Points of Return

| To get John Authers’ newsletter delivered directly to your inbox, sign up here. The biggest question over this week’s FOMC: Who exactly woul | | | | | | To get John Authers’ newsletter delivered directly to your inbox, sign up here. | | | | | | | | | This week’s Federal Open Market Committee meeting, which starts Tuesday, had an element of suspense like few others in history. With only hours to go, there was genuine uncertainty over who would vote. This drama was never going to have more than a minimal impact on the outcome — but the longer term implications are profound. Seven Federal Reserve governors have a vote on interest rates, along with five of the eight regional bank presidents, who serve in rotation. Late Monday, the Senate rushed to confirm Stephen Miran’s appointment to fill a vacancy, so he will take part. Meanwhile, the administration tried to persuade an appeals court that it could fire Lisa Cook, a governor whose term has more than a decade to run, in time to prevent her from voting. On Monday night, the court ruled that she could vote. There was never any chance to replace her before the meeting, but the administration evidently cares passionately about each vote. This is not because of the outcome on Wednesday. The Fed will decide whether to cut rates, probably by 25 basis points. It’s possible they will opt for a “jumbo” 50 basis points, but the futures market, as gauged by Bloomberg’s World Interest Rate Probabilities function, gives that only a 5% chance. The big shifts in the odds have come in response to data, which could move the majority of the committee, not the legislative maneuvers around Miran, or the legal proceedings against Cook. Only if there are five FOMC voters (other than Miran and Cook) already prepared to back a jumbo easing could it make a difference. And as central bankers tend to be conservative types (with a small c), they were highly unlikely to be comfortable with a big decision like this being made by a 6-5 vote after the administration had engineered two changes to the committee hours earlier. A jumbo cut might just happen — but subtracting Cook would on balance have made it less likely. A further oddity is that while Cook’s politics are plainly well to the left of President Donald Trump, there’s no direct readthrough to her views on interest rates. She has written extolling the virtues of adding full employment to the Fed’s mandate, which political liberals are often comfortable prioritizing over inflation — that would mean a readiness to make big rate cuts. All of this helps to explain why markets have not so far treated the Miran and Cook issues as terribly relevant; they don’t affect the near-term outcome, while few expect the courts to allow Cook to be fired without a full airing of the charges of mortgage fraud leveled against her. It would be unwise to expect it to stay this way. First, Miran’s arrival, after he insulted the current members by saying they suffer from Tariff Derangement Syndrome, will be provocative to say the least. Last year, he published a paper on the Fed suggesting that the White House appoint the seven governors, while also having the right to dismiss an expanded list of 12 regional presidents at will. In the very short term, he can be expected to dissent in favor of cutting rates by more than the majority on the FOMC decides, and may express himself vocally. The situation grows more charged. But this is only the first step in a five-step plan that would allow the administration to “pack” the FOMC to follow its wishes, without passing legislation through Congress. Will Denyer, chief US economist of Gavekal Research, lays it out as follows: - Get the US Senate to confirm Miran (which has now been done);

- Get a court to uphold the firing of Cook, and do so by February (which could be much tougher, given the Supreme Court went out of its way in an opinion earlier this year to say that the president didn’t have the same freedom to fire Fed officials that he did with other government agencies);

- Get the Senate to confirm Cook’s replacement (which should be easy);

- With Governors Michelle Bowman, Christopher Waller, Miran and Cook’s replacement now forming a majority of the seven Fed governors, get them to block any nominations to the Fed’s eight regional presidencies, which need to be approved by the end of February (this is where the urgency to fire Cook comes from); and

- Get the governors and presidents now on the FOMC to vote as Trump wishes.

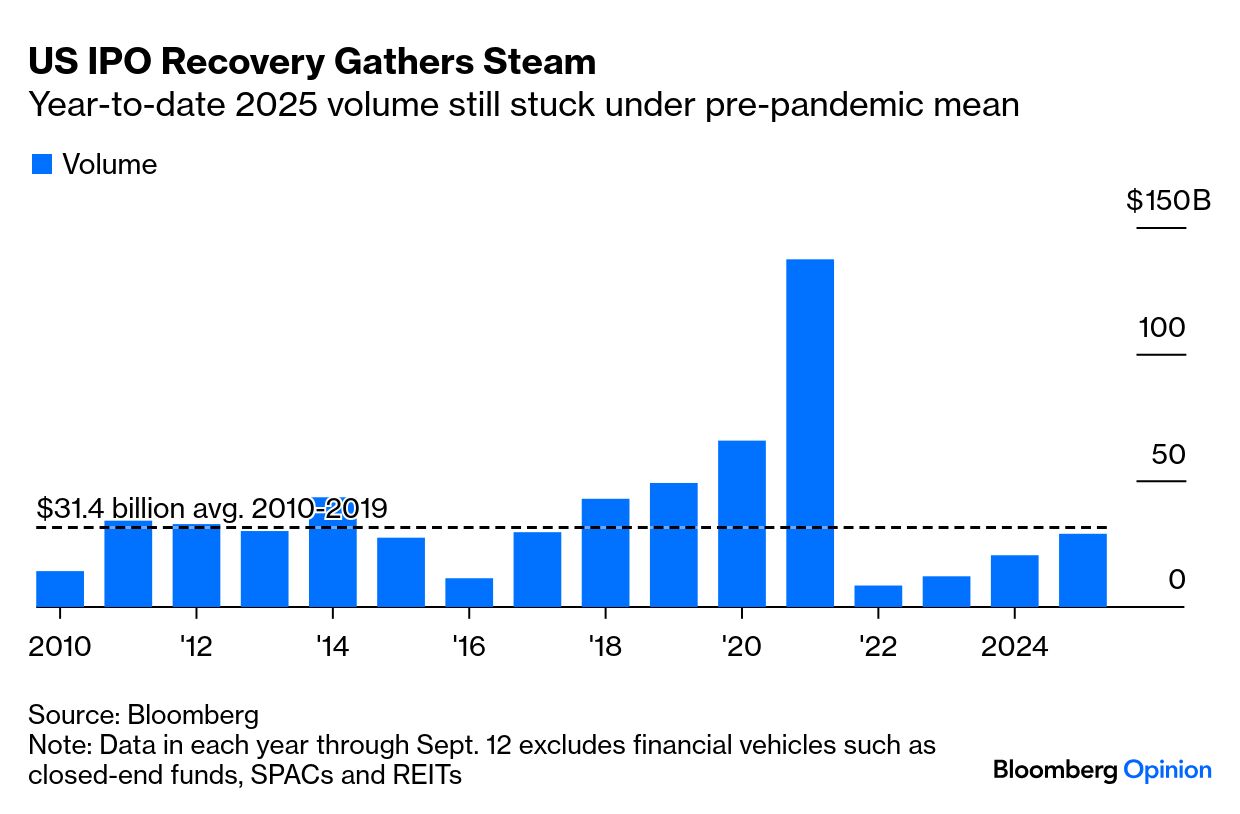

It’s fair to say that 4. would follow from 2. The critical steps are to get Cook fired, which will be a fascinating test for the Supreme Court, and then to appoint a new FOMC that will follow Trump’s instructions by making it a priority to minimize the rates the government pays to service its debt. That could be a problem, as attested by the long history of Supreme Court nominees who don’t turn out the way the presidents who nominated them had hoped. These will be intelligent people for whom a seat on the FOMC is the pinnacle of their career. Thus it’s still on balance unlikely that these machinations will end with a Fed prepared to go along with fiscal dominance and financial repression to keep rates low. That’s why the market isn’t too fussed about it. It would change if the Supreme Court decides Cook can be fired. And legal experts think that’s growing more likely. Law professor and Bloomberg Opinion colleague Stephen L. Carter writes: “As recently as last month, I’d have estimated about a 5% chance that the Supreme Court would allow Trump to fire Fed governors; today I’d say the odds are closer to one out of three.” | | | | | If there were any lingering doubts about renewed momentum in initial public offering (IPO) activity and dealmaking, Klarna Group Plc’s debut last week extinguished them. It’s starting to feel a lot like 2021 again, when zero interest rates and stimulus checks delivered a fleeting but powerful boost to companies riding the risk-on wave. Recent market debuts, such as Circle Internet Group Inc., CoreWeave Inc., and Figma Inc., much like the Zooms and Pelotons of the last cycle, are enjoying strong early momentum. That shows revived investor appetite even at stretched valuations by historical standards. First-time share sales on US exchanges have raised $28.9 billion this year, excluding closed-end funds and other financial vehicles. As the chart below shows, while the haul is nowhere near the records set in the Covid era, it is still 42% ahead of last year’s pace, according to data compiled by Bloomberg: What explains the recent surge? Phil Haslett of Equityzen Securities explains that stable geopolitical conditions compared to prior years are often the catalyst that pushes companies to finally go public. The challenge now is that so many firms have been waiting since 2021–2022 that there is likely to be a bit of a rush: Investors will be watching closely to see whether these companies have the right metrics and whether there’s enough capital to support them all. The timing feels right, especially as we move past summer, but while rate cuts should provide another catalyst, I’d argue they’re already largely priced in.

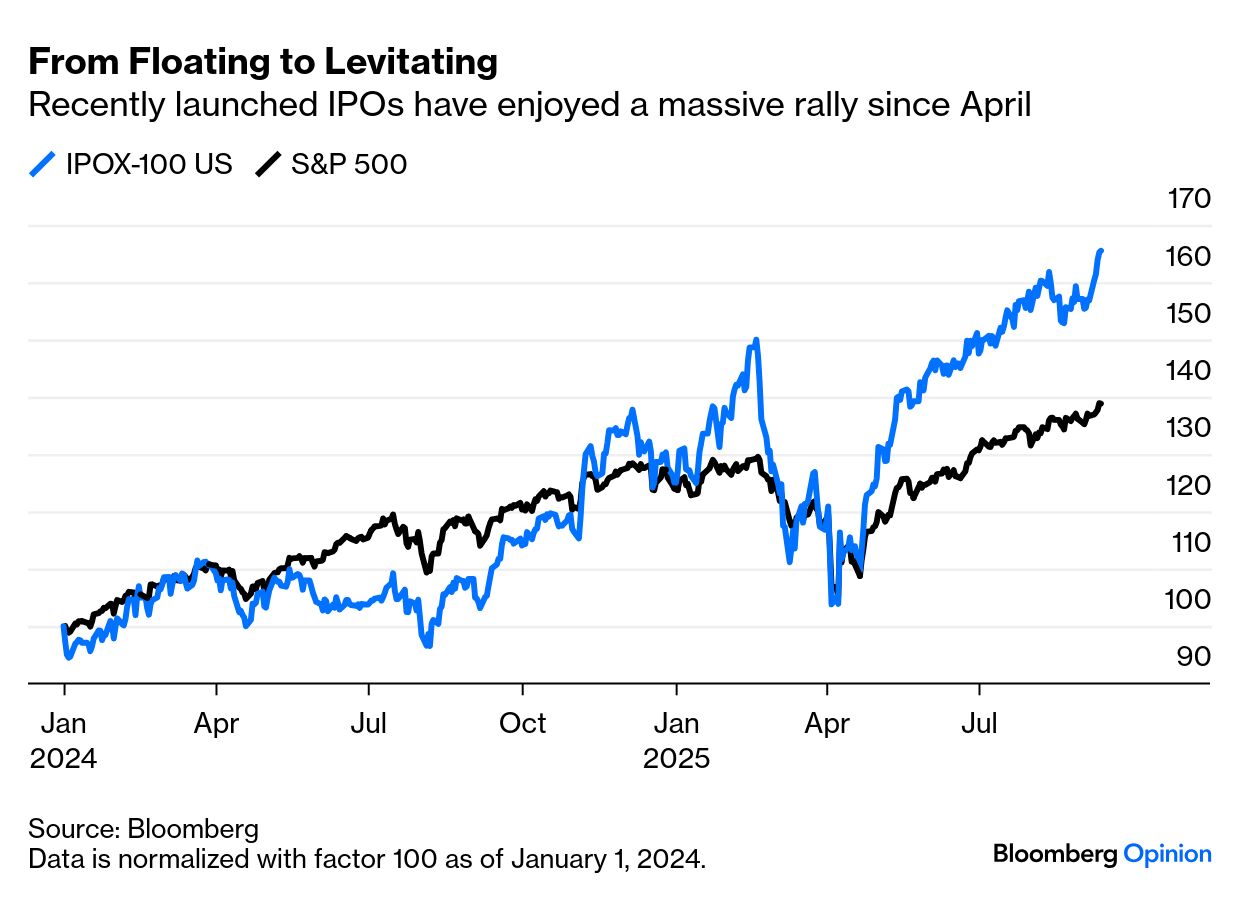

It’s not clear how durable the momentum will be. Unanswered questions surrounding the pace and magnitude of Fed rate cuts, global trade tensions, and ongoing geopolitical instability, particularly in the Middle East, all complicate valuations, Kyle Stanford of PitchBook notes. That is not ideal in a market where down-round IPOs, where a company’s valuation decreases from previous estimates, have already become the norm — nearly every high-ticket public listing year-to-date has priced well below its peak private round. For example, Klarna topped at over $40 billion during the pandemic, but made its public debut at less than half that figure. Stanford says that such reduced prices make going public untenable. However, as market uncertainty begins to ease and conditions improve, the gap between private and public assessments is starting to narrow. “This year, IPO valuations have been just 25% above a company’s highest private market value at the median. In 2021, that median was 126%,” he says. For those buying the stock, rather than selling it, the last few months have been a bonanza. The IPOX-100 index of recently floated shares has massively outperformed during the post-“Liberation Day” rally, which is testament to strong animal spirits, and likely encourages more companies to go public: With as much as 130 basis points in Fed rate cuts priced over the next year, MI2 Partners argues that looser financial conditions are likely to bolster the case for going public. The strength of the IPO market does, however, in itself argue against the need for monetary easing: This is not our first time around the block, and we assure you that the reopening of the IPO window is not usually considered a symptom of tight financial conditions. Perhaps we are a bit old-fashioned in thinking that this is even more true for IPOs of blockchain fintechs, crypto brokers and “buy-now-pay-later” consumer microlenders.

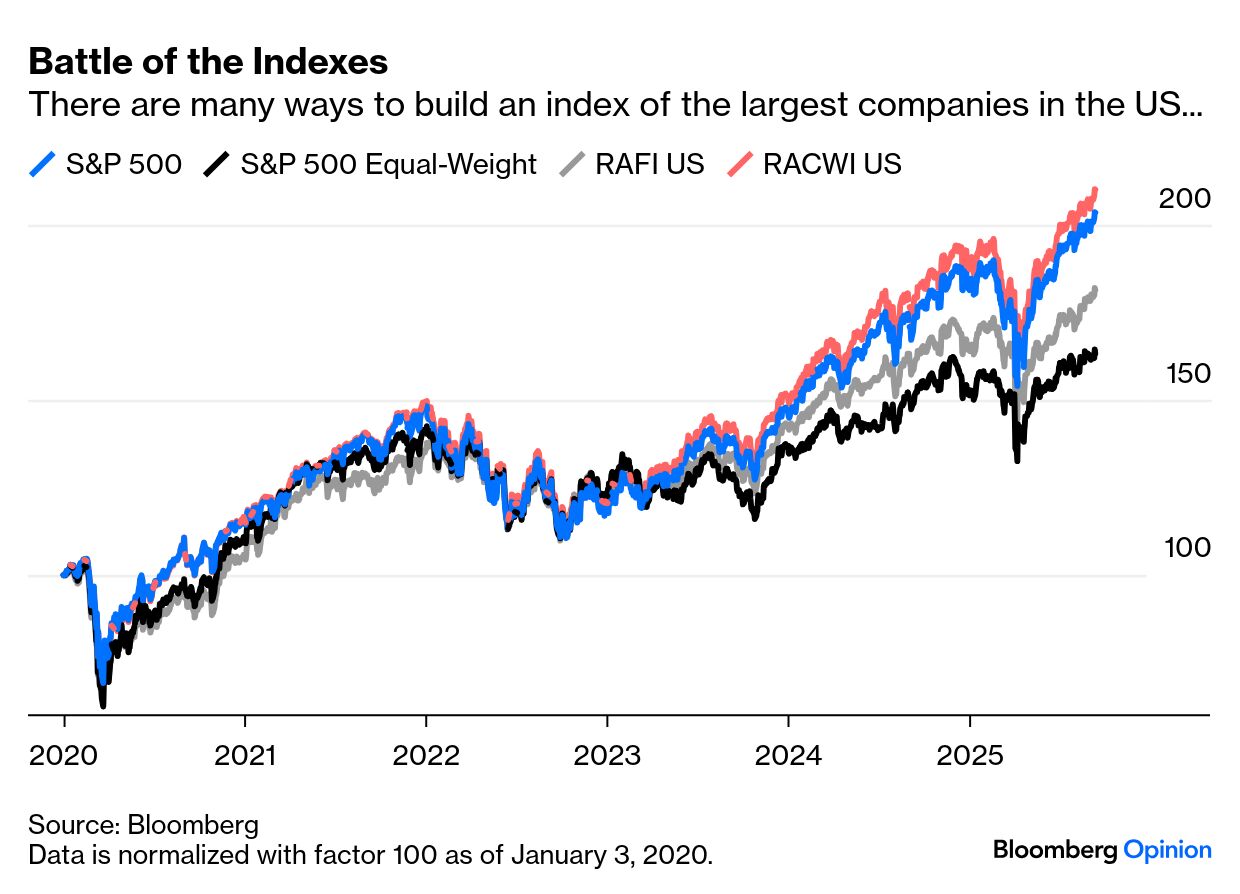

Beyond Klarna, last week’s deals involved the blockchain lender Figure Technology Solutions Inc. and Gemini Space Station Inc., the crypto custodian and broker founded by the Winklevoss twins. That underscored the tailwind for unicorns operating in sectors closely aligned with the Trump agenda. At present, Stanford notes that companies in AI, crypto and fintech enjoy a rare combination of regulatory support, targeted federal investment and market enthusiasm. We can expect plenty more companies in those sectors to IPO while the going is good. — Richard Abbey | | | | | Points of Return is coming from Hong Kong this week, as I will be taking part in a special live edition of the China Show on Thursday. Subscribers are invited to our Hong Kong bureau for a discussion of Trump, China and what investors can expect next. Is there more volatility ahead? Please join us if you’re in Hong Kong, and ask me and Bloomberg Opinion colleague Shuli Ren your questions. Register here. I need to correct one of the charts from yesterday’s note on indexing and alternatives to the market cap-weighted S&P 500. It showed the RAFI US Small-Cap index, not the RAFI US index, for larger cap stocks, which is the more relevant comparison. This is the corrected version: The arguments in the piece are unaffected. I apologize for the error. | | | | | Following on from that, maybe one relevant tip is that jet lag can be bad for your accuracy. My presence 12 time zones from home and the need to make a correction are connected. I made that mistake by adding one extra S to Bloomberg ticker — the kind of dumb error which is easier to avoid if you’ve had a good night’s sleep. Hints on dealing with jet lag gratefully accepted. Meanwhile, sensitive suggestions for listening in the small hours of the morning include: Insomnia by Faithless, Nessun Dorma (Nobody Will Sleep) from Puccini’s Turandot, and U2’s Bad (chorus: “I’m wide awake and I’m not sleeping.”) Any more? More From Bloomberg Opinion: - Aaron Brown: This Gold Rush Isn’t About Inflation — or Even Gold

- Matthew Winkler: Poland’s Economy Defies Putin’s Threats and Keeps Growing

- Chris Bryant: Germany’s Autobahn Bridges Are Going to Pieces

| | | | | You received this message because you are subscribed to Bloomberg's Points of Return newsletter. If a friend forwarded you this message, sign up here to get it in your inbox. | | | |