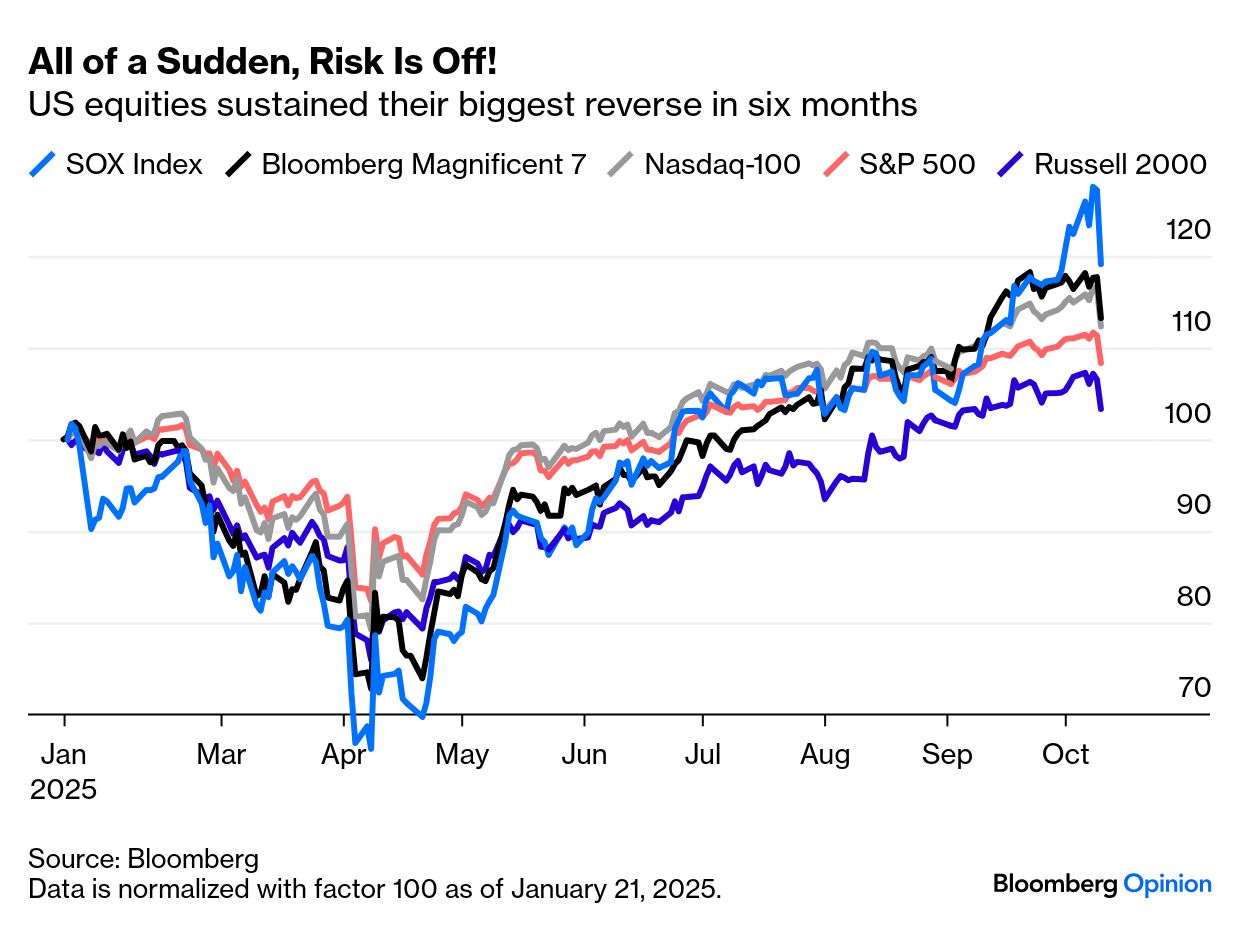

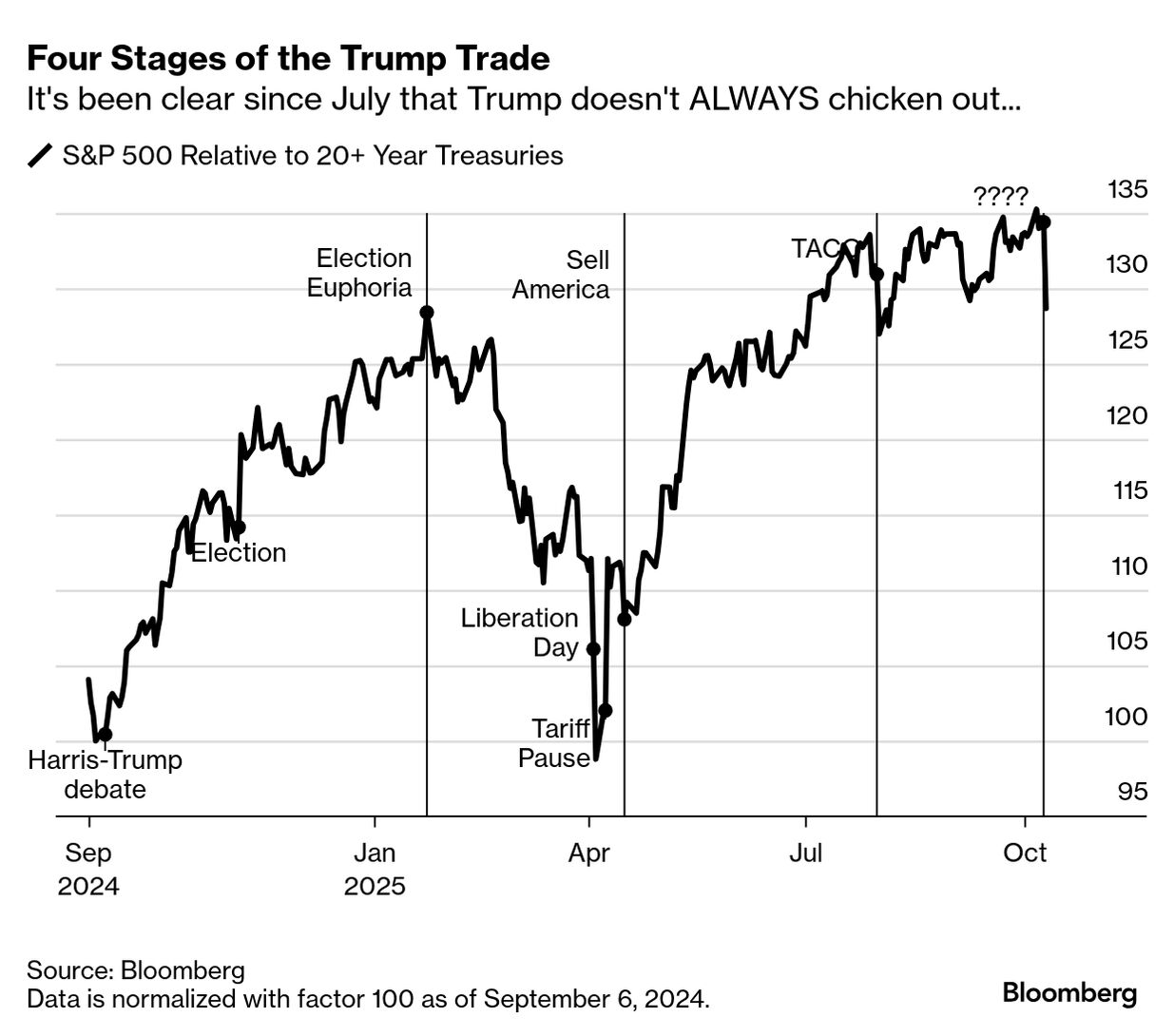

| At last we can explain why markets have been behaving as though all uncertainty over trade policy and tariffs had been resolved, even though it clearly hadn’t. Mr. Market really believed it was all over. That’s clear from the extraordinary reaction to the latest trade expostulation from President Donald Trump, who will slap 100% tariffs on all Chinese imports next month in response to new restrictions on the flow of rare earths from China.

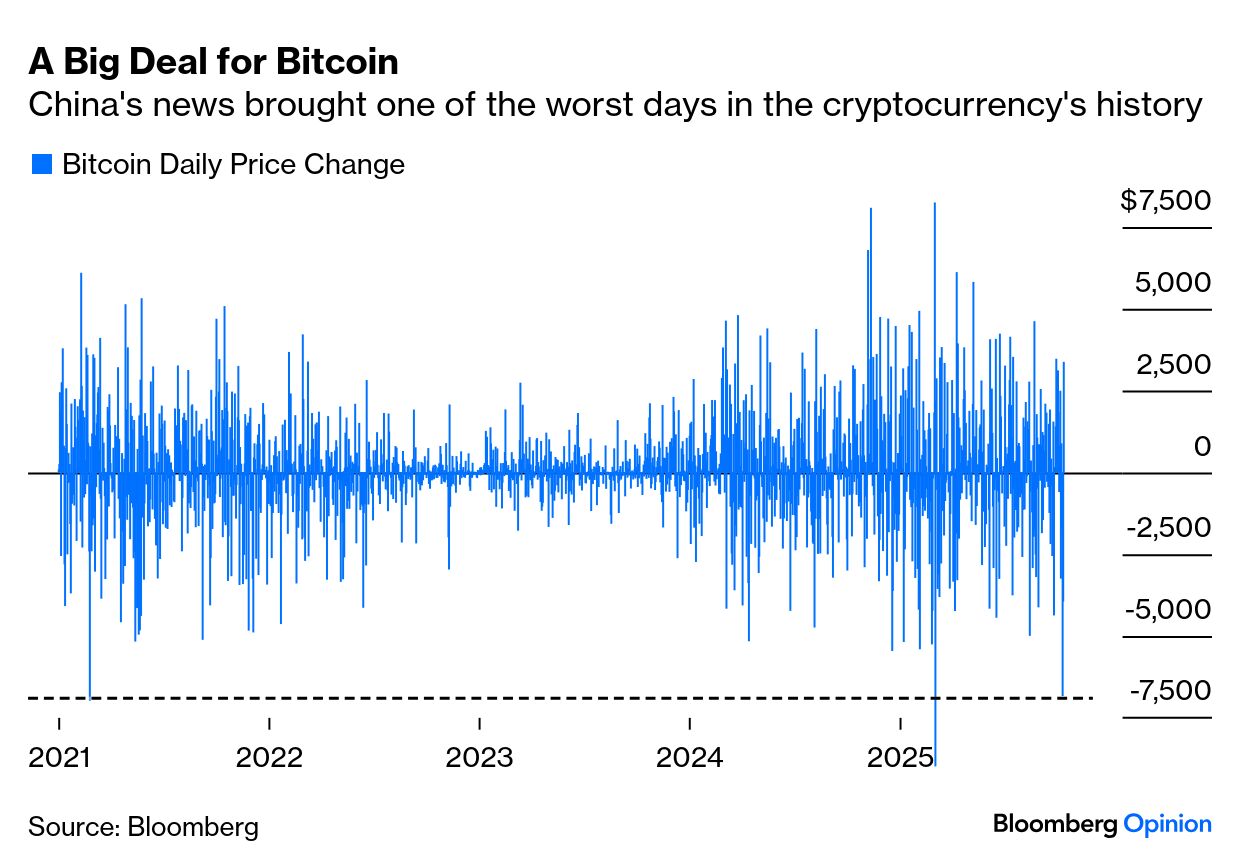

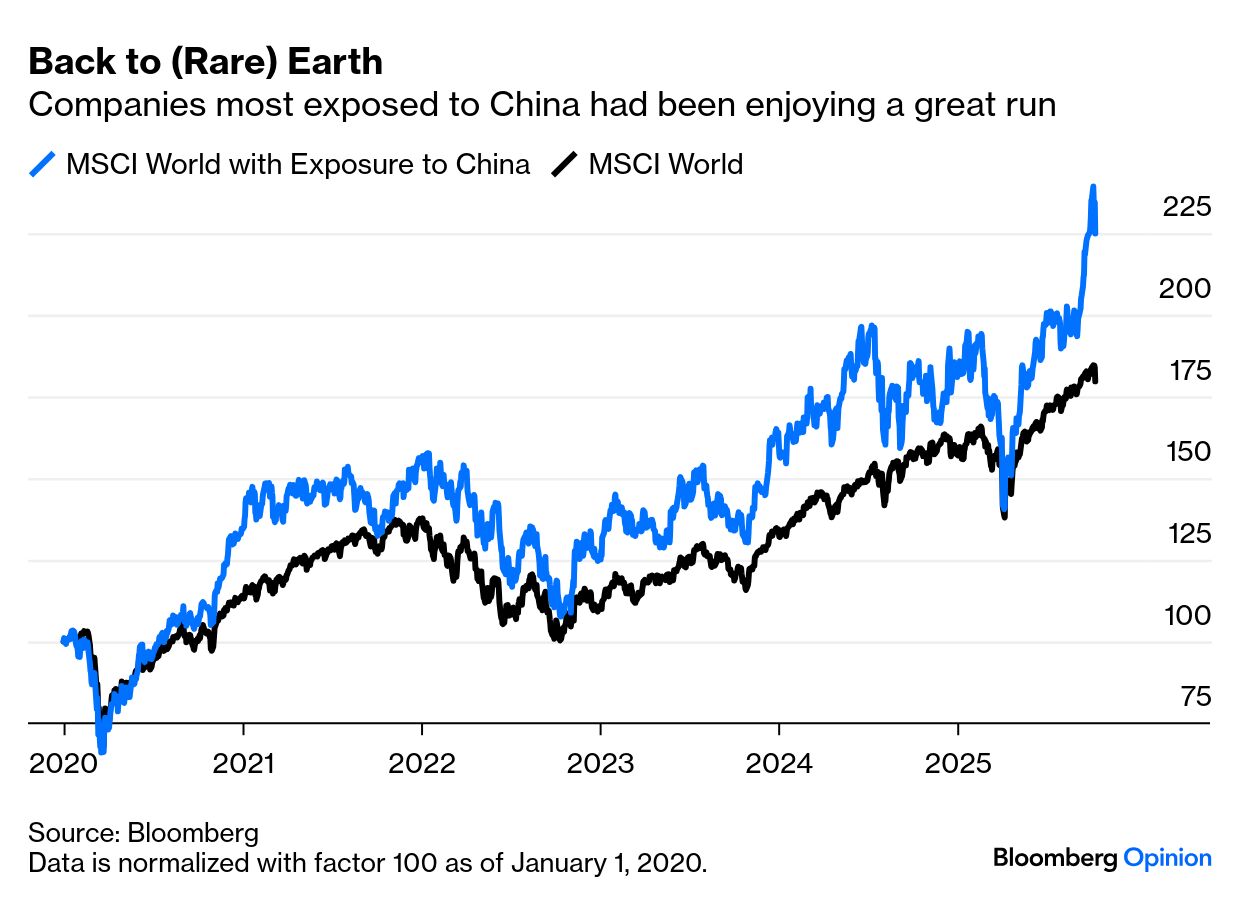

This is a big deal, which we analyze below, but the market withstood Trumpian threats of 145% tariffs on China six month ago. While there’d been a negotiating pause in trade hostilities, neither power has ever pretended to reach an ongoing, durable solution. This is bad news, but shouldn’t qualify as a major surprise. And yet US markets took a dive Friday. They’re still up for the year, and this may just be a correction, but it was drastic: Crypto had one of its worst days in history. Only once, in the wake of the Liberation Day tariffs in April, had so much Bitcoin wealth been wiped out in one day: MSCI’s index of the 100 developed-market companies most exposed to China had been rallying. It sharply reversed: The China trade conflagration may just be an excuse to take profits (and stock futures and oil enjoyed a bounce in Monday’s early Asian trading). It’s also possible that the relationship between markets and Trump 2.0 is in a new phase. So far, the response to the extraordinary upheaval in economic policy has moved in four stages: As Kamala Harris’ chances ebbed after her strong performance in the one presidential debate, markets went on a tear. Trump 1.0 was taken as a guide; he viewed stocks as a validator, so there would be a “Trump Put.” The policies investors liked — tax cuts and deregulation — would happen, while those they didn’t — tariffs and an immigration clampdown — would be watered down. The way Trump brought Silicon Valley’s lords onside boosted belief in a great pro-growth administration. After the inauguration, a rethink set in. Trump pressed on with tariffs, and said: “Markets are going to go up and they’re going to go down but, you know what, we have to rebuild our country.” The administration talked about “detox” for the economy. Trump posted about firing Jerome Powell from the Federal Reserve. Then Liberation Day on April 2, unveiling tariffs far higher than anything the administration had trailed, and a swift escalation to 145% tariffs on China, really set the cat among the pigeons. The narrative now was that money would exit America. - TACO (Trump Always Chickens Out)

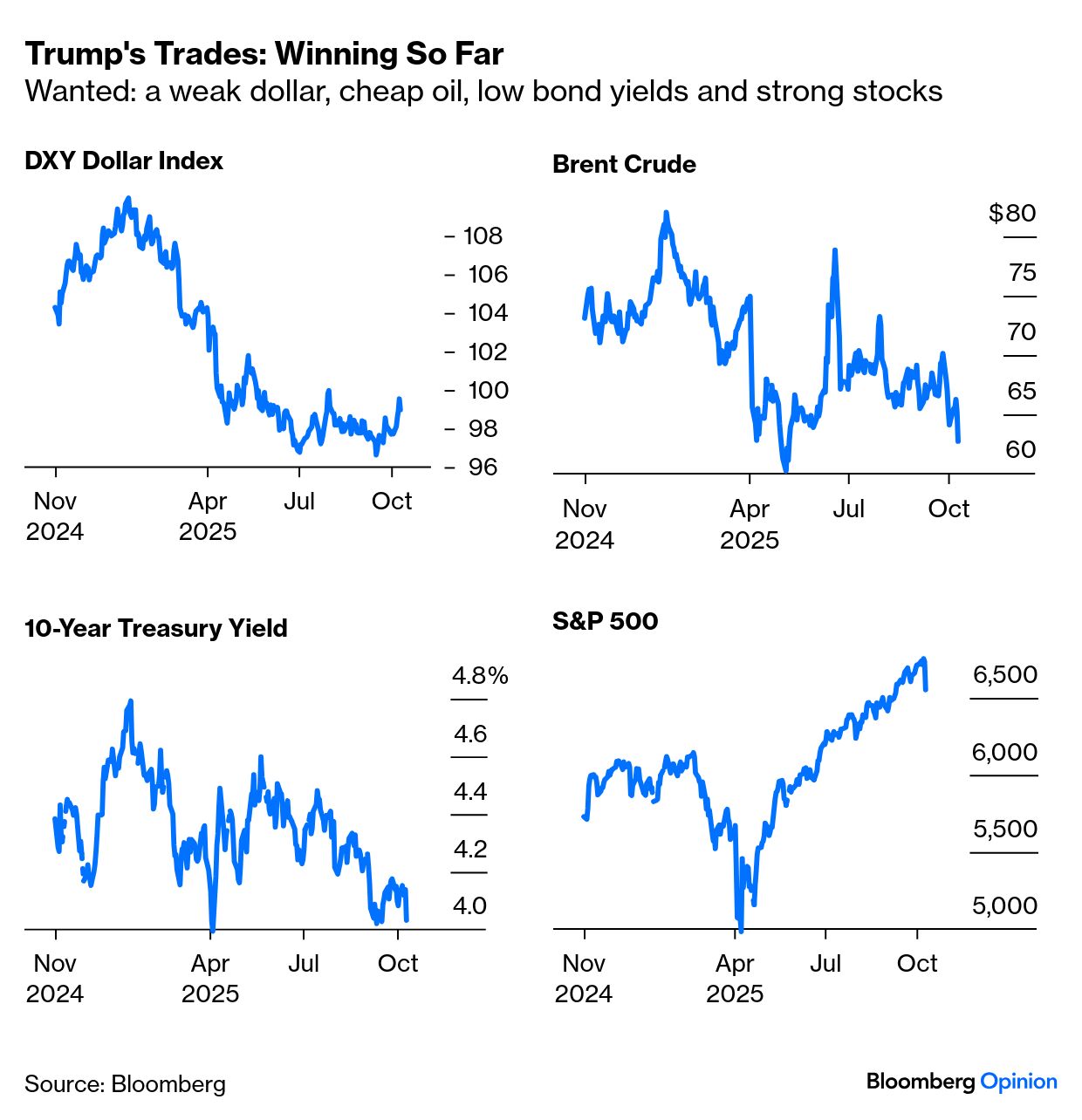

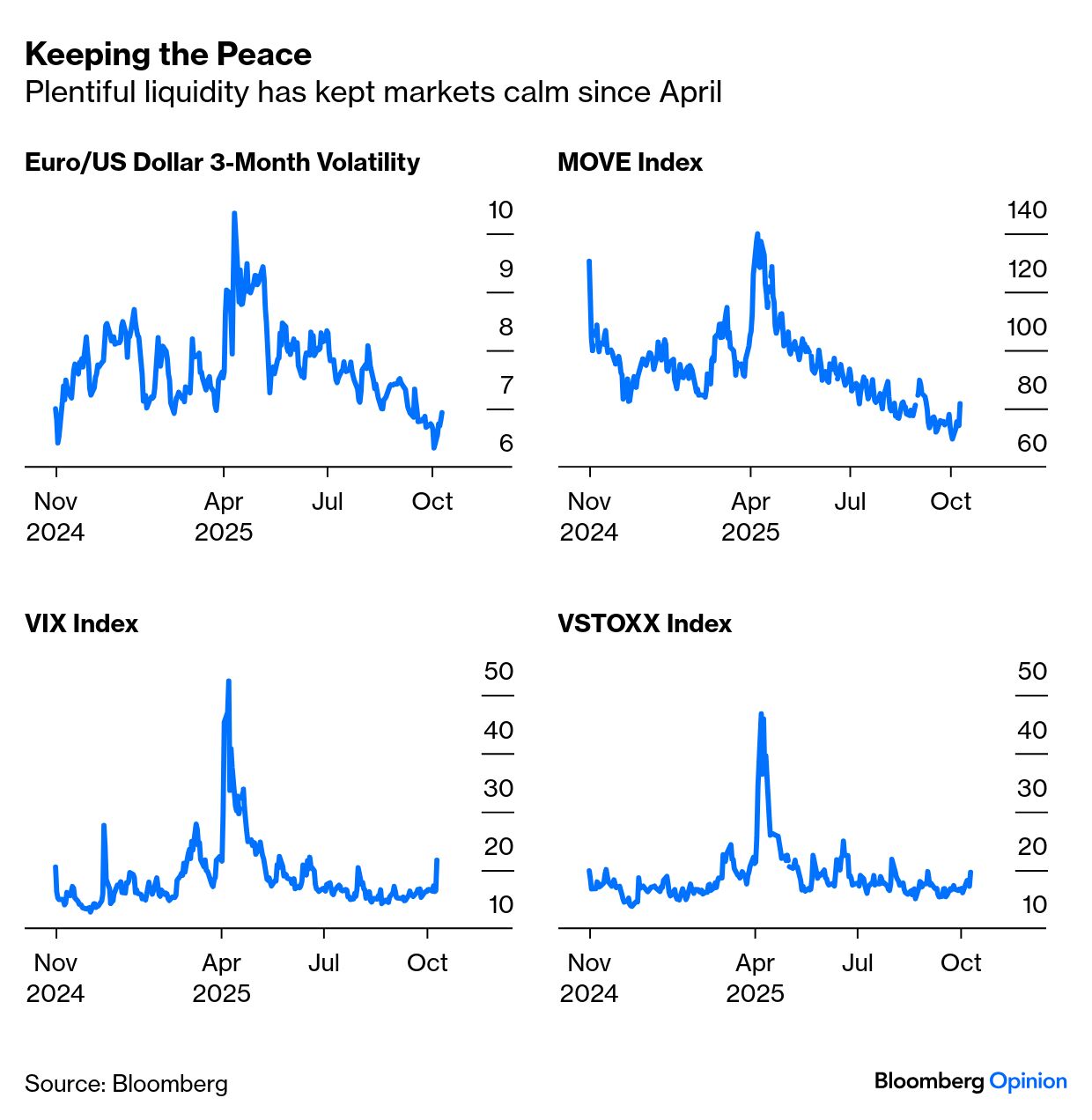

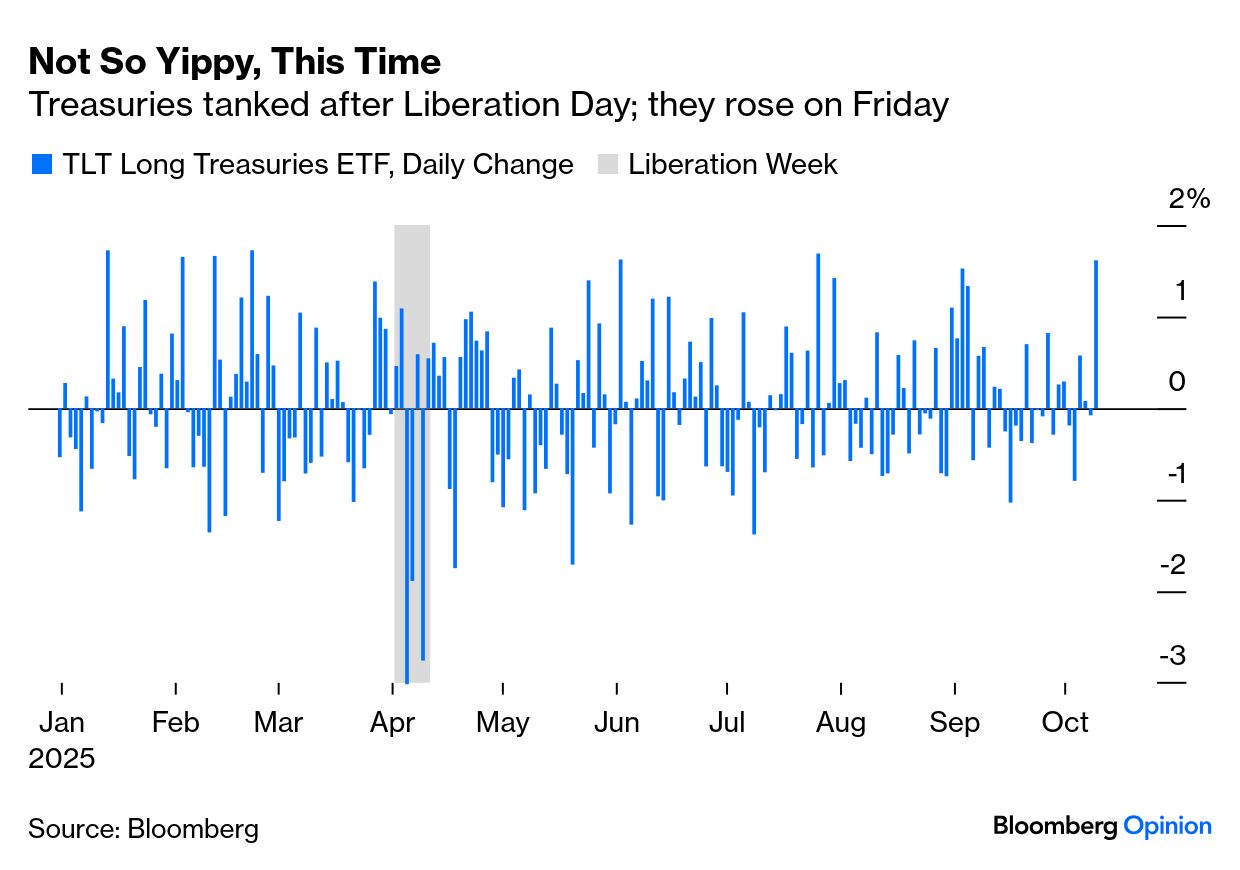

Once the administration said that tariffs on all nations but China would be paused for 90 days, the market enjoyed one of the biggest swings in history. A subsequent ceasefire with China, and acknowledgement from Trump that he wouldn’t fire Powell, combined with a return to boosterish White House pronouncements about the stock market to ram home the notion that Trump always chickened out. By the end of July, taking the relative performance of stocks and bonds as a gauge, all the lost ground from Liberation Day had been made up. Market performance since the end of July has been more of a question mark. The Liberation Day tariffs ended up being applied with close to the full force that was originally announced. “Deals” with the UK, the EU, Japan and others were vague and resolved nothing; countries as significant as Brazil and India faced even higher levies than first announced. Trump tried to fire the Fed Governor Lisa Cook as central bank independence remained very much up for grabs. But the rally continued until Friday’s correction. This could be the moment when the Trump trade takes a new direction — or it could prove to be a correction to speculation. A healthy start for stock futures on Monday Asian trading leaves both interpretations open. This is how the Trump trades have played out, mapped by the relative performance of the S&P 500 and 20-year+ Treasuries (the SPY and TLT exchange-traded funds): Were markets really working on the assumption that the trade issue was resolved? Is Mr. Market that naive? There certainly seems to be some naivete going on. That said, the administration has done much to get its ducks in a row in a way that they weren’t six months ago. Treasury Secretary Scott Bessent has aimed for lower bond yields, a cheaper dollar, cheap oil and strong stocks. Between them, they keep the economy juicing nicely, aid competitiveness and minimize the experience of inflation. And he’s getting all of them (even after the selloff). Indeed, Friday’s big drop in the oil price even helped: Meanwhile, the provision of abundant liquidity (even if the Fed keeps overnight rates too high for the administration’s taste) has put market volatility to sleep, in stocks, bonds, and currency. This helps, a lot: And one dog didn’t bark on Friday. Trump admitted that the April tariff climbdown was driven by “yippy” bond markets. The way bonds sold off after Liberation Day was a classic sign of lost confidence in the US as a jurisdiction, as often suffered by emerging markets. This time, investors seem to have treated bonds as a haven once more; they had a strong gain on Friday: Markets’ confidence wasn’t as great as it appeared. But its foundations remain intact for now. Whether this situation escalates will depend on the two sides’ motivations. |