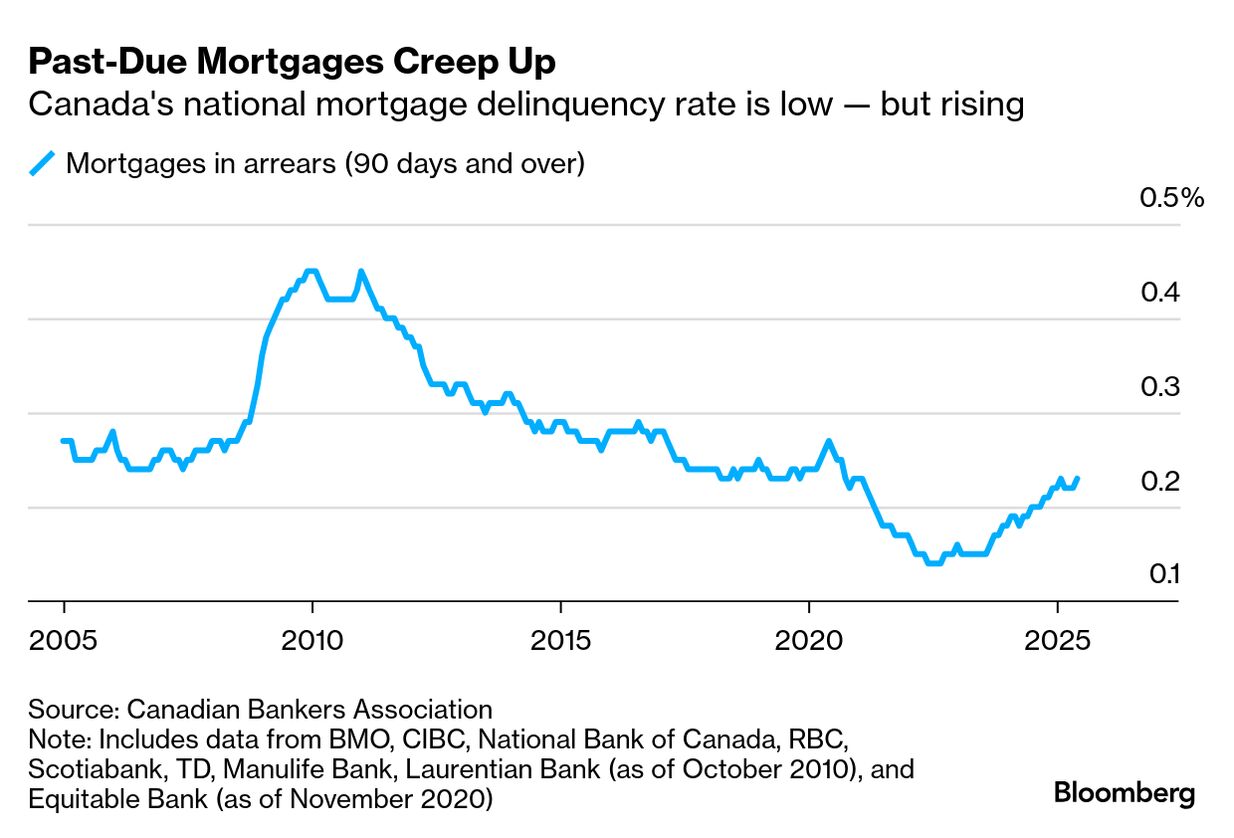

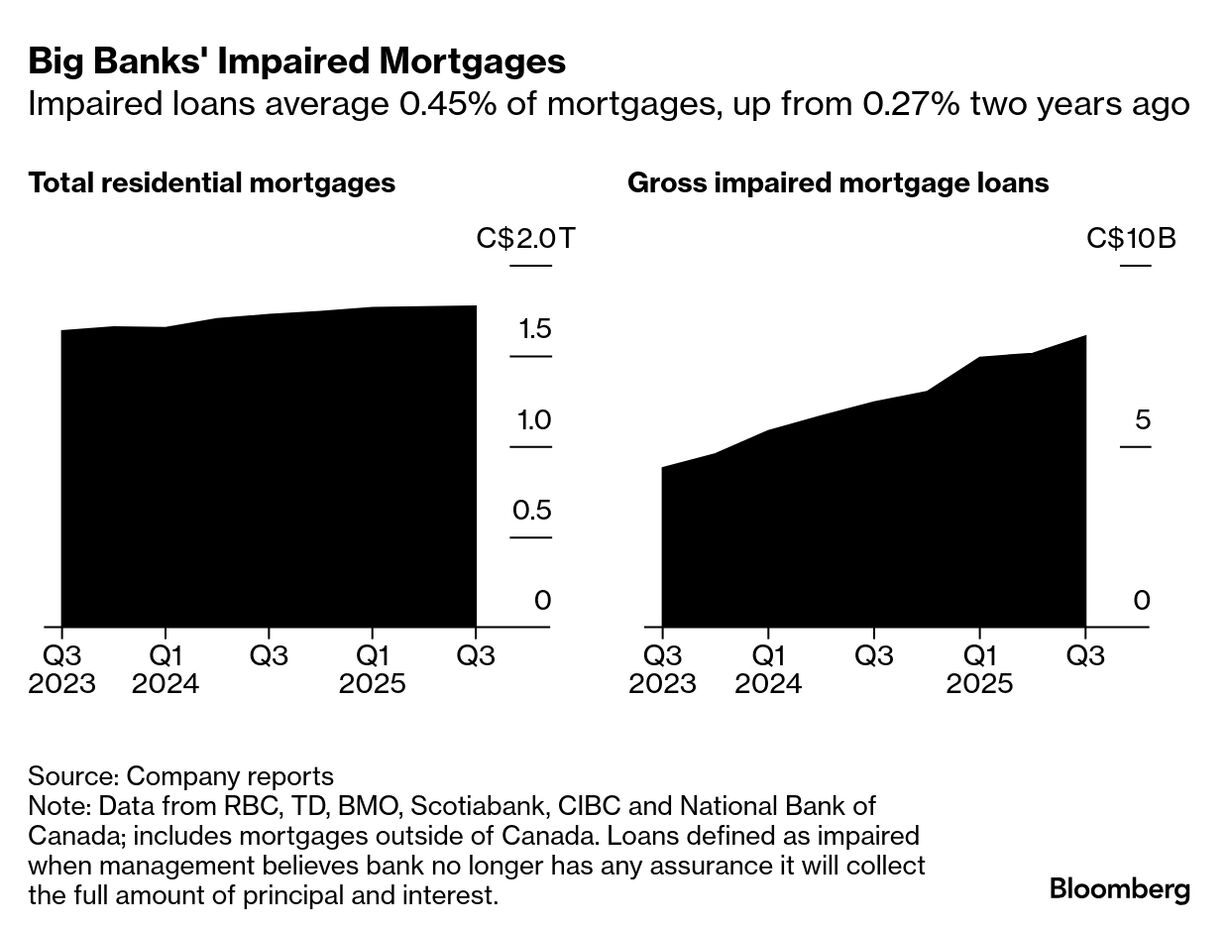

| Bankers love a metaphor, even a vaguely disturbing one. “We’re starting to see the pig moving through the python,” Phil Thomas, Bank of Nova Scotia’s chief risk officer, told analysts last week. He was talking about the bank’s credit book, particularly its auto loans, which gave Scotia some problems over the past few years. The pig — loans to troubled borrowers — was about “halfway or maybe more through that python now.” Canada’s big banks set aside less money for bad loans in the fiscal third quarter than they did earlier in the year and we’re starting to hear more talk of reaching the peak of the credit cycle. The lenders are slowly but steadily digesting all that distress — bones and all. I’d just gotten the image out of my mind when Scotiabank’s chief executive officer brought it up again. “As Phil said, the pig in the python is coming through,” Scott Thomson said at a financial conference on Wednesday. “We are going to see that improvement continue. I think our Canadian clients are still under stress, but they’re managing effectively.” And what about real estate loans? “I’m not really worried about the mortgage book.” It’s true that delinquencies and loan losses on mortgages don’t appear high enough to cause Canada’s big banks any serious trouble. But they’re rising, and it’s easy to spot signs of the stress hitting parts of the market.

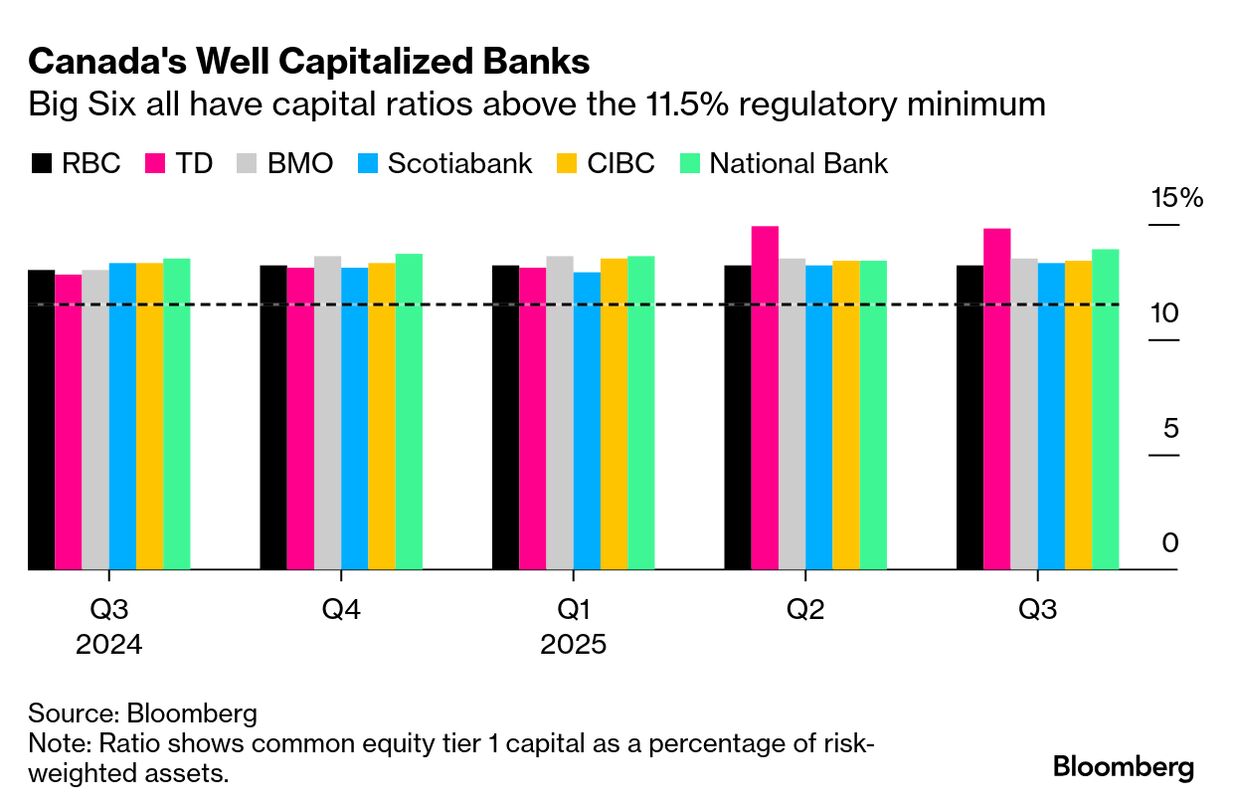

Home sales are depressed and prices have fallen. The benchmark price of a home in Toronto declined again in August, dropping 0.1% from the previous month to C$978,100 ($707,000) — and it’s now 22% below its peak. That’s causing trouble for some real-estate focused lenders. At EQB Inc., impaired loans were up by 5% in the third quarter, with almost all of the increase coming from the mortgage-heavy personal lending portfolio. The firm lends to underserved demographics such as self-employed people and new Canadians. EQB is seeing particular stress in Toronto’s suburbs, where rising unemployment, elevated interest rates and declining home prices are combining to cause pressure. “There were some pockets where we did see prices drop 25% to 30%,” EQB Chief Risk Officer Marlene Lenarduzzi told analysts on an earnings call. Some people are struggling to sell their homes. About 25% of sellers are pulling properties off the market after not getting the price they’d hoped for, according to Peter Routledge, Canada’s superintendent of financial institutions. The fact that they can delist their properties and continue to make their monthly mortgage payments is a good sign, Routledge said at the Scotia conference. Still, he’s tracking the strains in the condo market, which has left many developers sitting on unsold units and facing financial distress. “We are concerned about it, particularly in our larger cities, Toronto being the most prominent one. Vancouver is also one where we’re watching closely,” Routledge said. The regulator “is paid to worry about the downside and prepare for it. And I’m not predicting that the downside's going to arrive, but we worry about it all the time.” On balance, there’s ample capital in the system to absorb some of the shock if there is a more serious housing downturn, making it a “manageable situation for households and financial institutions,” he said. As for the “payment shock” homeowners have been bracing for as their mortgages renew at higher rates, the banks aren’t too worried. TD Cowen analyst Mario Mendonca estimates that the average payment increase across clients of the Big Six banks, excluding TD, will be just C$158 a month. But Mendonca warned the situation might appear more benign than it actually is. The average monthly increase is skewed downward by borrowers who took out shorter-term mortgages after rates jumped. But those who signed onto fixed-rate mortgages in 2021 or 2022, when rates were significantly lower, will face much bigger bills, he said in a note to investors. TD estimates there are C$118 billion worth of uninsured, fixed-rate, five-year mortgages issued at an average interest rate of 2.2% in 2021 that are set to be renewed next year. In June of this year, similar mortgages were originated or renewed at 4.3% — basically double. “While we continue to believe mortgages will not drive material charges for Canada’s largest banks, the payment shock for certain borrowers is not trivial,” Mendonca said. At greatest risk, perhaps, are homeowners who are heavily in debt but losing their source of income. Friday’s labor force report was grim reading — the second straight month of big job losses and the highest unemployment rate in four years. In the Toronto region, that rate is around 9%. The banks are fine, but for some people, that pig’s got a long way to go. |