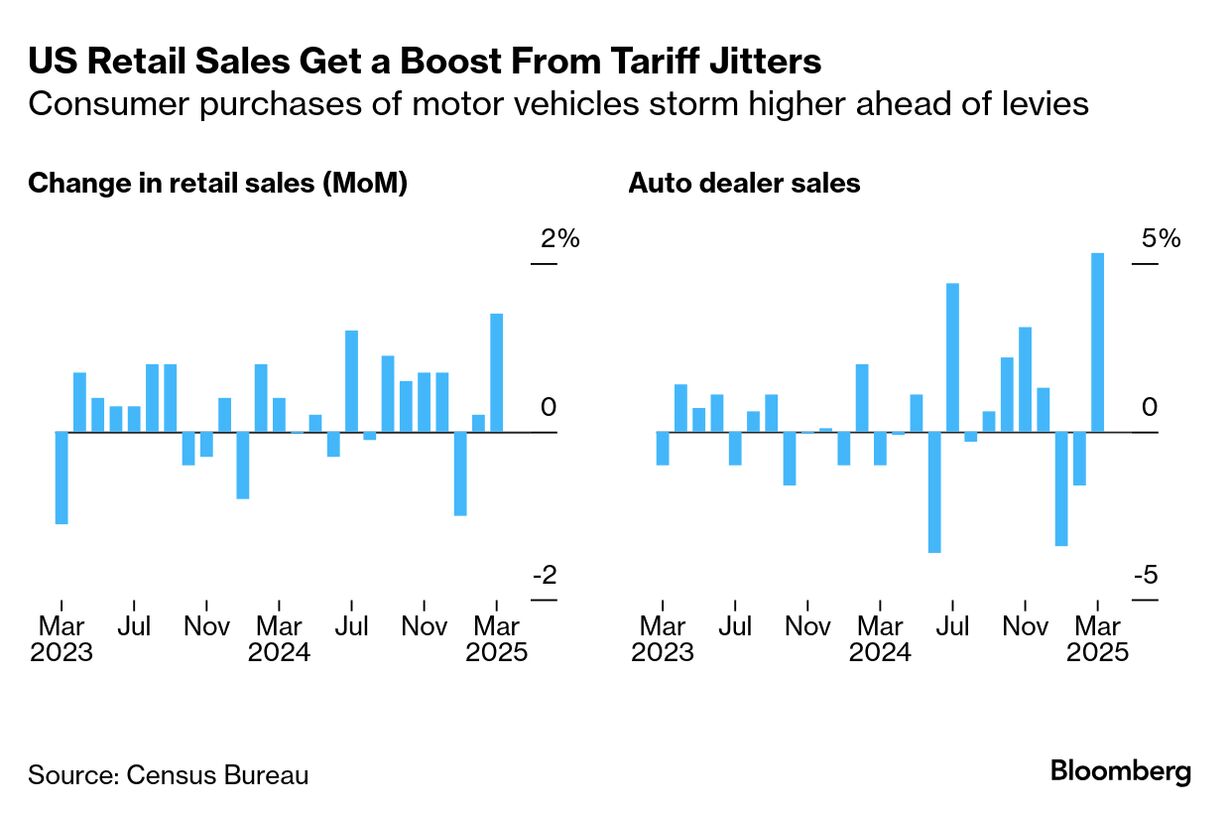

| I’m Cécile Daurat, an economics editor in the US. Today we’re looking at US retail sales. Send us feedback and tips to ecodaily@bloomberg.net. And if you aren’t yet signed up to receive this newsletter, you can do so here. Note: Economics Daily will return Monday following the Easter holiday. A March shopping spree by US consumers is coming to the rescue of the economy in the first-quarter. Spurred by the threat of high tariffs that will most certainly boost prices in the coming months, Americans bought cars, electronics and the type of items like sporting accessories that are often imported from China. The resulting jump in retail sales last month confirmed anecdotal evidence of a rush to buy now rather than later that anyone who visited a car dealership recently could witness. The surprise boost is also lifting estimates for first quarter economic activity. The Atlanta Fed’s GDPNow forecast is now showing a decline of only 0.1% — excluding the impact from gold trade — a better outcome than the larger drop that was predicted just a few weeks ago. Many forecasters, including Bloomberg Economics, see slower but still positive growth. For now, government data on spending, inflation and the labor market show no sign of strain from the tariff gyrations. But it may be a matter of time. Wall Street economists have increased their recession odds, consumer sentiment is near a record low in data going back to the 1950s, and companies big and small are at a loss when trying to figure out how tariffs will apply to their supply chain and whether they’ll be passing the costs on to consumers. Speaking at an event at the Economic Club of Chicago Wednesday, Federal Reserve Chair Jerome Powell acknowledged that a weakening economy and elevated inflation could eventually bring the central bank’s two goals into conflict. “We think consumption will effectively stagnate over the next couple quarters, as the tariff-linked hit to real incomes and greater economic uncertainty weigh on spending,” Pantheon Macroeconomics wrote in a note. The Best of Bloomberg Economics | - President Donald Trump said Powell’s termination as Fed chief can’t come quickly enough, arguing that the US central bank should have cut rates already.

- Central banks in South Korea and Ukraine kept rates unchanged, while Turkey unexpectedly hiked. Later today, Egypt may see its first cut since 2020.

- Putin is drawing up a legal framework for companies looking to invest in post-conflict Russia — firms are wary.

- Australia’s unemployment ticked up in March, showing a weaker labor market even before the hit from Trump’s tariffs.

- Japan’s exports rose at a slower pace in March and officials began formal trade talks with the US. Meanwhile, the BOJ may pause rate hikes.

- Lesotho is at risk of a liquidity crisis if Trump follows through on plans to impose a 50% levy on imports from the tiny southern African mountain kingdom.

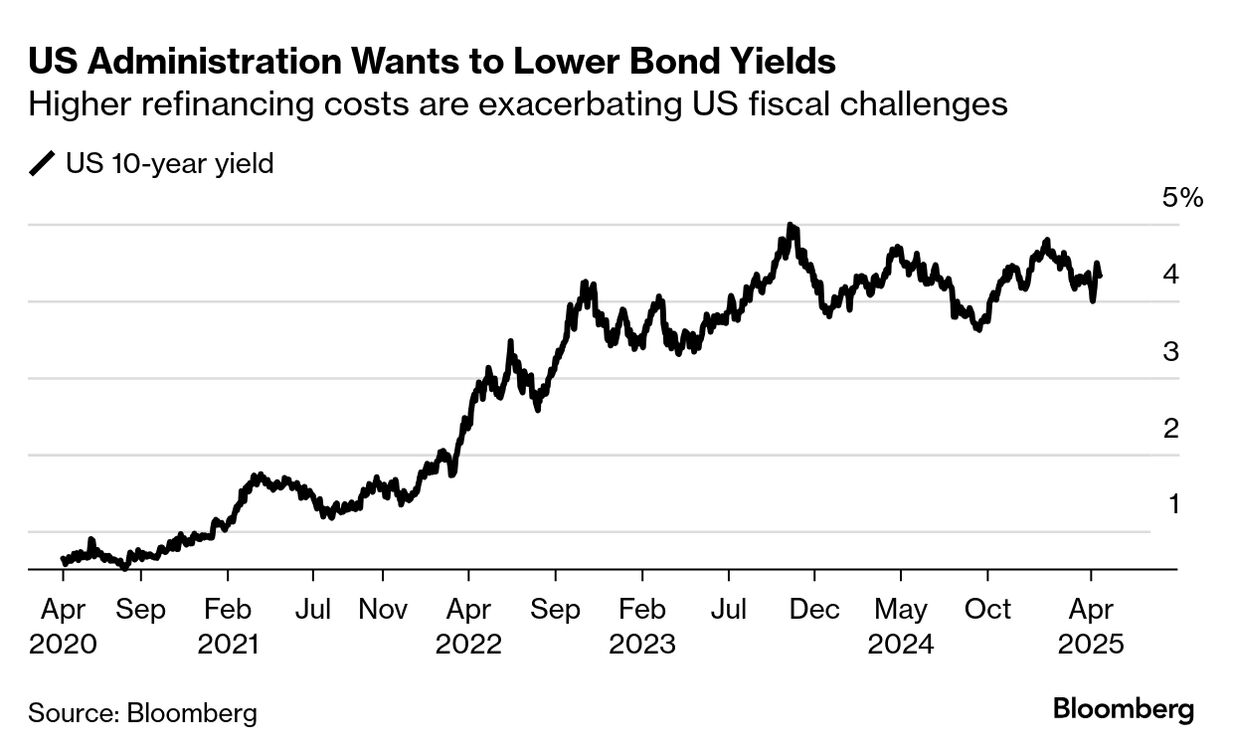

Last week’s selloff in US Treasuries notwithstanding, 10-year yields are well below their peak levels hit in mid-January, thanks in part to diminished expectations for economic growth this year. Lower rates would suggest relief for the federal government with respect to its interest bill. But this isn’t a good trade-off. Torsten Slok, Apollo Global Management Inc.’s chief economist, highlighted in a note to clients Wednesday that economic downturns do more damage to the government’s budget than can make up for the interest-cost savings from lower yields. Let’s say interest rates drop by 2 percentage points (five-year Treasury yields are currently just under 4%). That would save around $500 billion in annual interest, Slok says. But history indicates that, during recessions, the US budget deficit deepens by around 4% of GDP — corresponding to “an additional $1.3 trillion erosion of US government finances measured in 2025 dollars,” Slok says — dwarfing the interest savings. The bottom line: “Creating a recession to lower long rates is not a good idea,” Slok wrote. |