books, Admiral uses reinsurance.

|

In 2025, they used reinsurance deals to pass 78% of their UK car insurance risk to other partners.

This makes the business much safer and allows them to pay out most of their profits as dividends to shareholders.

Revenue Split

Most of the revenue (which they call turnover) comes from UK car insurance.

Here is the split for the 2025 fiscal year:

UK Insurance (Motor, Home, Pet): £5 billion (85% of turnover)

European Insurance (Italy, France, Spain): £674 million (11% of turnover)

Admiral Money (Personal Loans): £226 million (4% of turnover)