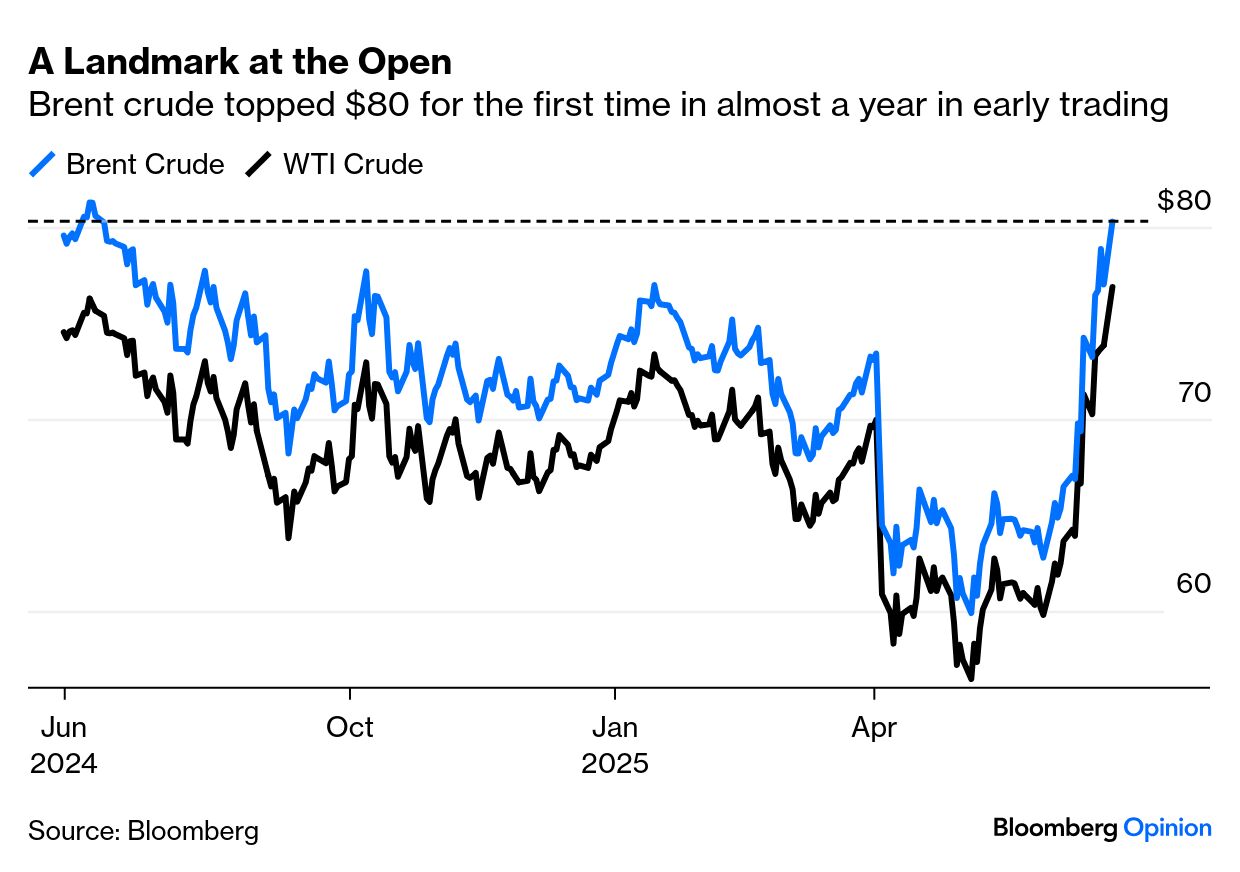

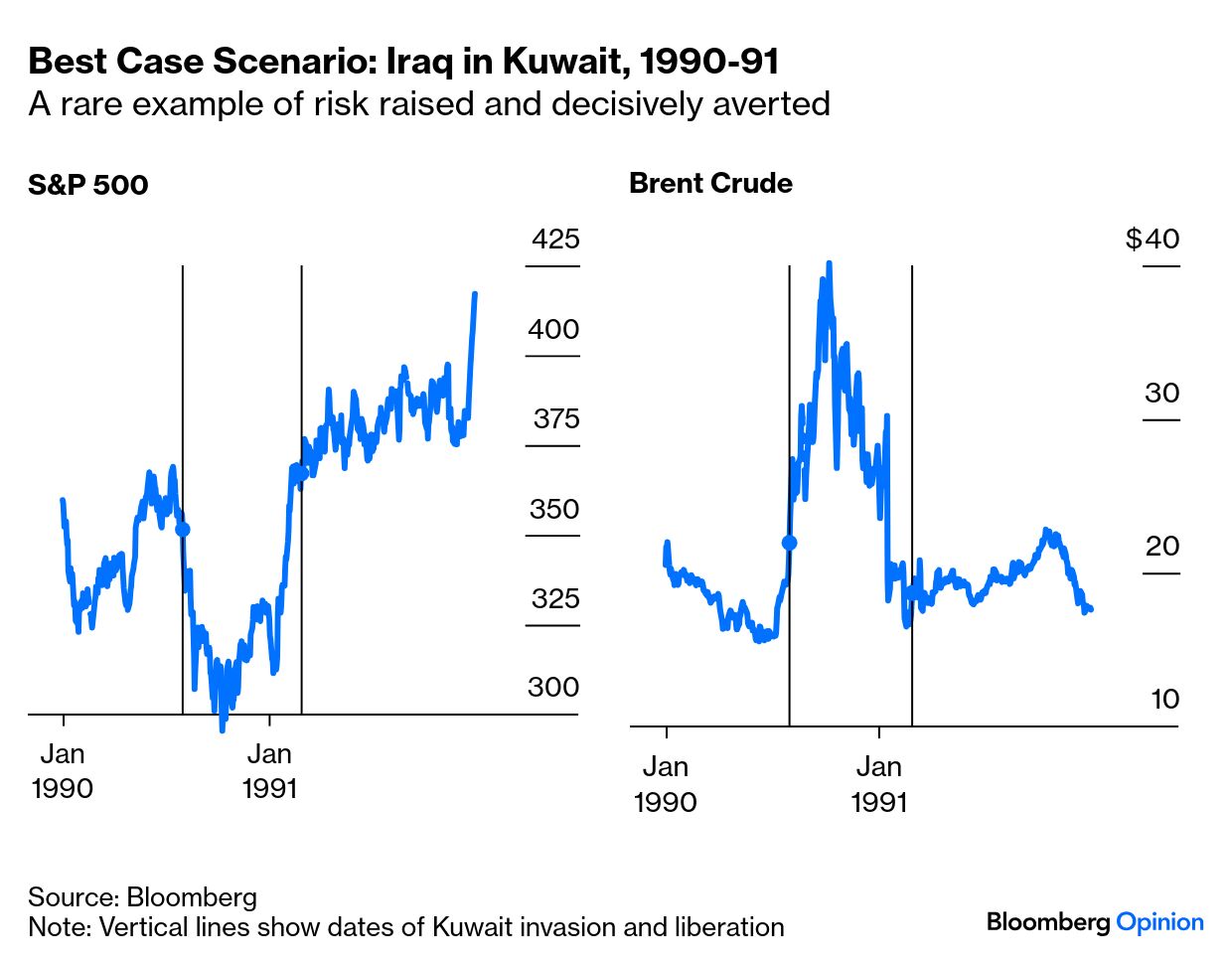

| Trump didn’t chicken out this time. As the US attempt to obliterate Iran’s nuclear sites ratchets up geopolitical tensions, the next critical question in the game of chicken is what the Islamic Republic does to retaliate. Its parliament has already voted to block the Strait of Hormuz, through which about 20% of global oil supply flows. If the country were to go through with that — and parliament doesn’t make the decision — then risk will climb higher. Prediction markets think it will probably happen: At the opening of Asian trading, crude oil did indeed rise significantly, with Brent crude topping $80 for the first time since last June. But the increase of 6% was relatively muted given all the political noise, and it didn’t hold above $80: Realistically, the template for hope is the first Gulf War in 1991, after Saddam Hussein’s invasion of Kuwait. That was a rare geopolitical incident that arose quickly, and was soon completely resolved: A massive Western military response booted Iraq out of Kuwait with surprising ease, and the supply of oil swiftly resumed. This time, the US has already declared its mission a success, without boots on the ground or loss of American life. But examples abound of misplaced optimism about short wars, from the First World War (supposedly “over by Christmas”), through Vietnam and “Mission Accomplished” in Iraq, to Russia’s misadventure in Ukraine. The case against escalation is that Iran is already Monty Python’s Black Knight: Tehran’s best available option might be, like Saddam after 1991, to reinforce itself at home while desisting from greater offensive ambitions. That would be a win for the US, and the oil market. Yet the regime has no choice but to retaliate if it wants to maintain its hold over its own people. Doing nothing would guarantee regime change. If it is to fall, it would far rather do so with a bang than a whimper. Closing the Strait, however, would be a desperate measure that might not last long. Tina Fordham of Fordham Global Foresight in London points out that parliament voted in a “consultative capacity”: Such a move would have to be approved by the Supreme National Security Council... It is not clear at this time whether this action will be implemented or is a kind of protest vote from the parliament. Long regarded as Iran’s “nuclear option” for the global economy, any move to close the Strait could be undermined by the US carrier (and likely US Navy SEAL) presence in the region — the likelihood is that the US response would be swift and severe.

Such an escalation would evidently create further risks, and until they have been contained as convincingly as they were by February 1991 after the Kuwait invasion, risk assets face a headwind. To quote Larry McDonald of Bear Traps Report: Iran has little downside to talking up the closure of the Strait of Hormuz. The real pain is the closure itself, which affects China, their cash cow, far more than the rest of the world. Bottom line: Oil prices will likely be elevated for the rest of the summer.

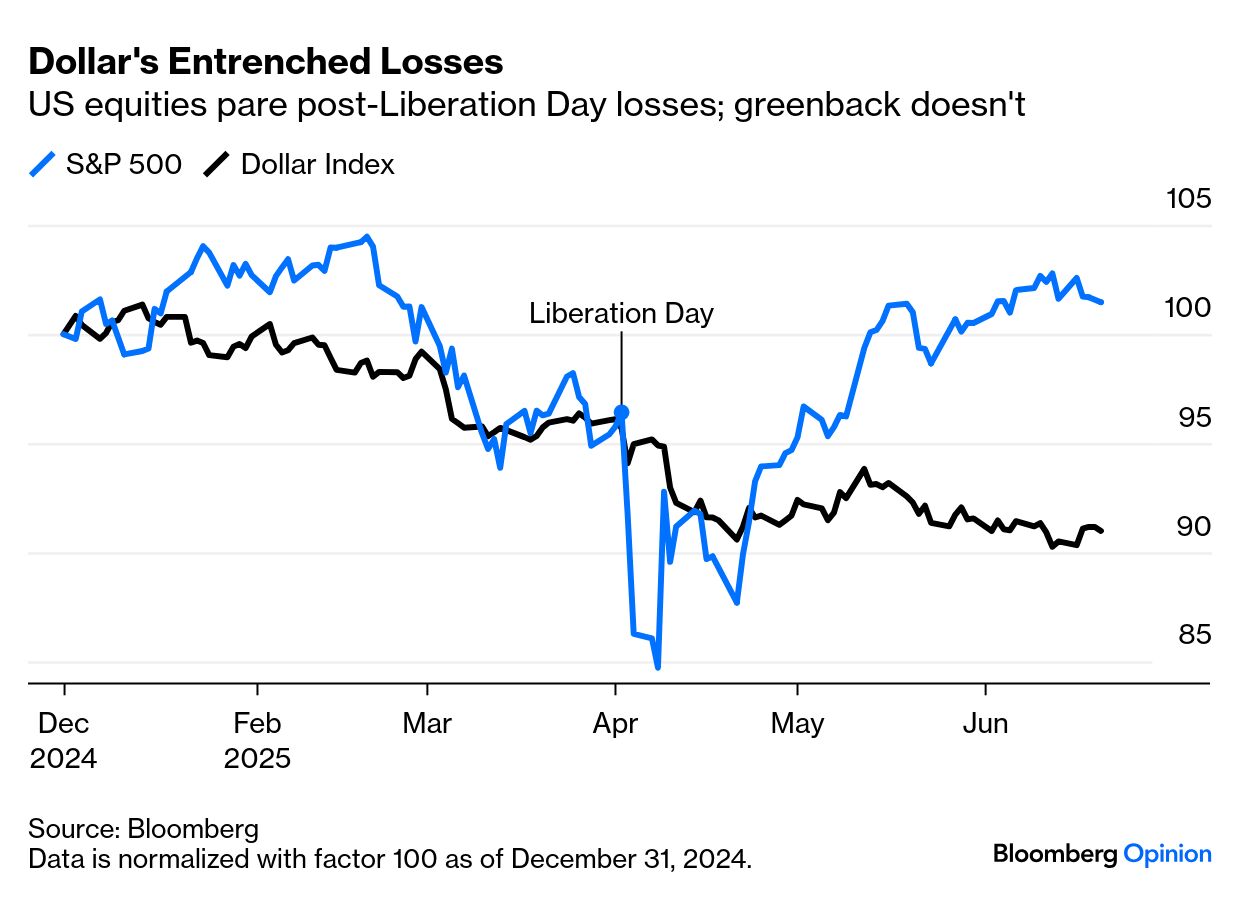

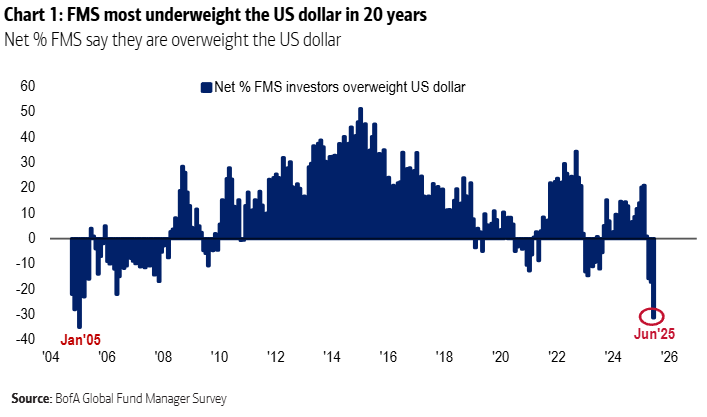

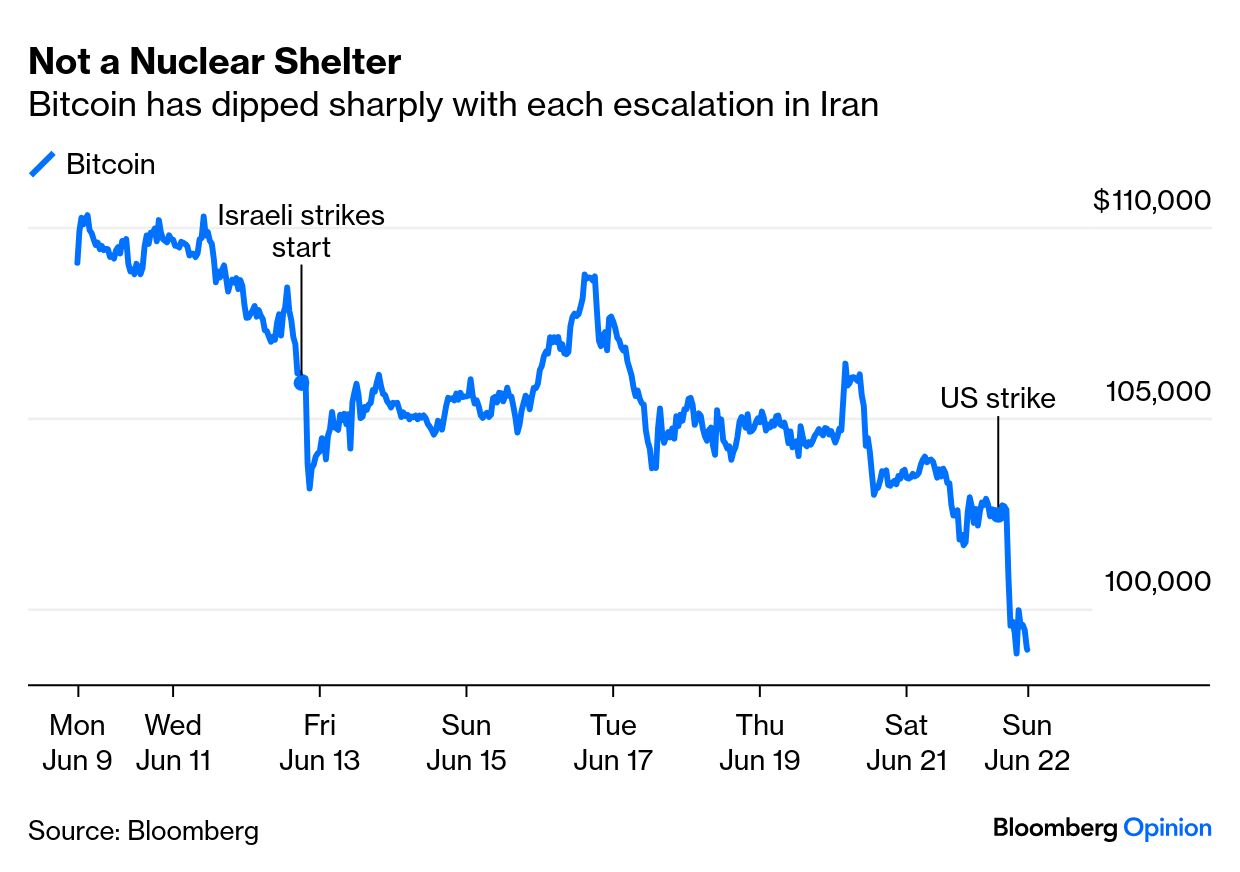

That would make it harder for the Federal Reserve to ease rates, and dampen economic activity. And that would in turn mean hits to commercial real estate, private credit, CCC-rated bonds, housing, and the US consumer. For now, what’s happened is a headwind for global equities. It’s little more than that as yet, but TACO-happy investors might want to take some money off the table. The dollar had been on a poor run before the Iran crisis, thanks to the unwinding of perceived “US exceptionalism” amid erratic trade policy. It’s lost nearly 10% of its value this year, falling to levels last seen in 2022. A semblance of trade policy clarity has helped equities erase their post-Liberation Day losses, but the dollar’s misfortunes linger: The currency ticked up slightly in early Asian trading, but a broader recovery would depend on fiscal and monetary policy as well as geopolitics. For now, Longview Economics’ Harry Colvin finds the dollar’s losing streak counterintuitive. “Normally, the opposite occurs: shocks and rising uncertainty typically generate a safe haven bid in the dollar. This time, that’s happened for gold, not the dollar.” If the greenback is to show that it retains its haven role, it should be now. Absent significant Iranian retaliation, UBS’s Andrew Garthwaite projects a weaker dollar for at least the second half of the year. The US foreign debt (88% of GDP, up from 9% in 2005), excessive global dollar holdings compared to its trade share, and a massive $13.4 trillion in unhedged dollar positions all suggest a move in this direction. Garthwaite sees additional pressure coming from threats of new tariffs, and particularly the notion that Washington could start taxing foreign investment funds. Reports of the dollar’s death may be exaggerated. Goldman Sachs Asset Management’s Gurpreet Garewal argues that it “remains dominant in global foreign exchange reserves, and no alternative matches its scale and liquidity.” The tendency to rally during risk-off episodes is not entirely extinguished. “While the dollar’s dominance may be diminished,” she adds, “it’s far from finished.” Longview Economics’ dollar sentiment model suggests a short-term rebound might be brewing. The dollar index is oversold, sentiment readings are bearish, and large investors are at their most underweight level in 20 years, as shown last week by the latest Bank of America fund managers survey: Meanwhile, one currency that is emphatically failing as a shelter is Bitcoin. Rather than attract investors looking for safety, it has sold off hard with each new ugly development in the Middle East and has dropped back below $100,000: Bitcoin is a “risk-on” asset that behaves like a speculative stock, not the haven its founders envisioned. Peter Tchir of Academy Securities also blames its appeal for those wanting secrecy: Why is crypto lower? Despite all the positive domestic headlines, we have seen time and again that when countries who are “known” to violate sanctions are hit, crypto tends to go down. Presumably because those countries now need to sell crypto to fund themselves (and why gold/commodities should outperform).

—Richard Abbey |