Brex’s $5.15 billion agreement to sell to Capital One isn’t the kind of exit employees or investors would have dreamed of four years ago, when it was valued privately at $12.3 billion. But it appears to be a good enough ending to the corporate credit card startup’s run as a private company. For one, the half-cash, half-stock deal gives Brex shareholders the kind of instant payday another private round or initial public offering wouldn’t. The company had raised $1.3 billion in venture capital, corporate filings show, from investors such as Greenoaks and Tiger Global Management. That means early investors will do well and later investors will at least get their money back, due to liquidation preferences.

Brex’s $5.15 billion agreement to sell to Capital One isn’t the kind of exit employees or investors would have dreamed of four years ago, when it was valued privately at $12.3 billion. But it appears to be a good enough ending to the corporate credit card startup’s run as a private company.

For one, the half-cash, half-stock deal gives Brex shareholders the kind of instant payday another private round or initial public offering wouldn’t. The company had raised $1.3 billion in venture capital, corporate filings show, from investors such as Greenoaks and Tiger Global Management. That means early investors will do well and later investors will at least get their money back, due to liquidation preferences.

Greenoaks, one of Brex’s largest investors, will return twice its investment across its funds invested in Brex, a person familiar with the matter said. It first invested in the startup’s $1 billion valuation round in 2018, and it later poured in money at higher prices. (It’s worth noting, of course, that the Nasdaq Composite has roughly tripled since 2018.)

Employees appear poised to do at least OK as well. After Brex hit major speed bumps in 2022 and 2023, it repriced employees’ options to keep them from going underwater, a person close to the company said.

What also makes the sale less jubilant is the Ramp of it all. Brex’s rival, with which it formerly competed neck and neck, has raised money at an ever-increasing valuation, most recently $32 billion, and has grown faster. Ramp executives and investors took a victory lap about Brex’s sale on X. (Classy.)

Brex, for its part, seemed to realize a couple years ago that the time for dreaming was over, and it was time to get real. The company laid off 20% of its staff in early 2024, a painful moment that seemed to refocus it. Co-founder Henrique Dubugras told my colleague Abram Brown soon after that: “Look, people come to work for you—you sell them a dream, and they come to work for you. And this was no one’s expectation when they joined.”

Today’s sale price wasn’t the dream Dubugras likely envisioned. But it made the most of the startup’s current reality. —Cory Weinberg

Now, onto today’s column.

Over the last year, our reporters have regularly scooped news about venture firm partners leaving to launch their own funds. While there’s no sign of that trend letting up, new data underscore just how challenging it is for VC managers to keep raising more money to make new investments—particularly if they have only raised one or two funds.

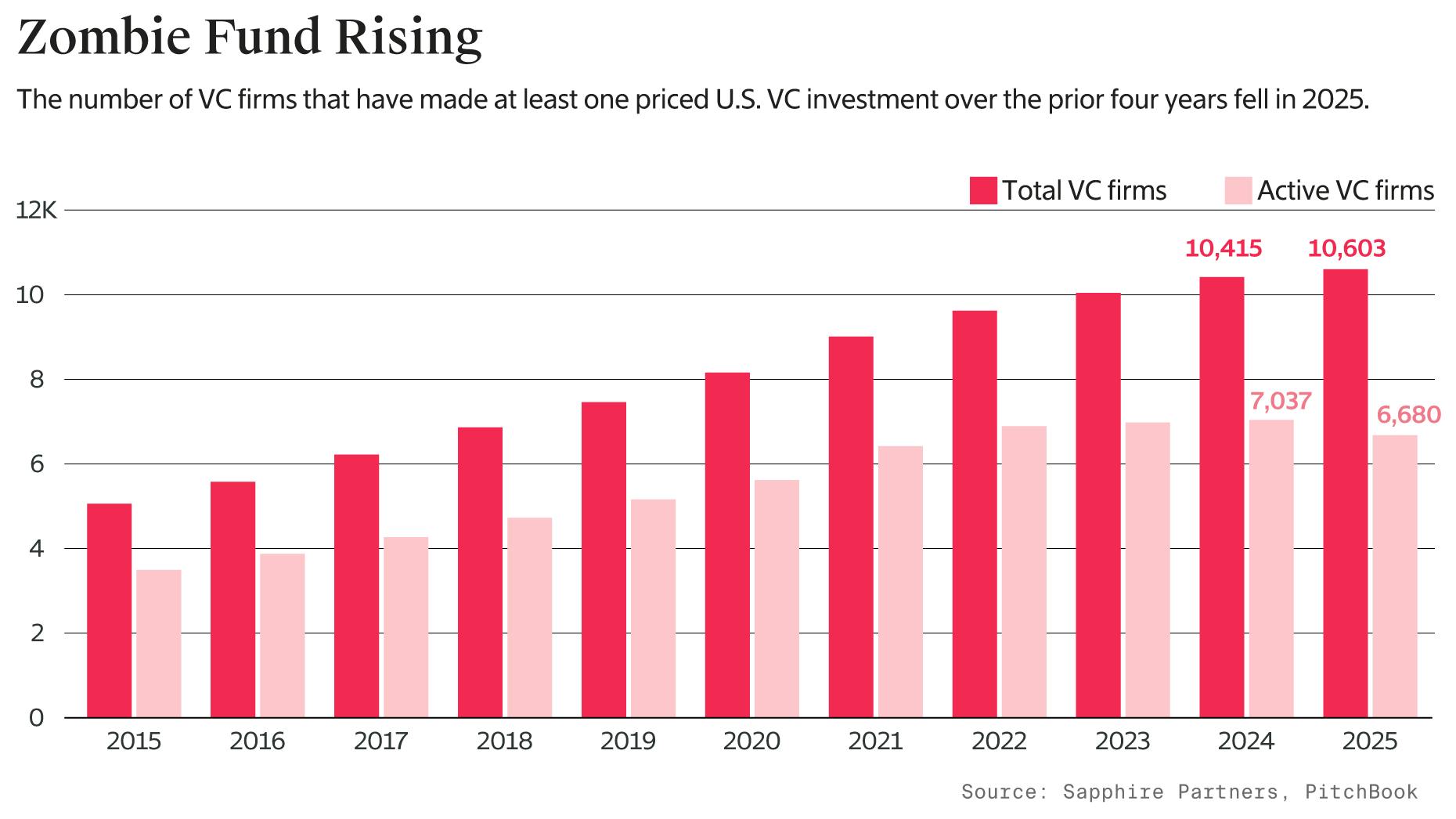

Sapphire Partners, a limited partner in early-stage VC funds, analyzed two decades of PitchBook data on fund formation and investments as well as its own data. It found that the number of VC firms in the U.S. has continued to rise, topping 10,600 last year. But Sapphire also found that active funds fell for the first time in at least a decade. It defined active funds as those that made an investment at a certain price in the past four years; many of those funds also likely made unpriced investments, such as entering simple agreements for future equity (SAFE contracts).

VC funds that aren’t making new investments are sometimes termed zombie funds. Their partners can continue to manage past investments and earn management fees. But without fresh capital, their hope of making new investments dries up.

“We’ve always had the haves and have-nots,” said Beezer Clarkson, the partner at Sapphire Partners who analyzed the data, referring to funds that are able to outperform and raise more capital and the ones that don’t. “But we haven’t actually had a contraction [before]” in the number of active funds.

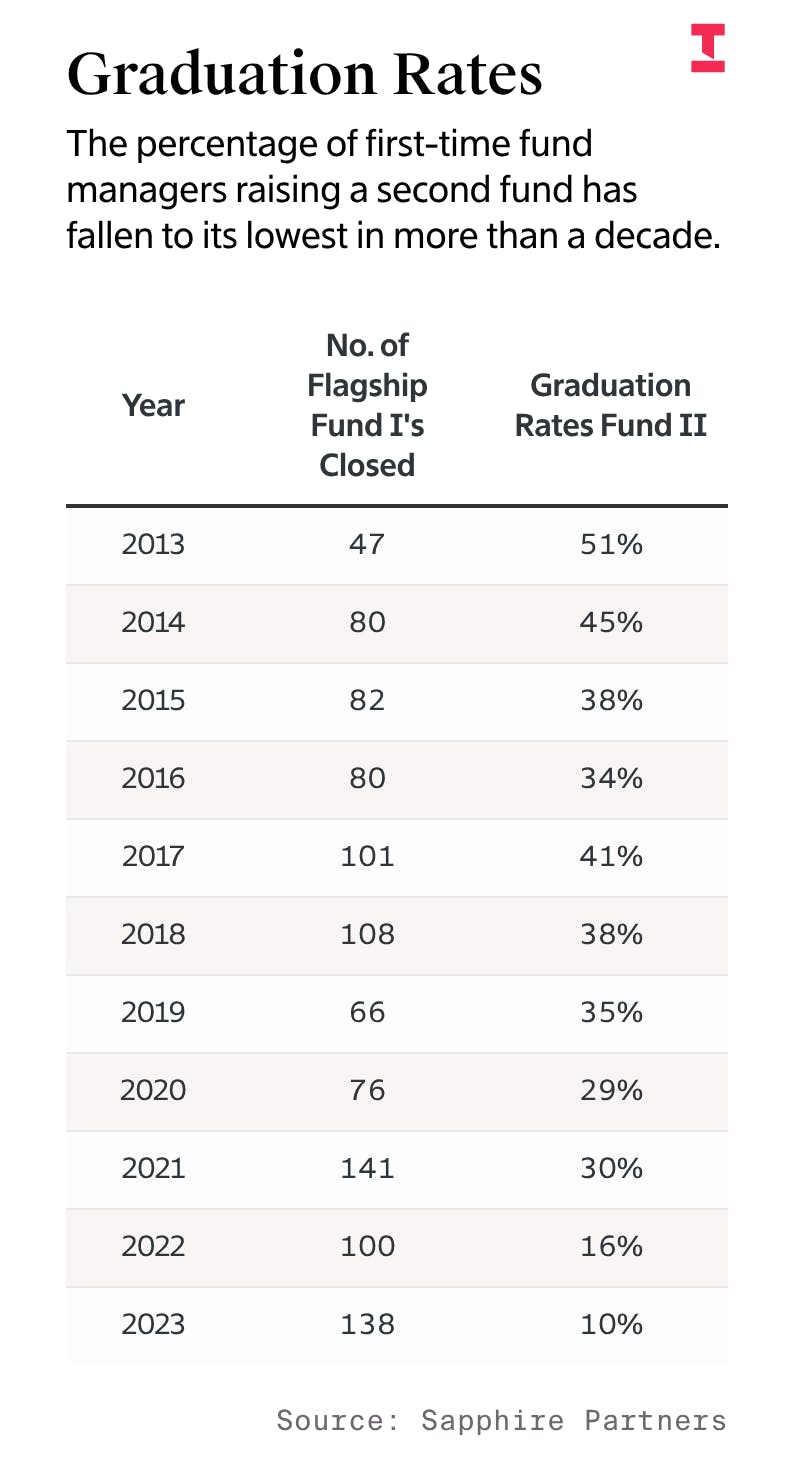

This drop in active funds follows a surge in new VC funds launched since 2020, when pandemic-era low interest rates spurred more venture capitalists to branch out on their own. In 2021 alone, first-time fund managers raised 141 new funds. But only 30% successfully raised a second fund, the lowest “graduation rate” since at least 1995, Sapphire estimates. And 2022 was worse. Of the 100 new funds raised that year, only 16% successfully raised a second fund.

Some of this contraction is a natural reaction to exuberance during the low-interest-rate period, when buoyant tech stocks and dozens of IPOs helped venture funds return cash to their backers, encouraging more managers to start their own new funds.

“New firm formation is very cyclical and tied to how the market is doing: When the market is bullish and money is coming back to [limited partners], they will take riskier bets”—say, by trying new managers, Clarkson said. “In down markets, that’s much more difficult. It’s typical to concentrate dollars.”

The data give more detail to the past year’s VC fundraising. Investments in VC funds last year fell 35% to a nine-year low, according to PitchBook. But some of the biggest firms, including General Catalyst, raised multibillion-dollar funds. At the same time, the amount of money raised by emerging fund managers sank.

Clarkson said she expects the number of active funds to keep falling until more firms are able to return cash to their limited partners thanks to mergers and acquisitions and public offerings. Deals like Brex’s sale to Capital One make her optimistic on that front.

“It would not surprise me that until we have a stronger exit market, we’ll see this contraction continuing,” she said. --Laura Mandaro

Join The Information Founder and Editor-in-Chief Jessica Lessin for a subscriber-only live session drawing on her reporting from the World Economic Forum in Davos.