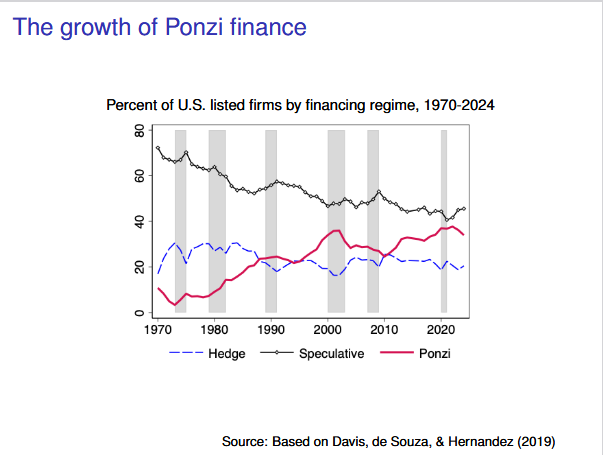

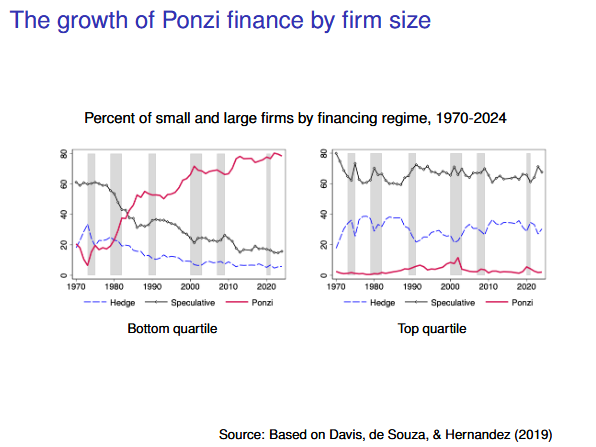

| In another one of Dr. Davis’ slides, you can see that Ponzi financing remains rare among big firms, but in the bottom quartile of public companies, there’s been a dramatic rise in those that can’t finance their operations out of cash flow. In the Minsky framework, a company is considered to have hedge financing if expected cash flows exceed interest and principal payments. They’re speculative when they need to roll over principal payments. Ponzi is when you can’t fund your business without an influx of new money. SpaceX is an example of a business considered successful that is operating in Ponzi. It’s now raising money to fund operations at a valuation of $400 billion. It’s hard to fight the received wisdom — that Trump won’t follow through on his threats because he’s afraid of the consequences — when that thinking has recently driven US equity markets to record highs. Still, it’s disconcerting. I mean, even if you can rule out worst-case scenarios, the economy can still get wrecked by the drip-drip of threats and the uncertainty of it all. After all, copper prices rose the most since 2008 on the 50% tariff news. That price increase gets passed through to all manner of manufactured products. If that constant uncertainty and whipsawing of prices finally brings the US economy to a standstill, there’s a non-zero risk — I’d call it substantial — that investors’ willingness to fund firms with operating budgets that exceed cash flow would diminish swiftly and substantially. It’s not that the Silicon Valley model is going away. It’s wildly successful. And Dr. Davis’ research shows this isn’t just a tech play. She says Ponzi structures have grown across sectors of the US economy in response to that success. Still, to the degree investors husband their cash more tightly due to a downturn in growth, you will get a knock-on effect that hurts small listed companies. The majority of them can’t fund operations from cash flow and will, thus, be forced to cut capital investment and lay off staff. Knock-on effects a la the 2000s | What does that mean for big firms and the economy? My view is that it’s akin to what we saw when the Internet bubble popped. Many a small internet companies and upstart telecom businesses went bust. The accompanying wave of job losses and the evaporation of capital investment helped tip the US economy into a recession. It also reduced earnings multiples for publicly-traded companies large and small. The double whammy of lower profits and lower profit multiples meant excruciating losses. Many of these companies would have been viable without the withdrawal of funding. Internet startup Webvan crashed and burned in that downturn despite the fact that versions of its business model have proven wildly successful for Walmart, Instacart and Amazon. It’s just that, when the cash flow stops, you have to be able to fund yourself from operations or go out of business. Between 2001 and 2010, the percentage of small businesses with negative operating cash flow declined. The percentage was still high, but it fell as investors became more discerning. That’s the risk this time as well. ------- One housekeeping note. Until this year I hadn’t been active on social media for a long time. But I now post often on Bluesky. Follow me there at @edwardnh.bsky.social. |