|

|

|

|

|

|

|

|

|

Pamela Francis, an administrative assistant at UBC, turned her love for travel into a part-time gig as a vacation consultant, something she plans to continue after retiring from her day job. Jennifer Gauthier/The Globe and Mail

|

|

|

|

|

Good morning. As many of you’d guess (or are already experiencing), retirement is much more than just palm trees, golf and gardening. In a new, recurring instalment here at Retire Rich, we’re talking to Canadians to find out what their “second acts” are, and hopefully it’ll help inspire you. Let’s get into it. |

|

|

|

|

When a passion for travel becomes a retirement plan |

|

|

|

|

Meet Pamela Francis, 56, a university administrative assistant in Vancouver who’s mapping out her transition to semi-retirement and doing it on her own terms. |

|

|

|

|

Back in her 30s, Francis earned a master’s degree in art history in Britain. That experience sparked a love for travel that’s stuck with her ever since. |

|

|

|

|

In 2019, she turned her passion into profit, starting a part-time gig as a vacation consultant for Expedia Cruises. Now, she spends evenings and weekends booking dream getaways for clients and earning commissions while doing it. |

|

|

|

|

Her big plan? To retire from her day job within five years and continue to work as a travel consultant part-time. She plans on using her earnings to help supplement her retirement income, along with her pension from her job and her own personal savings. |

|

|

|

|

“I want my brain to be engaged,” she said. “Helping people plan their perfect trip keeps me energized and excited. The travel perks are a sweet bonus.” |

|

|

|

|

Her advice to folks gearing up for retirement is to find something you genuinely love to work on: “It should be something that feels easy because it lights you up,” Francis said. |

|

|

|

|

She is not alone, of course. Many Canadians use their retirement as a launchpad to try out new skills and interests, mixing additional income with personal fulfillment. |

|

|

|

|

Got a Second Act story of your own? Whether you’re dreaming, planning, or already living it, drop me a line at mraman@globeandmail.com. I’d love to hear it. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

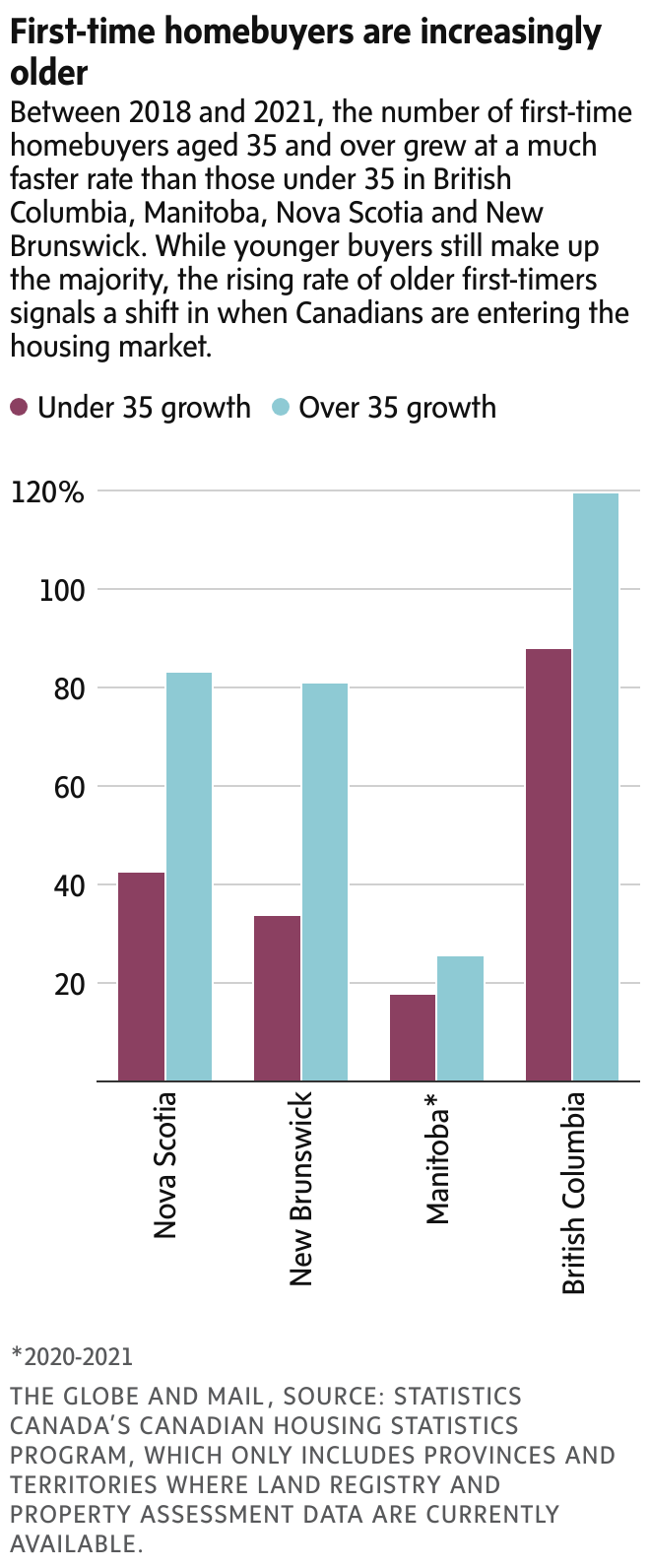

First-time homebuyers are getting older. Between 2018 and 2021, the number of first-time homebuyers aged 35 and over grew at a much faster rate than those under 35 in British Columbia, Manitoba, Nova Scotia and New Brunswick. |

|

|

|

|

Why? Homes prices have soared. The average Canadian home now goes for just under $700,000, nearly four times what it was back in 2000. But annual individual incomes haven’t kept pace, creeping up only about $10,000 since then, up to $59,400. |

|

|

|

|

Why it matters: Younger Canadians are hitting pause on home buying, choosing instead to spend their 20s and 30s travelling, learning and living on their own terms, before settling down in their 40s or later. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Craig, 64, and Sharon, 62, have a net worth of $3.5-million with no debt. Can they retire next year and sustain their current lifestyle? Ashley Fraser/The Globe and Mail

|

|

|

|

|

|

|

|

|

|

|

That’s the question Sharon, 62 and Craig, 64, are asking. Let’s break it down. |

|

|

|

|

The numbers: In 2018, when the couple was first featured in The Globe,

their net worth was $1.7-million. After years of saving, they’ve now grown it to $3.5-million with no debt and have a retirement spending goal of $90,000 a year after tax. Sharon earns $110,000 a year, while Craig is semi-retired and collecting a $30,000-a-year defined benefit pension. Craig recently inherited $830,000, which they used to top up TFSAs and help their two kids with down payments. |

|

|

|

|

The situation: They’re wondering if Sharon can retire in January, if Craig should defer his Quebec Pension Plan and whether they should buy a house in town to move into when they’re older. |

|

|

|

|

The good news: A financial planner says they’re in great shape. Sharon can afford to retire next year, with a few strategic moves. |

|

|

|

|

Key steps, from a financial planner: |

|

|

|

|

- Start drawing down their registered retirement savings plans/registered retirement income funds early in retirement while their taxable income is low, to manage taxes and avoid Old Age Security clawbacks.

- Defer QPP and OAS to age 70 if they’re healthy.

- Their portfolio is 100-per-cent stocks, too risky at their age given they’ll be drawing down assets. All-in-one exchange-traded funds could be a better, lower-cost option.

- Buying a house in town could work. If they rent it out, it would be cash-flow neutral. Moving in later might trigger capital gains, but tax deferral options exist.

-

Plan for the family cottage. To avoid estate tax issues and family disputes, they should discuss succession plans with their kids now.

|

|

|

|

|

|

|

|

|

|

|

|

|