“Overall, strength in company fundamentals, such as high cash balances, can provide investors with a feeling of safety during difficult economic periods.”

That’s how Segal Macro Advisors described the biggest technology companies in 2023 — that’s when the Magnificent Seven title was conceived to describe the largest and fastest growing US technology companies. The appeal of safety — typically reserved for AAA-rated bonds — isn’t usually cited for high-growth stocks. Segal’s analysis was framed as a question: “Is Mega-Cap Tech a Safe Haven or a Bubble?,” ultimately concluding that big tech would be a port of safety when the seas turned rough. I looked at the numbers and found that since the pandemic that’s mostly true for five of the Magnificent Seven technology companies, Alphabet Inc., Amazon Inc., Apple Inc., Meta Platforms Inc. and Microsoft Corp. Alphabet, for example, has delivered a return on common equity between 20% and 35% for each and every of 18 quarters since 2021. It makes sense. These companies offer almost utility-like functions in the tech-centric world we live in — so much so they have drawn antitrust concerns. Alphabet via Google search, Amazon via shopping and Internet infrastructure, Microsoft via the cloud and business productivity, Meta for its dominance in social networks and Apple’s for its ubiquitous iPhones. But what does Tesla do that we all depend on? Right now, it just makes high-end vehicles. Its dispensability shows in its eroding return on equity as electric vehicle competition has increased. That’s down every single consecutive quarter from 28% in the fourth quarter of 2023 to a measly 8% in the past quarter. As for Nvidia, for sure they make the chips powering a revolution in generative artificial intelligence. This potential shows up in returns on common equity of over 100% for six quarters in a row. But for all the capital investment, Generative AI has famously yet to yield a ‘killer app’ everyone is willing to pay for. It does suggest that when the storm does come, the five utility-like companies will provide a cushion compared with the risk rewards in Tesla and Nvidia’s valuations. Nvidia carries more promise — and risk | Nvidia is meeting the current moment like no other given its $4 trillion size. Revenue is up by a multiple of six times since ChatGPT was released in November 2022, setting off an enormous investment cycle in GenAI. The company looked incredibly expensive in July 2023 trading in excess of 200 times earnings. It has since grown into that price while still delivering a 10-fold increase in share price for shareholders. Still, the upside revenue surprise this past quarter of 1.1% was the smallest consensus beat since January 2023, the quarter that captured ChatGPT’s debut. Brook Selassie, a Vice President in technology consultant Gartner's Business Growth Strategies team told me: “GenAI has passed its hype peak, with failures, cutbacks, and superficial “checkbox” deployments pushing it toward the Trough of Disillusionment by 2026; fewer than one in five projects will realize business value.”

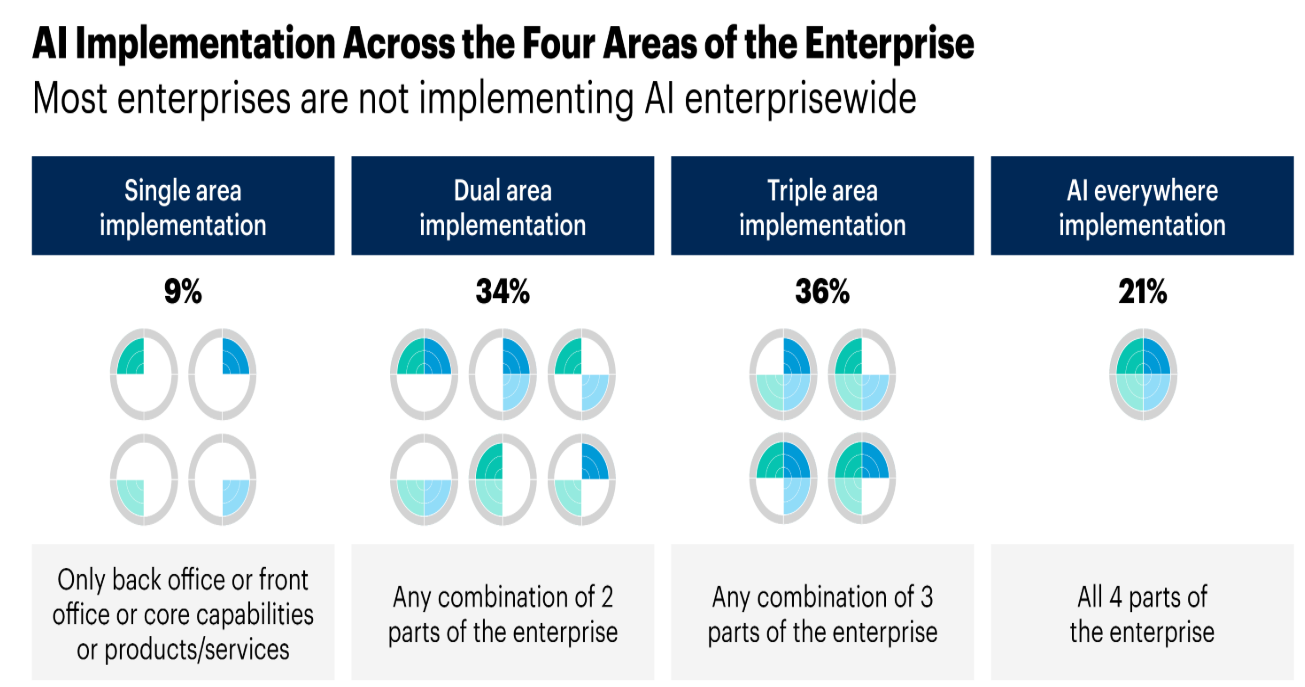

Most enterprises remain confined to narrow productivity gains—often barely measurable— with less than 30% of initiatives pursued by the top 8 industries being disruptive, enterprise-level projects, Selassie said. MIT found that 95% of AI pilots failed to yield any discernible results. So, while the big tech companies have promised to keep spending on artificial intelligence, the slowdown in the pace of that spend is already evident. And many other companies outside of big tech are highly skeptical about what AI will deliver for the bottom line. Sam Altman, the leader of the company that makes ChatGPT, has even used the term ‘bubble’ to describe what’s happening now. While AI spending is still growing rapidly, much of this growth is coming from just a handful of tech giants. AI hyperscalers including Microsoft., Meta, Amazon and Alphabet now comprise a record 31% of the total capex spend of firms in the S&P 500 Index, according to data compiled by Strategas Asset Management, LLC’s Ryan Grabinski. By comparison, that figure stood at 19% at the end of 2019. |